PSMC delisting: Are minority shareholders getting a fair shake?

Nilam Bano | January 19, 2024 at 10:54 PM GMT+05:00

January 19, 2024 (MLN): Ensuring the protection of shareholders' rights serves as the foundation for business success. However, when access to these rights is restricted for minority shareholders, it leaves a sour taste that repels corporate cream from the local stock exchange over time.

In this scenario, minority shareholders not only find themselves excluded from decision-making but also bear the brunt of the consequences at large. In the intricate game of corporate ups and downs along with complex regulations, they can discover fewer opportunities for advancement and encounter more unforeseen challenges.

The recent event of the delisting of Pakistan Suzuki Motors Company Limited (PSX: PSMC) portrays a similar picture where minority shareholders see things differently than majority stakeholders.

When did it all start?

On October 12, 2023, the majority shareholders of PSMC expressed their intent to purchase all outstanding shares of PSMC and potentially de-list the company. Later, on October 19, 2023, The Board of Directors (BoD) of PSMC resolved to delist the company.

The decision of delisting was taken in the interest of minority shareholders especially in light of the low trading prices of the company's shares, according to the spokesman for PSMC.

“In light of these circumstances, the sponsors and majority shareholder, Suzuki Motor Corporation, are planning to acquire all outstanding shares and securities held by minority shareholders, to offer them a fair exit,” he stated.

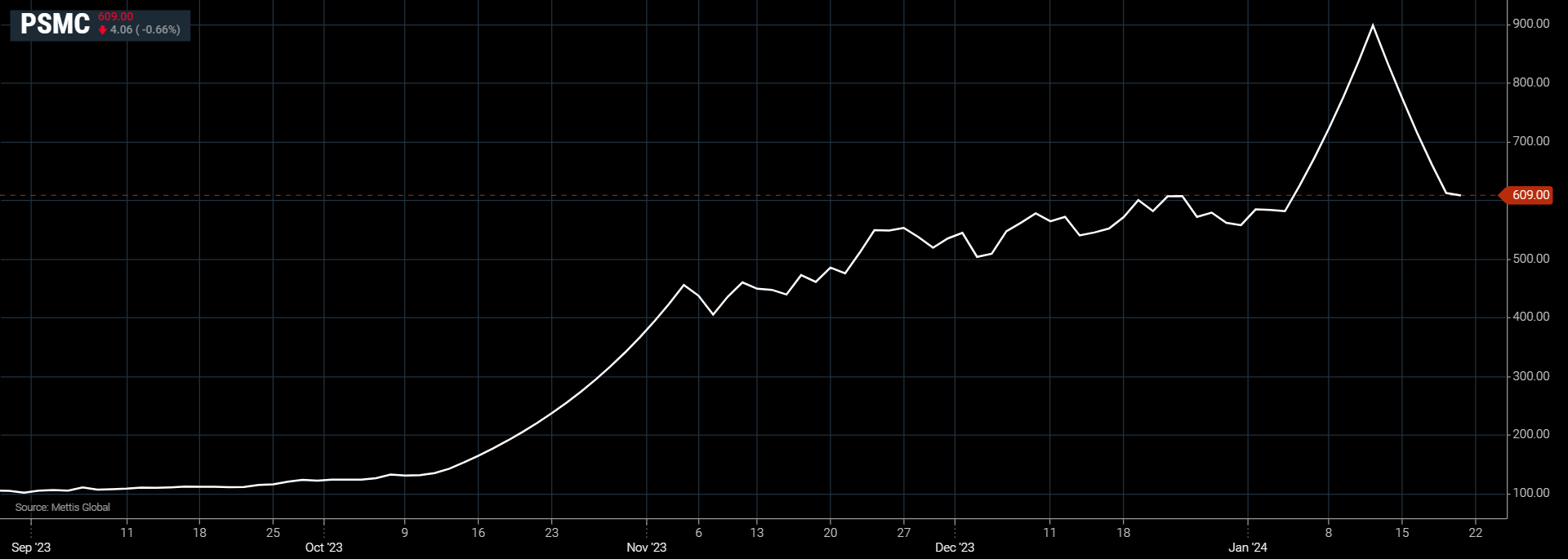

To note on October 11, 2023, the scrip price was Rs136. Right after this development when majority shareholders of PSMC expressed their intent to purchase all outstanding shares, the scrip started gaining attraction and witnessed a series of daily caps with its historic high of Rs919 on January 12, 2023, a surge of 6.75x.

