MPS Preview: Will SBP Cut Rates or Play It Safe?

Nilam Bano | May 05, 2025 at 01:30 PM GMT+05:00

May 05, 2025 (MLN): The clock is ticking down to the State Bank of Pakistan’s monetary policy decision today, and the uncertainty hangs thick in the air. The market sentiments remain divided on whether the central bank will cut rates by 50 basis points or simply hold its ground.

According to a recent survey conducted by Mettis Global, 50% of the respondents are betting on a 50bps rate cut, mainly because inflation has been cooling off. Not to forget, April’s inflation dropped to just 0.3%, and the bigger picture shows a clear disinflation trend.

With CPI expected to remain low over the next year, there is a strong case for easing policy without jeopardizing macroeconomic stability.

However, core inflation tells a different story. It rose by 1.2% in April, while headline inflation fell by 0.8%. Additionally, the external side of the economy cannot be overlooked. The SBP expects reserves to rise to $14 billion by June-end, supported by anticipated IMF inflows next week.

However, the import bill of $5.5 billion in April, which pushed the trade deficit to its highest level since September 2022, will add further pressure.

Most importantly, the IMF review is around the corner, and global uncertainties like US trade policies and Indo-Pak tensions have not settled yet. In fact, the IMF has already stated that Pakistan needs to keep its policy tight to keep inflation in check.

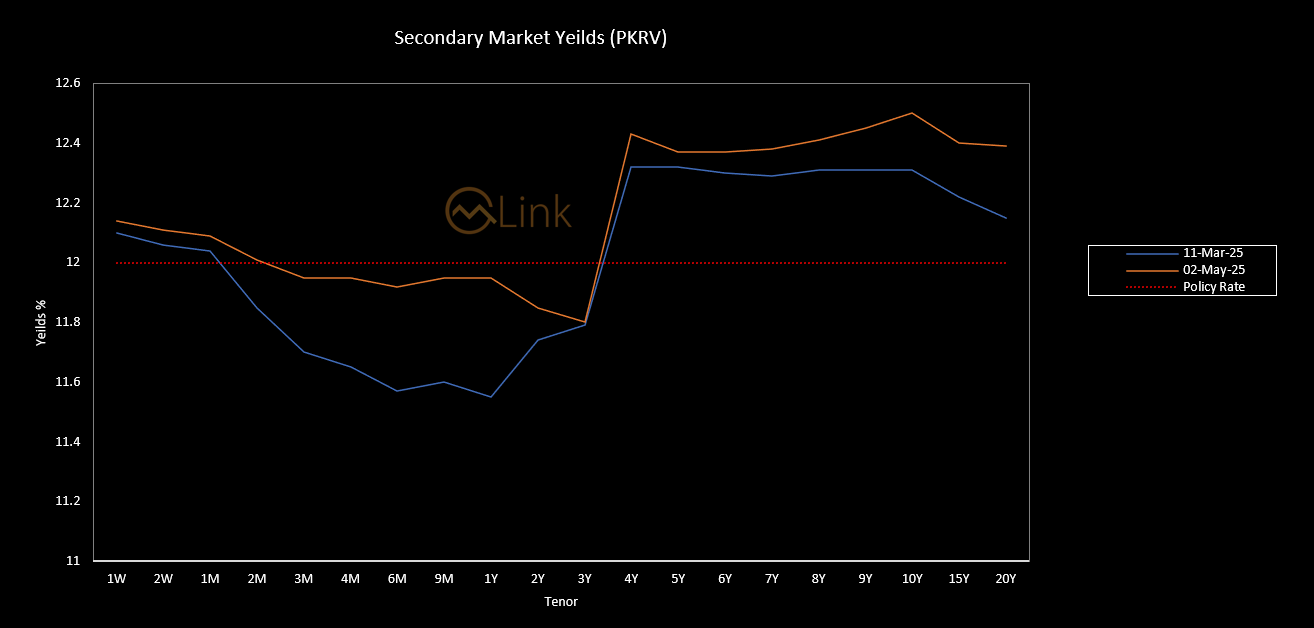

Secondary Market Yields

Since the last MPC meeting, the secondary market has experienced a notable rise in yields across all tenors. The 6M and 9M yields surged by 35 bps each, while the 1-year tenor increased by 40 bps.

Medium-term tenors also saw gains, with the 2-year and 4-year yields rising by 11 bps each, respectively. Long-term yields remained relatively stable, with the 10-year up by 19 bps, the 15-year up by 18 bps and the 20-year by 24 bps.

