Policy Rate Reversal: Sooner or Later!

Muhammad Ghazanfar Sakrani | December 04, 2023 at 10:18 AM GMT+05:00

December 04, 2023 (MLN): After a cumulative raise of almost 4,000 bps in policy rate by nine developed economies, markets around the world are pricing an end to interest rate hikes.

Rate traders are reinforcing their stance on a reversal in interest rates by the mid of next year after two years of a global cycle of rate hikes. Swap contracts depict a quarter percentage point decline in Fed rates from its current levels of 5.25%-5.5%.

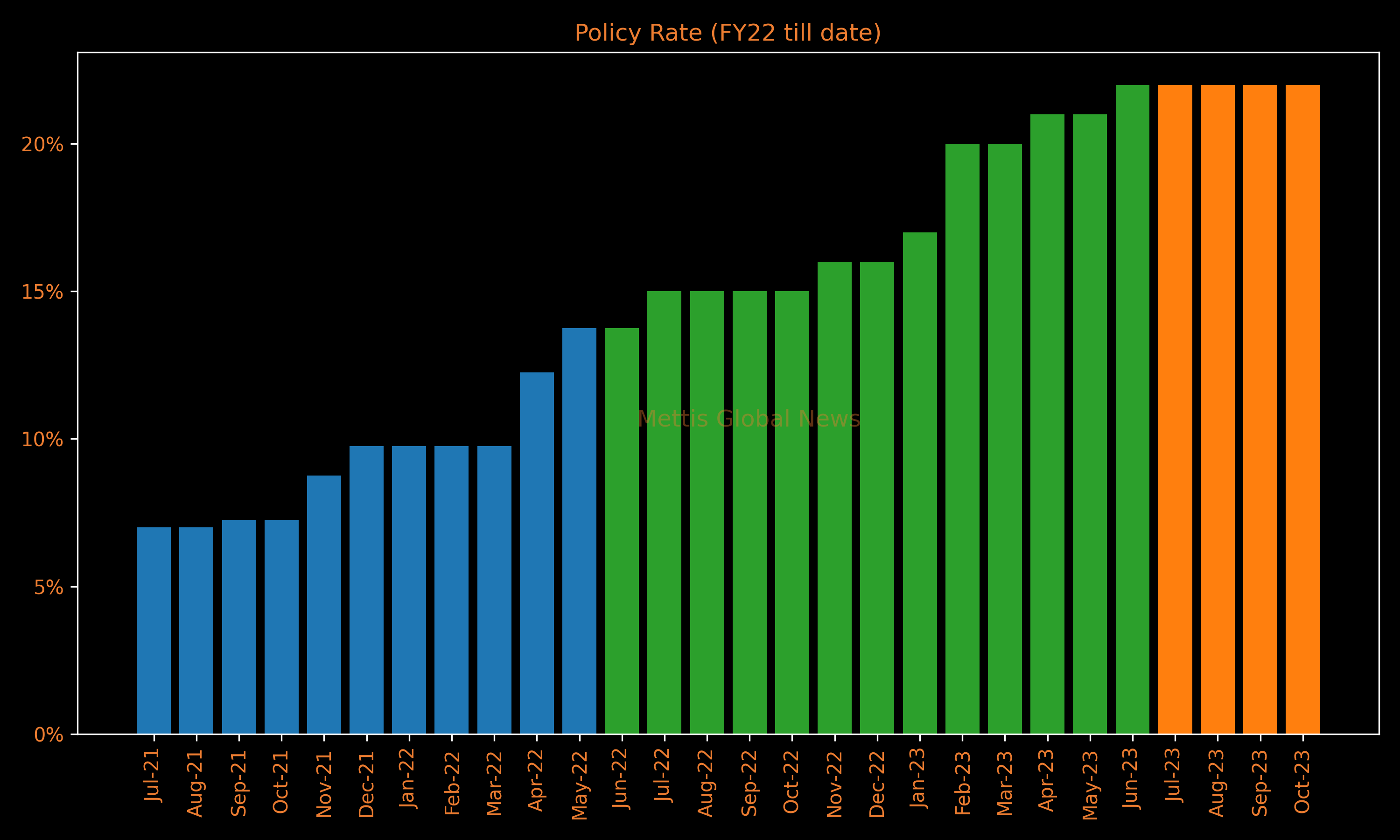

In Pakistan, the policy rate has reached its peak as per its incumbent governor and a status quo has been witnessed since the last couple of MPC meetings.