On December 04, 2023, the company as the majority shareholder proposed to purchase 22,145,760 ordinary shares (26.91%) of the paid-up share capital of the company held by the minority shareholders at a minimum purchase price of Rs406/- per share.

How did the company calculate this price?

The intrinsic value per share of the company is determined based on the revaluation of fixed assets carried out by Iqbal A. Nanjee & Co. (Pvt.) Ltd. who are approved valuators by the Pakistan Banking Association and one of the valuators under PSX's approved valuators list.

VDC decides buyback on Rs609 per share:

On January 15, 2024, the PSX said that its Voluntary Delisting Committee (VDC) determined the minimum buyback price of PSMC is Rs609 per share after having detailed discussions with the representatives of the Sponsors and after taking into account all the relevant aspects under the applicable regulations.

What is the relevant aspect on which the VDC increased straight Rs200 per share on the company’s suggested price of Rs406 per share for buyback? Seems like sprinkling some fairy dust on the suggested price of Rs406.

Royalty realities leave shareholders questioning the price tag:

To note PSMC pays a noble tribute in the form of brand royalties to Suzuki Motors and as a result of delisting, there must be a call for fair compensation to shareholders, recognizing the esteemed value embedded in the brand.

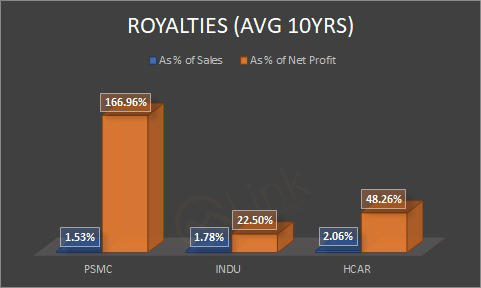

Based on the last available annual report of CY22, PSMC paid royalties of Rs4.2bn to SMC which is 2% of net revenue and 36% of the total gross profit. In the latest quarter, in 3QCY23, it paid 2.5% which is above the industry average.

However, the delisting price of Rs609 per share or $2.2 per share may not reflect the brand value. Though the size of the balance sheet is currently depressed due to COVID-19 and continuous plant shutdowns, the book value of the company before covid was hovering around $2.75 per share (5 years average CY15/19).

The delisting price, in dollar terms, is even below the book value of the company before COVID-19. (21% discount).

Within the industry, PSMC pays relatively higher Royalty as compared to INDU and HCAR as the 10-year average royalty as a percentage of net profit stands at 166.96%.

Delisting indigestible amidst huge potential, auto boom:

Minority shareholders seem unhappy with the decision as this delisting came at a time when the automotive industry is witnessing substantial growth, as evidenced by Suzuki Motor Corporation's plans to invest $4 billion in India's Maruti Suzuki.

This investment aims to establish a second manufacturing facility with an annual production capacity of 1 million units.

Comparatively, PSMC's shareholders are left grappling with a buyback offer that may not adequately reflect the true value of the company.

If the potential of PSMC is harnessed, a transparent approach could lead to a more favourable outcome for minority shareholders.

Considering the replacement cost of a manufacturing facility in India, a similar investment in Pakistan for a plant with 150,000 capacity could amount to over $500m.

In India, the per-car cost would be $4,000, i.e., $4,000,000,000/1,000,000.

