SBP maintains policy rate at 22% for fifth consecutive meeting

MG News | January 29, 2024 at 04:15 PM GMT+05:00

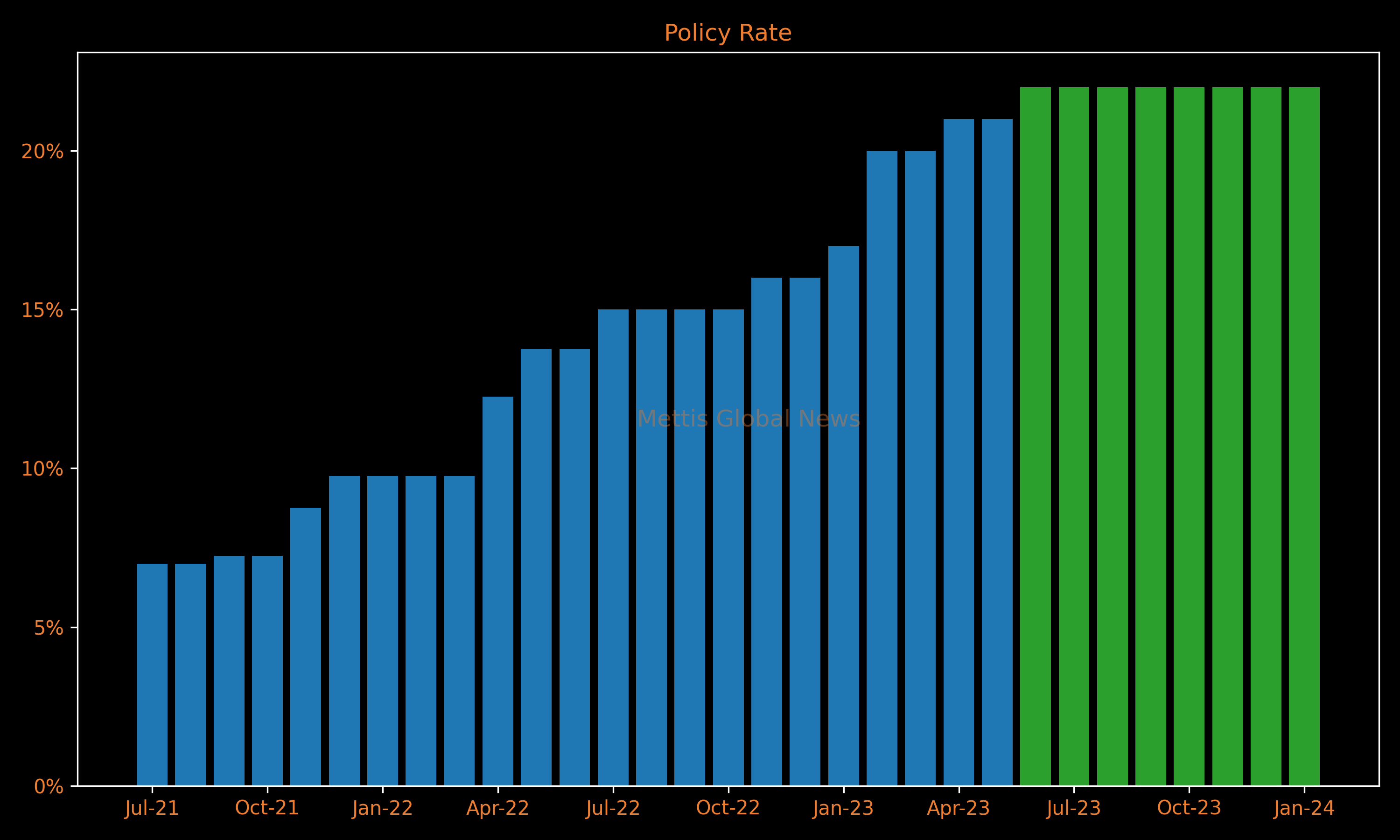

January 29, 2024 (MLN): The Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) in its meeting held today, has decided to keep the policy rate unchanged at 22% for the fifth consecutive meeting.

The decision came in line with the market expectations wherein the majority of market participants were in consensus on the rate pause.

The committee observed that the frequent and sizeable adjustments in administered energy prices have slowed down the pace of decline in inflation anticipated earlier, besides impeding a sustained decrease in inflation expectations.

On the other hand, the non-energy inflation continues to moderate, in line with the committee’s expectations.

On balance, the committee viewed that the real interest rate remained significantly positive on 12-month forward looking basis, as inflation is expected to remain on a downward path.

The MPC noted several key developments since its December meeting, which have implications for the economic outlook.