Will the next MPC meeting on December 12, 2023, be the start of a reversal in interest rates which have remained on an upward trajectory since September 2021?

Skyrocketing inflation in Pakistan has been the root cause of monetary tightening. The country’s inflation, which touched 38% in May 2023 has started to cool down amid a high base effect, downward adjustments in fuel prices and ease in prices of major food commodities.

Inflation for October dropped to 10 months low of 26.9% which bolstered hopes of decelerating inflation in FY24 as compared to the last year. The country is also on the track of fiscal consolidation as evidenced in the first quarter of fiscal year 2024.

Moreover, the reduction in the current account deficit propped up the fragile position of SBP reserves. The country’s growth rate also enhanced by 2.13% in the first quarter of the current fiscal year, compared to adverse growth observed in FY23.

In the recent auction of treasury bills, increased participation was witnessed in 12-month tenor t-bills. The same pattern was observed in the previous auction.

The cut-off yields were also slashed by 5 to 7 bps for 3, 6 and 12-month t-bills. As per the central bank, the real interest rates are positive on a 12-month forward-looking basis.

All these developments may lead some participants to price interest rate cuts in the upcoming policy meeting.

However, as of yet, the stage may not be set for a decline in policy rates. The country’s inflation rate for July-Oct 2023 remained at 28.5%, well above the official target of 21% for the year.

The core inflation of 26.7% for rural also remains ahead of the policy rate. After dipping in October, the inflation elevated in November to 292% owing to a massive surge in gas prices. The weekly sensitive price index (SPI) inflation on November 16 raised eyebrows as the recently imposed fixed charges within the gas tariff structure led to a 480% surge in gas prices.

Inflation is also expected to remain sticky due to the fuel cost adjustment at 3.5 rupees/kwh in the month of December. The introduction of a new Axle Load Regime (ALR) is also expected to raise the cost of living.

No significant decline was observed in petrol prices in the second fortnightly review.

Moreover, the weakening of Real Effective Exchange Rates (REER) depicts that the exchange rate which has stabilized after a long time may come under pressure in case of a dovish policy stance until inflation further slows down. Consequently, the pivot in the upcoming policy meeting may be far-fetched.

The country may experience an expansionary monetary stance from the upcoming fiscal year which will provide much-needed breathing space to industries heavily reliant on bank financing.

The government will also largely benefit from the monetary easing whose debt servicing is expected to remain around Rs.8 trillion in the current fiscal year, almost 10% higher than the budgeted expense of Rs.7.3 trillion.

Though the hawkish monetary policy has had its day, the milestone moment of reversal in monetary stance may initiate from the upcoming fiscal year.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 135,939.87 307.74M |

-0.41% -562.67 |

| ALLSHR | 84,600.38 877.08M |

-0.56% -479.52 |

| KSE30 | 41,373.68 101.15M |

-0.43% -178.94 |

| KMI30 | 191,069.98 82.45M |

-1.17% -2260.79 |

| KMIALLSHR | 55,738.07 422.01M |

-1.03% -577.24 |

| BKTi | 38,489.75 45.79M |

-0.02% -8.33 |

| OGTi | 27,788.15 6.87M |

-1.24% -350.24 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 117,300.00 | 120,695.00 116,090.00 |

-2935.00 -2.44% |

| BRENT CRUDE | 68.72 | 69.41 68.60 |

-0.49 -0.71% |

| RICHARDS BAY COAL MONTHLY | 96.50 | 96.50 96.50 |

0.50 0.52% |

| ROTTERDAM COAL MONTHLY | 104.50 | 104.50 104.25 |

-2.05 -1.92% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.51 | 67.13 66.22 |

-0.47 -0.70% |

| SUGAR #11 WORLD | 16.56 | 16.61 16.25 |

0.26 1.60% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|