Inflation set to stabilize at 7%, lowering borrowing costs

MG News | January 28, 2025 at 01:37 PM GMT+05:00

January 28, 2025 (MLN): Inflation is expected to stabilize near the long-term average of 7%, fostering conditions conducive to economic activity.

This anticipated stability will likely facilitate a further reduction in policy rates, lowering borrowing costs for both businesses and consumers, as revealed in the half-yearly report, "State of Pakistan's Economy," by the Finance Division.

Such a shift is expected to boost investment and economic momentum, particularly in LSM and services, which are key growth drivers this year.

Remittance inflows are expected to maintain their upward trend, contributing to a more stable external account and boosting household consumption.

On the fiscal side, a significant decline in markup expenditures, supported by reduced borrowing costs, will enhance fiscal sustainability.

The overall economic outlook for Pakistan remains encouraging due to stabilizing macroeconomic fundamentals and the gradual recovery of key sectors.

Pakistan's economy, after contracting by 0.2% in FY2023, recovered with a 2.5% growth in FY2024 and continued to improve in H1FY2025, building upon the stabilization achieved in FY2024.

The positive momentum has been fueled by sound macroeconomic management, effective inflation control measures, and enhanced fiscal and external account stability.

Agriculture has shown a growth of 1.15% in Q1 as compared to 8.09% in the same period last year, the report added.

The growth in important crops contracted by 11.19% in Q1 due to the high base effect in the crop sector of the last fiscal year and the decline in the crop production of cotton (-29.6%), rice (-1.2%), sugarcane (-2.2%) and maize (-15.6%).

Although important crops comprise wheat, cotton, rice, maize, and sugarcane, however, in Q1 there is no impact from wheat as it is neither sown nor harvested during this quarter.

Other crops have witnessed 2.08 % growth in Q1 as compared to -2.08 % last year. Livestock has increased by 4.89 % as compared to 4.56 % last year because of a decrease in inputs (dry fodder).

Forestry and fishing have retained their normal growth tendency and witnessed modest growth of 0.78 % and 0.82 %, respectively.

In Q1FY2025, the government remained committed to support agriculture by ensuring the timely availability of farm inputs for Kharif crops.

The allocation of Rs23.9 billion under PSDP in FY2025 underscores the government’s strategic focus on productivity enhancement and sector modernization.

Agricultural credit disbursement rose significantly by 24.8 % in FY2024, reaching Rs2,216bn, which helped farmers to manage input costs and improve productivity.

This upward trend is expected to continue, with agriculture credit expansion target of Rs2,572.3bn for FY2025, the reported noted.

During Jul-Nov FY2025, agriculture credit disbursement recorded Rs925.7bn compared to Rs853bn same periods last year showing an increase of 8.5 %.

Imports of agricultural machinery surged by 46.8 % in H1-FY2025 to $53.7 million, reflecting a shift toward mechanization and improved efficiency.

Conversely, insecticide imports declined from $94.9mn to $66.5mn, indicating the need to enhance crop protection measures.

Similarly, the fertilizer offtake during the Kharif sowing season of 2024 showed a decline, with urea offtake falling by 17.3% to 2,746 thousand tonnes and DAP offtake down by 15.3% to 642 thousand tonnes.

These declines were driven by delayed sowing due to climate variations, shifts in crop acreage, and lower wheat prices, which affected farmers’ purchasing power.

For the Rabi 2024-25 season, urea offtake during October-December 2024 was 2,003 thousand tonnes, an 18% increase compared to October-December 2023, while DAP offtake was 690 thousand tonnes, 19.5% higher than the same period in 2023.

The higher fertilizer offtake can be attributed to the disbursement of interest-free loans to small farmers by the Punjab Government through the Kissan Card for the purchase of agricultural inputs, such as seeds and fertilizer.

The irrigation system was pivotal in supporting Kharif 2024 crops despite challenging climatic conditions.

The Indus River System Authority (IRSA) reported water supply at 60.48 MAF, slightly below the 61.85 MAF recorded in Kharif 2023.

The industrial sector experienced a contraction of 1.7% in FY2024, attributed to stabilization measures, a tight monetary policy stance, elevated inflation rates, and an unstable exchange rate.

