PKR in Dismay: No Distance Left to Run

By Nilam Bano | February 03, 2023 at 11:44 PM GMT+05:00

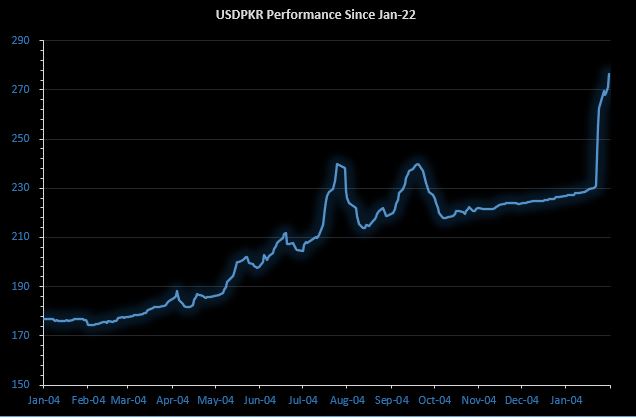

February 03, 2023 (MLN): The Pakistani rupee (PKR) had a rough ride at the beginning of CY23, taking a nosedive and losing a whopping 41 rupees or 18% throughout the trading sessions in January. With reserves dwindling, political turbulence brewing, and a lack of foreign investment and remittances, the local currency found itself in a tight spot.

Stirring the pot, talks with the International Monetary Fund (IMF) were put on hold due to unmet conditions, further impacting the economy. The government's inaction in fixing the IMF program has left the economy in a state of turmoil, causing the rupee to gradually slip against the dollar.

During the earlier sessions, the local unit kept losing ground slowly and gradually against the mighty dollar owing to the continuous decrease in foreign exchange reserves, political instability, absence of fresh inflows, plummeting foreign direct investment, melting remittances, and delay in Pakistan-IMF talks.

Dwindling macros had created enough uncertainty as the foreign exchange reserves melted to a historic low. Meanwhile, the noise over the shortage of dollars and fear of default fueled more chaos throughout the month.

ECs came to the rescue:

In order to mitigate the risk of default, the currency dealers/Exchange Companies (ECs) during the month offered to finance imports of up to $50,000 each, Zafar Paracha, President Exchange Companies Association of Pakistan said in a statement.

Most of the LCs ranged between 5000 to 25000 dollars and the clearing of LCs to help product availably and would to eliminate any shortage, he added.

He also said, “We can easily provide 200 to 300 million dollars to help ease forex reserves.”

He also suggested the government consider a three-tier exchange rate.

“In order to improve foreign exchange reserves while luring dollars, the government should consider the option of a three-tier exchange rate against PKR, export-import bills, and remittances,” he said.

The mentioned measure will motivate the exporter and overseas Pakistani/exchange companies including the home remittance business and de-motivate the elicitor business and import also throughout the non-channelize business, he noted.

Analyst fraternity was of the view that the authorities should not intervene to hold PKR/dollar parity which is one of the major conditions of the IMF for resuming talks for the release of a $1.12 billion tranche.

Let go of the dollar peg which will help remittances and exports perform better, Fahad Rauf, Head of Research at Ismail Iqbal Securities said.

Bangladesh also witnessed a sharp fall in remittances, when the gap between the open market and the official rate rose to 15 Taka per dollar. They increased the exchange rate for remittances, and the impact has been positive, he added.

Dollar shortage amid the absence of foreign inflows through documented channels kept the local unit under pressure. At the same time, dollars in the black market are available at higher rates.

The increasing rates between dollars in the open market and the black market have fueled the panic.

Making the situation worst, there were reports that the commercial banks refused to return the US dollars to depositors of Foreign Currency Saving Accounts (FCA), which is causing turmoil for depositors, Zulfikar Thaver, President of Union of Small and Medium Enterprises (UNISAME) highlighted during the outgoing month.

Banks were saying that they do not have USD, therefore they are unable to return the foreign currency to depositors, and are offering Pak rupee instead of USD at the bank rate of exchange, he added.

Moreover, depositors who requested immediate dollar withdrawals were advised by the bank to wait for two or three days, or else they are being offered Pak currency.