On the other hand, in Pakistan, the delisting price of Rs609 per share, determined by the stock committee, equates to approximately $1,200 per car, based on a plant capacity of 150,000 cars. This is more than 3.3x lower than that of India.

This stark contrast posed a question of whether minority shareholders in PSMC are receiving fair compensation for their investments.

Climate change is encouraging people to go for compact electric cars. Suzuki has taken the lead in the EV segment and has a bright future ahead.

Is it time that Suzuki starts selling EV cars as Suzuki Maruti is planning and help Pakistan get rid of smog and climate change issues? In that case, it could also be a US $ 10 billion market cap company, a first for Pakistan, according to Nadeem Nisar, a Shareholder having over 10% holding in the company told Mettis Global.

With sky-high prices of cars in Pakistan, Suzuki has become the top choice in the middle-class segment and it is anticipated that it would gain more market share as the economy recovers, he added.

During the last seven years Suzuki has on average sold 110,000 automobiles per annum; a mere 7% net margin puts its earnings in the range of Rs350-450 per share. The margin in the case of Suzuki Maruti was more than 10% last year, he highlighted.

In the last two quarters, Suzuki has earned an income of Rs85 per share while working only at 27% capacity. What would be its earnings working at 80% capacity? Does any other Japanese car company pay 4% of the revenue as commission to dealers except Suzuki? he questioned.

|

Comparison of commission paid to dealer |

|||

|---|---|---|---|

|

|

PSMC |

HCAR |

INDU |

|

Net Revenue |

202,467 |

95,087 |

177,710 |

|

Dealers' Commission |

7,871 |

1,645 |

4,393 |

|

Commission to the dealer as % of Sales |

3.9% |

1.7% |

2.5% |

PSMC data is for 2022, while figures for others are for 2023

(Amount in PKR Million)

The potential of the company showcases and gives a vibe that minority shareholders sense that they are not being offered the potential price.

Considering the aforementioned factors, there is a need for a more equitable approach to determining the company's value.

Additionally, in 2022, the company recorded a discount of Rs15.bn, while its net loss for the year stood at Rs6.4bn. This might be indicative of value erosion for the shareholders in both earnings and valuation during the delisting process.

Need to adopt the Reverse Book Building (RBB) method:

The PSX’s relevant regulatory authorities are urged to reevaluate the delisting process and consider the adoption of a Reverse Book Building method which is the only forum to ensure a fair and just outcome for all stakeholders involved.

It will be the right course of action as when companies go public on the PSX, they present optimistic outlooks in their prospectuses, but in the delisting scenario, they refrain from sharing reports and outlooks.

While deciding the IPO floor price, the sponsors' input (seller) is considered, but during delisting, no effort is made to seek the consent of minority shareholders on the minimum buyback price.

Let the shareholders discover the price irrespective of their quantum of shareholding just like IPO.

The Reverse Book Building is a process used for efficient price discovery. You can take it as a mechanism provided for capturing the sell orders on an online basis from the shareholders. When the Reverse Book Building is started, offers are collected from the shareholders at various prices, which are above or equal to the floor price.

Using Reverse Book Building, after offers from shareholders have been received, a price is then identified by evaluating received offers where Acquirer can delist its shares.

During the Reverse book-building process, Shareholders are free to decide the price at which they want to give their shares back to the company. They can offer their shares at Rs 100 and Rs 1000 also. The only restriction shareholders will have to follow is that they can't offer their shares below the Floor price. So, the offer price could be equal to the floor price or higher than it.

For successful delisting, the acquirer is required to buy at least that amount of shares from public shareholders which if added to the existing holding of the acquirer, will exceed 90% of the total shares issued by the company.

Thus, the regulatory authorities at PSX must ensure that minority shareholders have an equal chance in the delisting process as whether a shareholder is a majority stakeholder or a minority one, rights should remain the same.

Otherwise, such a delisting dilemma will continue to threaten Pakistan's investment appeal.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,070.00 | 64,215.00 64,070.00 | -145.00 -0.23% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|