Pakistan vs COVID-19 – A ‘do or die’ situation?

By MG News | April 14, 2020 at 12:29 PM GMT+05:00

April 14, 2020 (MLN): The COVID-19 virus, now considered a pandemic, has engulfed economies across the world into its inferno. As a result, several industries have suffered irrecoverable damages whereas others have gone bankrupt.

Pakistan’s economy is no exception to this. While most of the provincial governments have implemented lockdown in their respective states, the country is still facing an immense dilemma as it cannot afford to continue being on lockdown, especially when the economy is already at its worst.

Following is an analysis of how the major industries of Pakistan are holding up, and how their future is going to be impacted if the lockdown continues, and when it is lifted.

Fertilizer Sector

The sale of urea sales during March 2020, is likely to decline substantially owing to lockdowns across the country amidst the COVID-19 outbreak. Amongst the companies, Fauji Fertilizer (FFC) and Fauji Fertilizer Bin Qaim (FFBL) are expected to post an increase in urea sales during March, while Engro Fertilizer is anticipated to post decline due to its higher prices compared to its peers.

To recall, EFERT had further reduced the prices of urea by Rs240/bag to pass on the full impact of GIDC on the consumers. Similarly, FFC also reduced urea prices by Rs23/bag.

Despite the lockdown, urea production in Mar-2020 remained unaffected and is expected to remain unchanged at 495k tons, taking urea closing inventory to around 585k tons.

Automobile Sector

The latest data released by the Pakistan Automotive Manufacturers Association (PAMA) shows that the sale of passenger cars fell by around 71 percent on a year-on-year basis, and 44 percent on a month-on-month basis.

This shows that the Auto sector has suffered badly at the hands of the ongoing Pandemic, which has caused a lockdown for many auto companies across the country.

With the outbreak of COVID-19, things have just gone uglier for the Auto Sector which was already on a verge of collapse. The sector already faced several challenges including the high cost of financing and decline in the disposable incomes of consumers.

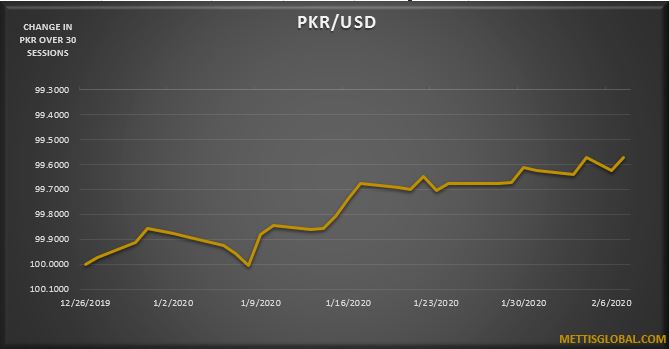

Even if the lockdown was to be lifted soon, the chances of which are very low, the Auto Sector shall still suffer in the form of slower sales. Similarly, once the lockdown is lifted, the sector will be facing another challenge i.e. PKR depreciation. The very reason why auto companies are suffering in the first place is because of the continuous price hiking done in the previous year. If PKR depreciates further, the companies will have to raise the prices further, which would not be well received by the public whose buying power has been tarnished already by this lockdown.

Cement Sector

Just like any other sector, Cement Industry is also feeling the brunt of this lockdown but on a slightly higher level. The COVID-19 pandemic has changed the entire game for the sector, that had just started to perform better.

Likewise, the construction sector is in no good shape either. The announcement of relief package may have provided some relief but hasn’t done anything in practice as the demand for cement has taken a freefall owing to the lockdown being observed throughout the country.

The only thing that the industry may have benefitted from this entire situation, is the cut in the Policy rate by 225 bps, which will ease the company off of higher borrowing cost.

However, a report by Insight Securities has said that when it comes to earnings and valuations, the Cement Sector is still not on its lowest yet, as the sector is backed by leveraged balance sheets, weak PKR, and slowdown in demand.

The report has further said that the demand for cement shall be dented in the upcoming months, as the outbreak of COVID-19 might compel the government to cut its PSDP budget. This is because the demand for cement is directly linked to development spending, so if there’s a cut in spending on public infrastructure, the Cement sector shall suffer.

Commercial Banks

While the measures taken by the Government may have managed to provide some respite to the rest of the sectors, the same cannot be said for Commercial Banks. The slashing of the Policy Rate by 225 bps has put a big question mark on the future earnings and growth of the sector.

Furthermore, the halt in business activities as a result of country-wise lockdown has added to the woes of the Banking industry. According to the research conducted by AKD Securities, the earnings through trade remittances and commissions are likely to take a serious hit, whereas advances are expected to show some growth as soon as businesses around the country resume operations.

Sharing the outcome of a stress testing applied to all Commercial Banks for the earnings outlook, the report stated that NBP and BAHL were the most vulnerable to credit shock whereas MCB and ABL were the safest.

Further comparing the performance of the sector to that witnessed in CY08, the report said that the banking sector is relatively better positioned right now due to improvement in quality and performance of liens, relaxations granted by the State Bank on NPL classification, and a higher share of Government Loans.

Since one does not know for how long the pandemic is going to last, and when the lockdown is going t be lifted, it would be difficult to project how and when the banking sector, or any other sector for that matter, would enter the recovery phase.

Oil & Gas Marketing Companies

The sale of POL products for the month of March 2020 suffered massive declines as a result of lower demand amidst the ongoing lockdown. If the lockdown is extended further with the operations remaining on a standstill, it is expected that the sale will decline even further, causing irreparable damage to the industry.

As per the report published by BIPL Securities, the continuous extraction of hot money from T-Bills and PIBs has caused the PKR to depreciate massively, which in turn has put the OMC industry on the brink of incurring large exchange losses. Within the sector, PSO, APL, and HASCOL are likely to be the most vulnerable to a decline in the value of the local currency.

However, given that the Economic Coordination Committee (ECC) decides to incorporate the exchange loss component in petroleum prices, the OMCs can be saved from suffering high losses.

Besides, the sector has gained some relief from the monetary easing, especially to those companies operating on high leverage such as PSO and HASCOL.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 130,686.66 280.01M |

0.26% 342.63 |

| ALLSHR | 81,305.25 897.01M |

0.35% 281.26 |

| KSE30 | 39,945.45 114.02M |

0.09% 37.19 |

| KMI30 | 190,698.05 148.61M |

0.61% 1163.05 |

| KMIALLSHR | 55,074.15 495.43M |

0.53% 290.50 |

| BKTi | 34,568.40 28.73M |

-1.07% -372.33 |

| OGTi | 28,739.35 22.59M |

1.57% 443.29 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 110,145.00 | 110,525.00 110,055.00 |

-270.00 -0.24% |

| BRENT CRUDE | 68.65 | 68.89 68.64 |

-0.15 -0.22% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

-0.75 -0.76% |

| ROTTERDAM COAL MONTHLY | 108.45 | 109.80 108.45 |

-0.55 -0.50% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.93 | 67.18 66.92 |

-0.07 -0.10% |

| SUGAR #11 WORLD | 16.37 | 16.40 15.44 |

0.79 5.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|