At the same time, the Federal Minister of Finance and Revenue Senator Ishaq Dar denied the government's consideration to access the foreign exchange held by commercial banks.

Removal of Dollar Cap, PKR in search of its true value:

Dropping all the weapons against PKR/USD parity, the authorities finally implemented a market-based exchange range during the last days of the review month.

In continuation of this, ECs on January 24 decided to remove the cap from the dollar in the open market.

The government’s imposition of a cap on the dollar created a black market. Thus, inflows have been reduced from official channels, Malik Bostan President of Forex Association of Pakistan said.

The decision to allow imports of dollars from other sources also increased the rate for Hundi hawala, he noted.

Moreover, he informed the nation that this act will eliminate the black market from the country, as well as the country will see stability in the rupee against the dollar.

According to Malik Bostan, if the dollar supply does not improve, the dollar rate in the open market is likely to shoot up.

Right after this decision, the PKR started collapsing against the greenback on January 25 as the local unit in the interbank depreciated by a massive 24.5 rupees and settled the day's trade at PKR 255.43 per USD, marking a significant drop from the previous closing of PKR 230.89 per USD.

It was the biggest single-session decline was witnessed on October 26, 1998, when the rupee slipped by 9.9%.

However, sources revealed that there were no sellers of dollars in the market. People were more inclined towards dollar buying.

Note that a market-determined exchange rate was one of the main preconditions of the IMF, along with the increase in energy tariffs, revision in Petroleum levy, and hike in interest rates.

As a result of this sharp depreciation, IMF announced a staff mission visit Pakistan on January 31 to complete talks on the ninth quarterly review of a funding program that has been pending for four months.

The Fund's resident representative in Islamabad, Esther Perez Ruiz, stated that the mission will focus on policies to restore domestic and external sustainability in Pakistan, including measures to strengthen the country's fiscal position and support those affected by floods.

Sana Tawfik, Analyst at Arif Habib Limited said, "The State Bank of Pakistan (SBP) had allowed this depreciation of the currency in order to make imports expensive and incentivize exports. As a consequence of continuous PKR depreciation and controls imposed by the Central Bank on imports, the current account deficit came down significantly in 1HFY23, marking a 60% decline.

However, by letting the market determine the exchange rate, pressure on the currency may mount given low reserve levels, she added.

It is important to note that on the last day of the month, the local unit snapped its losing streak and reported a minor gain of 1.7 rupees against the US dollar in today's interbank session as the currency settled the day's trade at PKR 267.89 per USD, compared to previous closing of PKR 269.63 per USD.

This slight appreciation was attributed to the smooth supply of dollars in the market as exporters started offloading dollars due to higher rates.

Meanwhile, the recent talks with IMF brought a sense of stability to the forex market, leading to a correction in exchange rate parity. This was a welcome change after the sharp decline in PKR value against the US dollar in previous sessions.

Gloomy Macros:

Pakistan's economy is feeling the pinch as the country experiences rising economic and political uncertainty.

The latest data released by the central bank showed that the inflow of foreign direct investment (FDI) in the first half of the fiscal year 2023 plunged by 58.7% YoY to $461mn compared to $1.11bn in the same period last year. This drop in FDI was due to a negative inflow in December 2022, with total outflows standing at $17mn.

The current account deficit (CAD) in Pakistan improved by 60%yoy to $3.67bn in the first half of the fiscal year, but in December 2022, the CAD narrowed by 78% year-over-year to $400mn, but worsened by 59% on a monthly basis compared to November 2022. Workers' remittances also took a hit, recording an inflow of $14.1bn in the first half of the fiscal year, which is a drop of 11.1% YoY in December 2022, the inflows stood at $2bn, which is a decrease of 20% YoY and 4.7% MoM.

The decline in remittances is primarily due to the global economic slowdown and the higher cost of living abroad, which has reduced the surplus funds available for remittances. SBP rejected claims that capping the price of the dollar was the sole reason for the decline in exports and remittances and cited several external and domestic factors that have contributed to the decline.

