Tariffs, trade wars and the fallout for PKR

MG News | August 09, 2019 at 05:52 PM GMT+05:00

August 8, 2019 (MLN): The aftermath of a never-ending trade war between United State of America and People’s Republic of China has now begun to seep through to their respective trading partners and its consequences shall be paramount, from what we have put together.

So where did it all start?

To provide a little background, the spat between US and China broke out back in 2016, shortly after US President Donald Trump assumed position and decided to wage a trade war against Europe, Mexico, Canada, Japan and above all, China.

The motive was to promote domestic manufacturers in the US, but China being a tough nut to crack did not only stand strong and upfront against all the attacks launched by the US in the past 18 months or so, it also retaliated in full force, thereby giving the most powerful economy in the World a tough time.

While Trump eased his wrath on the rest of America’s trading partners once minor changes were made in the existing trade arrangements, it brought the sky down on China by threatening to impose tariffs on its exports.

Retaliation by China has hurt American farmers the most as a result of which, farm bankruptcy has been on the rise during this whole time, despite government bailout.

According to Bloomberg, tariff imposition on Chinese imports has generated around $20 billion since the start of 2018 whereas bailout payments to the farmers has been summed at over $25 billion which shows a net loss to America.

The Current Scenario…

The most recent development in this Feud unfolded when Donald Trump announced to put an additional 10% tariff on the remaining $300 billion worth of goods imported from China by US, from September 1, 2019. This imposition would be exclusive of a pre-existing tariff of 25% on the $250 billion imports.

Two days later, in another rather sarcastic post on his official social media handle, Donald Trump wrote that, “Things are going along very well with China. They are paying us Tens of Billions of Dollars, made possible by their monetary devaluations and pumping in massive amounts of cash to keep their system going. So far our consumer is paying nothing - and no inflation.”

In retaliation, China was expected to lower its currency so as to somehow cancel out the impact of these new tariffs, but what happened next surprised analysts all around the World.

China took things to the next level by letting the Chinese Renminbi (RMB) fall past 7 against the dollar, a barrier it hasn’t crossed since 2008, thus letting its currency fall to an all-time low in over a decade.

On a side note; People’s Bank of China strictly monitors the RMB/USD rate which is only allowed to deviate by 2% or less from a midpoint that is fixed by the bank on a daily basis.

While the bank has officially associated the depreciation to a shift in demand and supply, the ongoing conjecture is that the drop would not have happened had the bank not allowed it. Note that such an event was avoided last year and in 2016 during bouts of depreciation, when China spent $154 billion in a single month to restore its currency.

By making Chinese products cheaper to import for Americans, China has attempted to nullify the impact of the recently imposed tariff.

There is no denying that this move has turned things exciting for those following the war, but the fact remainsthat this is bound to have a serious impact on currencies all across the globe, including Pakistan.

Weaker RMB means lower demand from China since its imports will become more expensive. This in turn would constrict the global economicgrowth.

Weaker RMB also means that Chinese exports will become cheaper and will steal its competitors’ sales, which is why another pressing concern is that this bout of devaluation on China’s part will have a domino effect on the currencies of its trade competitors as they will eventually have to devalue their own currencies in order to keep the competition fair.

Going by reports, the Australian dollar has already dropped to a low that hasn’t been seen since the global financial crisis, by 68 cents.

Economies near the Chinese region are also expected to follow Australia, including South Korea, Vietnam, Thailand, India and Indonesia.

Report has it that the European Union and Japan have also hinted at a rate cut in the near future.

Pakistan’s Next Challenge?

Currency-wise, Pakistan is presently living its best life in the last one month as a result of higher remittances on account of Eid ul Azha.

This means that the country should enjoy it while it lasts because the festival is just around the corner and once it is over, the inflow of remittance might see a clear decline, thereby withdrawal of the supporting hand that has been pushing up PKR.

Once other countries in the region start devaluing their currencies in response to CNY fall, the trend is expected to complete a full circle until its PKR’s turn to depreciate.

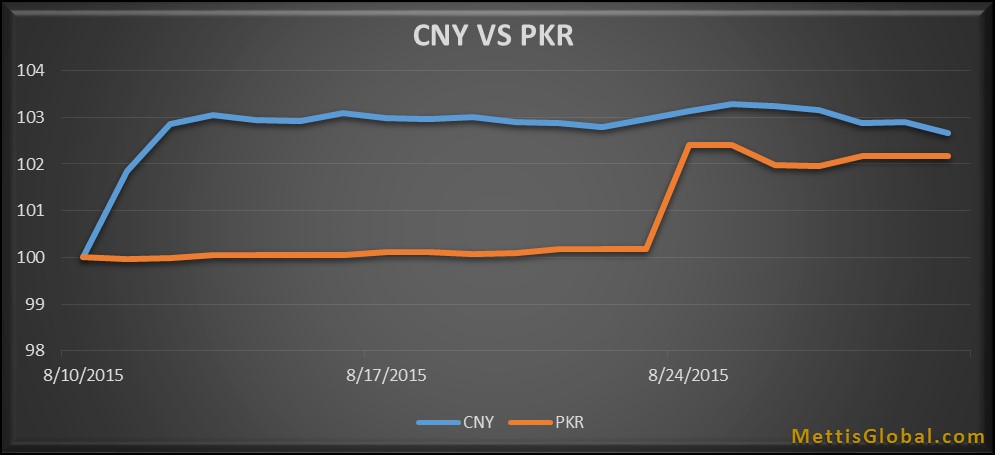

Looking at past trends, amongst China’s many bouts of depreciation in the last few years, one of the most significant one took place on August 11, 2015 when China knocked off 3% of its value over three consecutive depreciations, allegedly in an attempt to boost exports.

(Chinese Yuan) CNY’s descent was immediately followed by (Indian Rupee) INR as India competes with China in several sectors including textile, chemical and metals. Resultantly, INR dropped to a two year low and continued to trade low for the latter half of the year.

Meanwhile PKR joined the trend a day later as its began to depreciate slightly at first, extending its spell to 8 days with a one day breather in between before drastically losing Rs.2.3 on August 24, 2017. During this whole bout, PKR lost around Rs.2.5 to dollar, to touch Rs.104.3 per USD, a depreciation of about 2.5%.

Similarly, a comparatively smaller but prolonged round of CNY depreciation took place in November 2016 which was again quickly followed by an extended period of depreciation in PKR.

These trends imply that hadn’t remittances in Pakistan been on a rise, PKR would be depreciating as we speak.

What happens to PKR then?

Another aspect of this debate pans the spotlight on Pakistan’s Real Effective Exchange Rate (REER) which was last spotted at 90.5 in June. What we need to know about the REER is that it has two basic components; exchange rate and inflation.

When a country’s trading partners observe devaluation and inflation, its REER index goes up.

Now Pakistan has been running a trade deficit since 2005, and has a comparatively smaller role to play in the international trade field but its trading partners are expected to experience depreciations, while its biggest trading partner China has already experienced it.

As mentioned before, this would raise Pakistan’s REER a little. Since we are currently at 90.5, Pakistan’s REER has a 10 point margin to move without becoming overvalued.

But sadly IMF is watching and Pakistan is bound in a deal with the Fund to keep PKR undervalued in order to promote exports.

To top it off, the recent Kashmir issue and US-China spat might add a few more pounds to the weight that pulls down the currency.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|