First, the FX reserves have improved on the back of a notable surplus in the current account in December and significant financial inflows, including the latest IMF SBA tranche.

Second, fiscal consolidation remained on track and complemented the monetary policy stance.

Third, the business sentiments, as reflected in the recent surveys, continued to improve.

However, the escalated geopolitical tensions in the Red Sea region have led to a surge in global freight charges and are posing risks for global trade and commodity prices.

Taking stock of these developments as well as still-elevated levels of both headline and core inflation, the committee emphasized on continuing with the tight monetary policy stance.

This, along with continued fiscal consolidation and timely realization of planned external inflows, will help to achieve the inflation target of 5-7% by September 2025.

The revised assessment takes into account the recent and expected adjustment in administered energy prices

Real sector

Incoming data continues to support the committee’s earlier assessment of moderate economic recovery, primarily led by the agriculture sector.

Real GDP growth projection remains unchanged in the range of 2 to 3% for FY24. While Kharif crops’ output already turned out better than last year, the prospects for Rabi crops also appear promising amid better input conditions.

In the industrial sector, large-scale manufacturing registered a slight decline in the first five months of FY24, with a moderate increase recorded in November.

The recent survey results also showed consistent increase in capacity utilization in the manufacturing sector, while business sentiments, for both industry and services, turned positive for the first time since April 2022.

The committee assessed that momentum in the industrial sector is expected to pick up from 2HFY24.

External sector

The current account surplus in December 2023 helped bring down the 1HFY24 deficit by 77% to $0.8 billion.

The exports registered a growth of 5.3% YoY during 1HFY24, supported by growth in rice and volume of HVA textiles.

At the same time, imports declined considerably due to lower international commodity prices, better domestic crop output, and a decline in oil import volumes.

These factors more than offset the pick-up in non-oil import volumes.

Moreover, workers’ remittances continued to improve for the second consecutive month in December. In the financial account, the increase in official inflows in December, together with the receipt of IMF-SBA tranche, improved the SBP’s FX reserves to $8.3bn as of January 19, 2024.

The committee noted that the projection of current account deficit for FY24 remains unchanged in the range of 0.5 to 1.5% of GDP, despite the modest economic recovery and elevated level of profit and dividend repatriation.

Fiscal sector

The fiscal position continued to improve during Jul-Oct FY24. The overall deficit declined to 0.8% of GDP from 1.5% last year, while the primary surplus increased to 1.4% as compared to 0.2% last year.

This improvement is mainly led by a significant increase in revenue collection and somewhat restrained expenditures.

FBR tax collection grew by 30.3% during 1HFY24 amidst gradual recovery in economic activity and continued impact of taxation measures, while non-tax revenues also remained strong.

On the expenditure side, the decline in non-interest spending (as percentage of GDP) helped to keep overall expenditures at contained levels.

The MPC noted that the continuation of fiscal consolidation is essential for ensuring sustainability of public debt as well as overall macroeconomic and price stability.

Money and credit

The broad money (M2) growth, which has been hovering around 14% in FY24, surged to 17.8% YoY as of end-December 2023.

The MPC assessed that this acceleration is temporary and is expected to reverse in the coming months, as already depicted in the latest weekly monetary data.

The improvement in the external position has increased the net foreign assets of the banking system. In contrast, growth in net domestic assets of the banking system decelerated, primarily due to a slowdown in private sector credit (PSC).

This is primarily explained by relatively low fixed investment loans and a net retirement in in consumer loans.

However, the demand for working capital loans remained close to last year.

The committee also noted the continued declining trend in currency to deposit ratio, which was due to the strong growth in bank deposits and a decline in currency in circulation.

Inflation outlook

The MPC noted that both food and core inflation are moderating for the past few months.

This trend reflects the positive impact of tight monetary policy stance duly supported by ongoing fiscal consolidation, lower global commodity prices, and improved domestic crop output and supplies.

However, the positive impact of these developments is being diluted by sizable adjustments in administered energy prices, especially from November 2023 onwards.

The large adjustments have significantly impacted the inflation outturns and its near-term outlook.

In this regard, the committee emphasized on reforms to address underlying structural issues, especially those in the energy sector, to achieve price stability on a sustainable basis.

Incorporating the inflation in 1HFY24, expected significant decline in the second half, and the evolving risks, the MPC expects average inflation to fall in the range of 23 – 25% in FY24 and continue to trend down noticeably in FY25.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,740.00 | 64,610.00 63,260.00 | -380.00 -0.59% |

| BRENT CRUDE | 89.13 | 90.03 86.60 | 1.41 1.61% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.40 | 84.61 81.27 | 1.27 1.55% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|