Despite the decline in traditional channels, the foreign exchange inflows through Roshan Digital Account (RDA) have reached $5.68bn by January 2023. However, the inflows are shrinking gradually as the number of inflows is increasing at a decreasing rate.

The foreign exchange reserves held by the SBP recorded a ten-year low and dropped by $592.2mn to stand at $3.08bn at the end of January 2023.

Who will be the net beneficiaries of this freefall?

The recent devaluation of the currency has been a double-edged sword for various sectors in Pakistan. On one hand, it's a shot in the arm for the Exploration and Production (E&P), textile, and Information Technology industries, as their revenue is linked to the US dollar. This means that as the Rupee weakens, their profits will increase.

On the flip side, the devaluation of the Rupee is a body blow for the auto, pharma, and cement sectors, as it will raise the cost of imported raw materials such as steel and coal, which in turn will dent their profit margins.

Additionally, the chemicals sector is also likely to benefit as the cost of imported chemicals, which are used as raw materials, will increase.

However, these industries may be able to soften the blow by passing the increased costs onto consumers. It's worth noting that this negative impact will be limited to industries that use LNG as their main source of energy.

Outlook:

The rupee is expected to remain under fire, as it is predicted to keep weakening, particularly with the country's balance of payments position staying weak for the foreseeable future.

The continued depreciation of the local currency will have far-reaching implications for the economy. In the short term, it could cause imported inflation to skyrocket and could lead to the SBP hiking policy rates more steeply, according to Fitch Solutions.

These factors will only add fuel to the fire of Pakistan's already difficult economic situation. The rating agency expects the economy to shrink by 0.3% in the 2022-23 fiscal year.

On the flip side, the rupee's devaluation will help Pakistan secure more disbursements from the funds, which will be a silver lining for the long-term outlook as it will ease the country's balance of payments strains. The IMF's External Fund Facility agreement requires Pakistan to move towards a market-determined exchange rate regime.

Asad Rizvi, the former treasury head at Chase Manhattan in his video statement said, “The sharp devaluation of the currency is a sign that the government is willing to comply with the conditions set by the IMF in order to restore its bailout package.”

He reassured the public, stating that Pakistan will not default on its financial obligations.

This statement comes as the country continues to face economic challenges, including declining foreign reserves. The government has sought assistance from the IMF to address these issues, and the devaluation of the rupee is seen as a step towards meeting the conditions set forth by the organization.

The government is taking the necessary measures to restore stability to the economy and ensure long-term growth. He also expressed confidence in the government's ability to implement reforms and attract foreign investment.

His statement has been met with cautious optimism by the business community and financial analysts, who are hopeful that the government's actions will lead to a stabilization of the economy and improve the country's financial standing.

Domestically, the PKR's depreciation has also led to an increase in the cost of living for many Pakistanis, as imported goods have become more expensive, adding to the financial burden on households that are already feeling the pinch from rising prices and unemployment.

It's time for the government to take the bull by the horns and take decisive action to restore stability and turn the economy around.

The situation calls for immediate and effective measures to address the underlying economic challenges and regain confidence in the currency markets.

Copyrights Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 132,815.32 80.55M |

-0.44% -587.87 |

| ALLSHR | 83,072.98 453.76M |

-0.14% -115.07 |

| KSE30 | 40,401.98 30.16M |

-0.61% -249.48 |

| KMI30 | 191,023.43 34.36M |

-0.55% -1060.49 |

| KMIALLSHR | 55,745.63 232.57M |

-0.18% -102.07 |

| BKTi | 36,242.17 4.71M |

-0.50% -180.71 |

| OGTi | 28,298.13 6.58M |

-0.49% -139.48 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,095.00 | 109,545.00 108,625.00 |

-120.00 -0.11% |

| BRENT CRUDE | 69.96 | 70.09 69.85 |

-0.19 -0.27% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

2.05 2.15% |

| ROTTERDAM COAL MONTHLY | 106.65 | 106.65 106.25 |

0.50 0.47% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.15 | 68.27 67.78 |

-0.18 -0.26% |

| SUGAR #11 WORLD | 16.15 | 16.37 16.10 |

-0.13 -0.80% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|