Perceptual mapping is the key to Successful Stock Investing

Abu Ahmed | September 07, 2023 at 11:40 AM GMT+05:00

September 07, 2023 (MLN): The article questions the rationale behind institutional investors' belated selling of shares in an extended bearish market.

We witnessed the belated selling of shares in an extended bear market by institutional investors in the past and may witness it in the future as well.

The question is not why Institutional investors sell stocks in a bear market but rather why they resort to belated selling when they could have started it at the start of the bearish cycle.

It raises the question of what compels institutional investors to remain long when the market is gradually slipping to bear. Is it the hope of early recovery of the market or the fear of missing a bull market usually followed by a bear one? Irrespective of the reasons, selling shares by Institutional Investors during tiring times always surprises the market.

In an effort to visualize the rationale behind the belated selling of shares by Institutional Investors in an extended bear market within the context of economic and stock market cycles, the writer came across observations of Mr John Calverley, the Chief Strategist at American Bank and Chairman of the Society of Business Economists.

He wrote in his book “The Investor’s Guide to Economic Fundamentals" that;

“The stock market follows economic cycles; however, the major rise often happens in the middle of the recession or early in the recovery phase when the markets suddenly anticipate an upturn. Similarly, a downturn often happens when valuations are stretched, and the markets suddenly anticipate an economic slowdown or are upset by a political shock.”

The observations of Mr. John Calverley are no way different than what suggests the conventional axiom; that Stock markets boom during economic expansion and fall during an economic contraction, with the only exception that it makes stages of the economic cycle, anticipation of up/down turn in economy, and valuation stretch as a coincidence factor for rise or fall in the stock market cycle rather than a leading factor.

Infographics appearing below sufficiently corroborate that our Stock Market responds to the above factors the way markets around the globe respond in a similar situation, thus corroborating the contention of Mr John Calverley in verbatim.

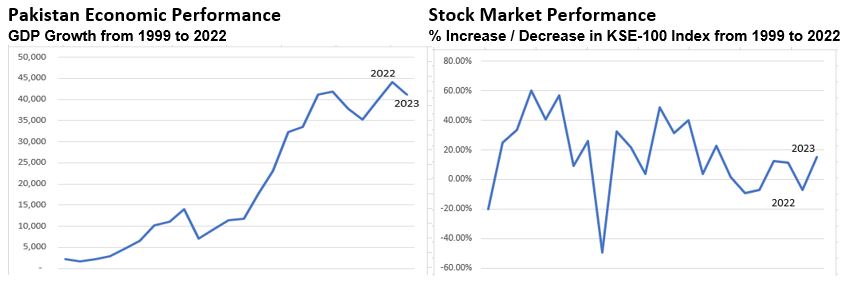

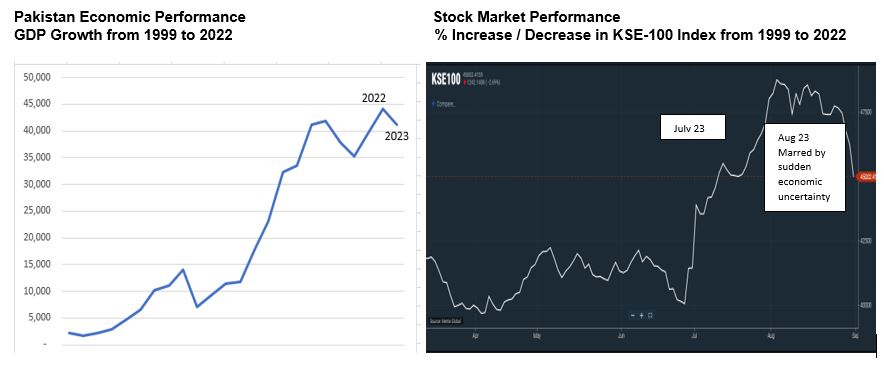

The year 2023 happens to be a period of extreme economic uncertainty for Pakistan. It is marred by fear of default on foreign debts, rising inflation, increasing policy rates, unprecedented weakening of PKR against US dollars, and slow economic growth. Together, they cast a gloomy picture of the economy during the first half of the fiscal year, caused the benchmark index to crawl to =42,000= level, and forced it to stay there for an extended period. However, once the fear of default disappeared with the signing of the $3 billion Stand-By Arrangement with IMF, the Stock Market took a sharp recovery and ended with a straight gain of = 9,000= points within a few days with technical correction in between even the actualization of economic benefits yet to realize.

Nothing, but the changes in economics drove the market to peak at = 49,000 levels.

Similarly, the stock market took a nosedive once hope for economic recovery dwindled. There was hardly a gap between the timing of the nosediving and reporting of the Caretaker Finance Minister about the shambled state of the economy with the admission of the absence of any fiscal space to manoeuvre the economy to steer out of the crisis.

It validated the later part of Mr. John Calverley contention too that;

“A downturn in the market often happens when valuations stretched, and the markets suddenly anticipate an economic slowdown or are upset by a political shock”.

It would be naïve to think of ignorance or the inability of institutional investors to conjure up the relationship between the economic and stock market cycle when they have the privilege of knowledge, skills, and technology for assessing market direction ahead of time.

Therefore, instead of finding rationale in the belated selling of shares in an extended bear market by institutional investors, accepting eco-politico as a co-incident indicator for the stock market and mapping eco-political ramifications of the same on the stock market performance would be a more logical initiative.

Conjuring up such a perceptual model will be a reality once Institutional Investors, Capital Market Custodians, and Academicians join hands for the cause.

An aspect perhaps where we lack as investors that why Top Line Security adopted “Stay Ahead of Curve” as a business slogan.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|