Loan demand remains strong in Q3FY25

MG News | May 08, 2025 at 08:27 PM GMT+05:00

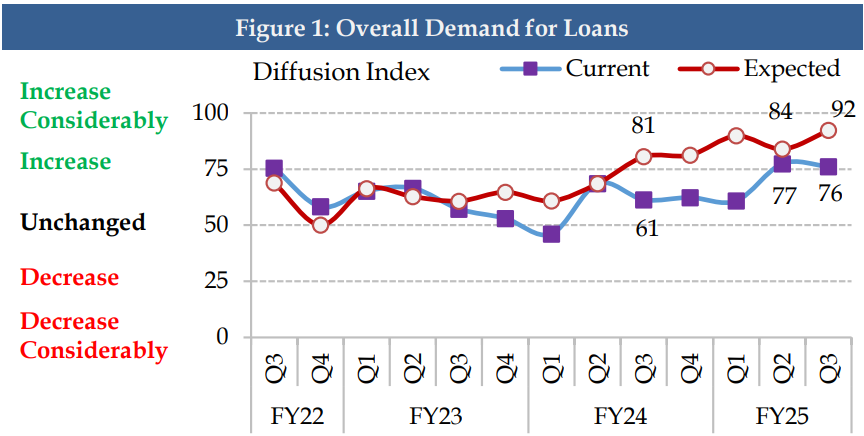

May 08, 2025 (MLN): Current loan demand remained stable at 76 in the " Increase Considerably " zone in Q3FY25 compared to 77 in the previous quarter, according to the latest Bank Lending Survey (BLS) for Q3-FY25, conducted by the State Bank of Pakistan (SBP)

Meanwhile, future loan demand is expected to rise 92 compared to 84 in the previous quarter, primarily due to monetary policy decisions.

This trend continues the upward trajectory observed in previous quarters, primarily driven by monetary policy decisions and increased financing needs across various sectors.

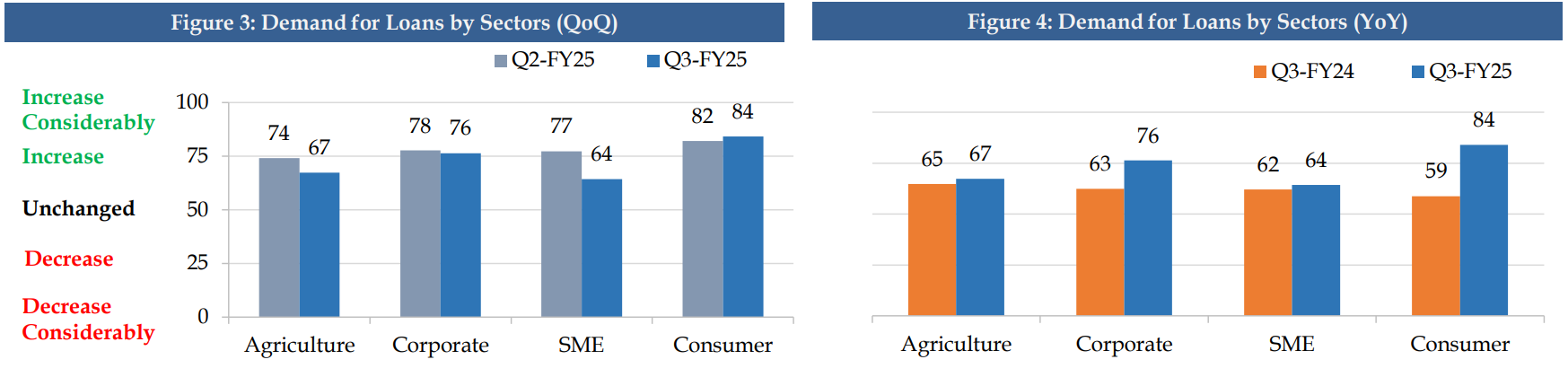

Sector-Wise Growth

A sectoral breakdown shows corporate loan demand rising to 76 (YoY), SME demand reaching 64 (YoY), and agriculture loans maintaining steady growth at 67 (YoY).

Meanwhile, consumer loan demand has jumped significantly, reaching 84 (YoY), reflecting increased borrowing appetite.

While quarterly comparisons (QoQ) indicate slight dips in Agriculture, Corporate, and SME sectors.

Loan Applications

The number of loan applications has risen sharply, aligning with anticipated future demand, while the cost of borrowing continues to decline, entering the "Decrease" zone since Q3-FY24.

Meanwhile, expected fund availability has reached "Increase Considerably" levels, supported by monetary policy adjustments.

Borrowing Costs

At the same time, the cost of borrowing has entered the “Decrease” zone since Q3-FY24, marking a notable easing in financial pressures. Expected borrowing costs have declined to 14 in Q3-FY25, offering relief to businesses and consumers seeking credit.

The lower borrowing costs are attributed to monetary policy changes, competition among banks, and fluctuations in deposit volumes.

Overall availability of expected funds reached “Increase Considerably” territory, whereas current availability of funds hovered in the upper zone of “Increase” territory, mainly on account of monetary policy decisions.

Key Drivers

The survey also highlights key factors influencing fund availability, with monetary policy decisions maintaining a diffusion index of 73, slightly lower than 78 in Q2-FY25 but significantly higher than 33 in Q3-FY24, indicating continued central bank support for credit expansion. The bank liquidity position also remains robust at 65, ensuring a stable flow of credit in the market.

Government borrowing, which was 56 in Q2-FY25, declined to 49 in Q3-FY25, suggesting a slight reduction in fiscal-driven credit pressures. Meanwhile, non-performing loans (NPLs) have increased from 39 in Q2-FY25 to 48 in Q3-FY25, potentially impacting credit accessibility in the long run.

Competition among banks has marginally intensified, with the diffusion index rising to 49, while the volume of deposits has remained steady at 64, reinforcing liquidity stability.

The macroeconomic situation remained a key determinant, although its influence slightly eased from 62 in Q2-FY25 to 51 in Q3-FY25.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 173,518.82 409.23M | -3.56% -6408.23 |

| ALLSHR | 105,463.40 895.64M | -3.48% -3807.29 |

| KSE30 | 51,709.62 172.22M | -3.72% -1996.09 |

| KMI30 | 244,367.91 157.85M | -3.61% -9164.01 |

| KMIALLSHR | 67,803.26 534.35M | -3.35% -2349.37 |

| BKTi | 49,017.52 55.15M | -3.88% -1979.98 |

| OGTi | 34,971.98 16.59M | -3.44% -1244.10 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,650.00 | 65,450.00 61,925.00 | 2300.00 3.69% |

| BRENT CRUDE | 84.54 | 87.55 83.37 | 1.24 1.49% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.30 -1.21% |

| ROTTERDAM COAL MONTHLY | 119.00 | 119.50 118.50 | -0.50 -0.42% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 79.00 | 81.27 77.84 | 0.86 1.10% |

| SUGAR #11 WORLD | 14.92 | 15.00 14.67 | 0.17 1.15% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|