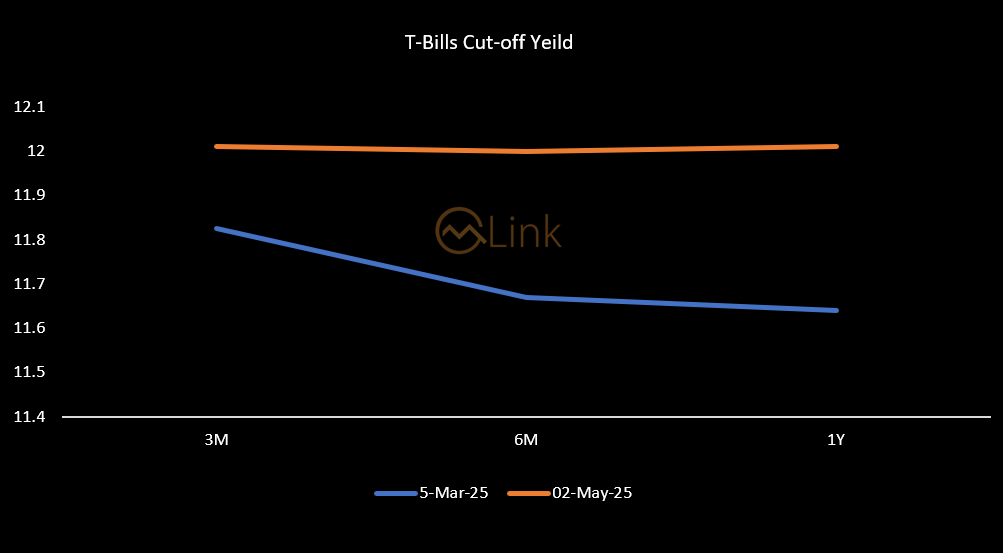

T-Bill Yields

Market Treasury Bills (MTBs) have also exhibited notable shifts. The Cut-off yields increased to 12.0098% for 3 months, 11.9998% for 6 months, and 12.01% for 12 months.

Since the last MPC meeting, a significant increase was observed in the 12M T-bill yield (+37 bps) and 6M yield (+32.99 bps) compared to the 3M (+18.51 bps).

These shifts in yields, particularly in the T-bills, signal growing expectations of a cautious approach from the central bank in its upcoming monetary policy decision.

Last time, the MPC kept the policy rate unchanged at 12%, effective March 11, 2025, in contrast with market expectations.

The Committee noted that inflation in February 2025 turned out lower than expected, mainly due to a drop in food and energy prices. Notwithstanding this decline, the Committee assessed the risks posed by the inherent volatility in these prices to the current declining trend in inflation.

SBP further noted that core inflation remains elevated and stickier than expected, with mixed inflation expectations from consumers and businesses. As a result, the Committee anticipated inflation to decline further before gradually stabilising within the 5%-7% target range.

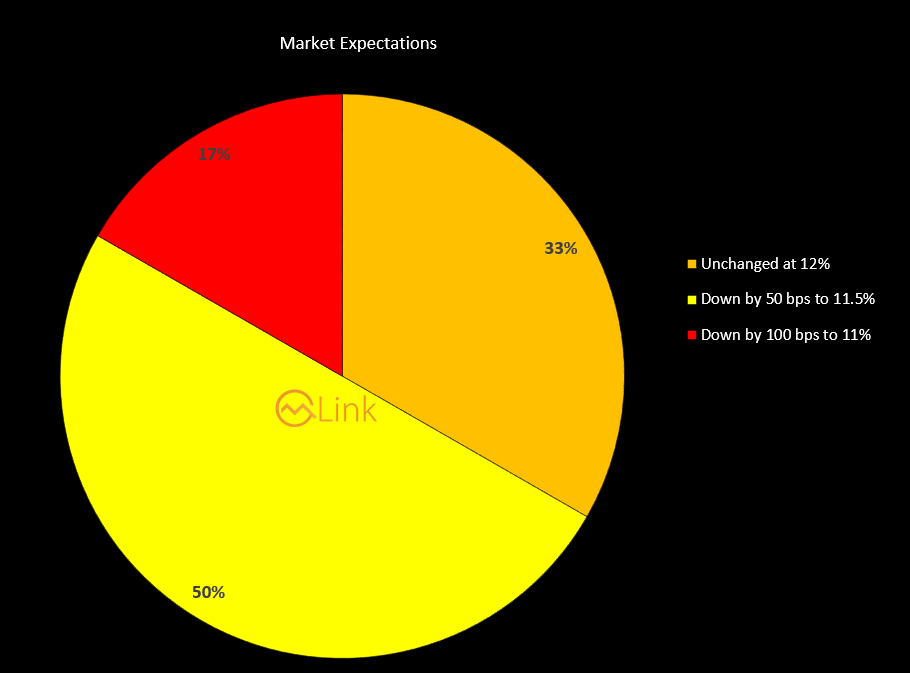

Survey Result

To gauge market expectations for today’s monetary policy meeting, Mettis Global surveyed various sectors, revealing divided market sentiment.

A significant 50% of respondents believe that the central bank will maintain the current rate at 12%, indicating the continuation of the bank’s cautious policy stance.

Meanwhile, 33% of participants anticipate a 50 basis-point cut to 11.5%. A smaller yet notable 17% foresee a more aggressive policy move, predicting a 100 basis-point reduction to 11%. Such a cut would signal a stronger monetary easing stance, possibly in response to heightened concerns over growth or liquidity constraints.

Copyright Mettis Link News

Related News

.jpg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,571.27 436.67M | 1.06% 1878.35 |

| ALLSHR | 108,600.94 844.23M | 1.00% 1073.54 |

| KSE30 | 53,548.42 162.02M | 0.99% 525.53 |

| KMI30 | 256,725.70 154.74M | 0.76% 1936.43 |

| KMIALLSHR | 70,620.69 563.61M | 0.98% 683.55 |

| BKTi | 48,625.03 36.31M | 1.37% 658.39 |

| OGTi | 37,179.52 8.29M | 0.94% 345.85 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 60,210.00 | 60,895.00 59,790.00 | 215.00 0.36% |

| BRENT CRUDE | 73.08 | 75.13 71.38 | -2.18 -2.90% |

| RICHARDS BAY COAL MONTHLY | 103.50 | 0.00 0.00 | 0.25 0.24% |

| ROTTERDAM COAL MONTHLY | 113.35 | 114.25 113.00 | -0.05 -0.04% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 70.24 | 71.86 68.56 | -1.68 -2.34% |

| SUGAR #11 WORLD | 14.55 | 14.68 14.02 | 0.45 3.19% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|