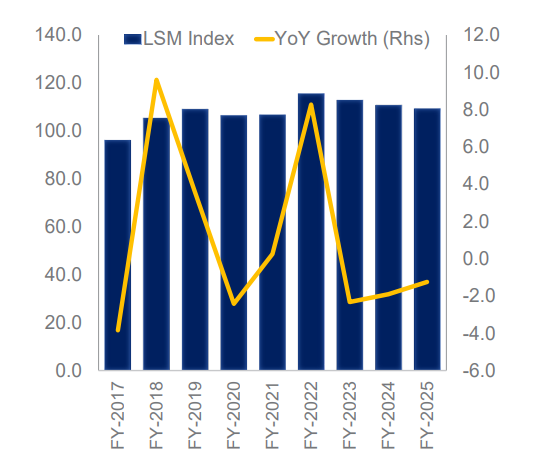

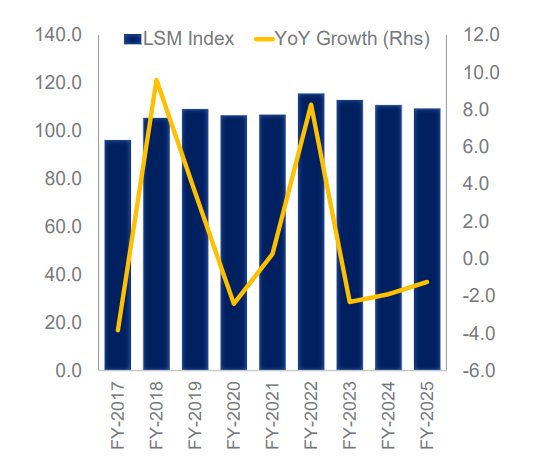

LSM sustain growth of 1% in FY2024. In Q1FY2025, the industrial sector contracted by 1.03%, showing improvement compared to a substantial contraction of 4.43% in the same period last year.

This recovery was largely attributed to growth in manufacturing, as well as electricity, gas, and water supply.

However, downside risks persist in Mining and Quarrying, which declined by 6.49%, and Construction, which contracted significantly by 14.91%.

During Jul-Nov FY2025, the LSM sector experienced a slight decline of 1.25%, compared to the contraction of 1.9% recorded during the same period last year.

In November 2024, LSM witnessed a contraction of 3.81% on YoY basis and 1.19% on MoM basis.

Figure 1: Performance of LSM Index and growth (Jul-Nov)

Economic activity within the textile sector, which constitutes 18.2% of the LSM output, showed signs of recovery.

Following a steep contraction of 12.7% in Jul-Nov FY2024, the sector rebounded with a 2.3% growth in Jul-Nov FY2025.

Figure 2: Sectoral performance of LSM

The automobile industry demonstrated a remarkable recovery during Jul-Dec FY2025.

Total vehicle production surged by 28.3%, while sales grew by 28.2% compared to the same period in FY2024.

November 2024 marked a significant milestone for Pakistan’s automotive and green energy sectors, with Dewan Motors commencing local production of electric vehicles (EVs).

The cement industry demonstrated a mixed performance during Jul-Dec FY2025, with total dispatches reaching 22.9mn tonnes, marking a 4% decline from the same period last year.

Domestic dispatches dropped by 10.4% to 18.1mn tonnes, reflecting weak local demand amid subdued construction activity and rising input costs.

In contrast, cement exports showed significant growth, increasing by 31.7% to 4.8mn tonnes during the period.

In FY2024, the Services Sector rebounded from a marginal contraction of 0.02% in FY2023 to achieve a growth rate of 2.2%, demonstrating resilience amid challenging economic conditions.

This recovery set a positive trajectory for FY2025, however, in Q1 FY2025, the growth moderated to 1.43% from 2.16% last year.

The drop in services growth is largely attributed to a slowdown in wholesale & retail trade and transport & storage.

Trade volume in services (encompassing both exports and imports) grew by 8.3% in Jul-Dec FY2025, supported by expansion in the Information & Communication sector, a cornerstone of Pakistan’s transition toward a digital economy.

Furthermore, remittance inflows saw a notable surge of 32.8% during Jul-Dec FY2025, enhancing household incomes and stimulating consumer spending across retail businesses and other private services.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 155,777.21 362.16M | -0.86% -1354.88 |

| ALLSHR | 92,994.52 618.17M | -0.61% -572.34 |

| KSE30 | 47,890.76 137.48M | -0.85% -412.22 |

| KMI30 | 220,015.06 115.60M | -0.35% -783.45 |

| KMIALLSHR | 59,910.72 260.41M | -0.13% -77.81 |

| BKTi | 45,388.60 42.55M | -1.74% -804.48 |

| OGTi | 30,631.34 29.10M | 1.45% 438.24 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 72,065.00 | 72,235.00 67,615.00 | 3600.00 5.26% |

| BRENT CRUDE | 82.77 | 84.48 81.28 | 1.37 1.68% |

| RICHARDS BAY COAL MONTHLY | 99.40 | 0.00 0.00 | -17.10 -14.68% |

| ROTTERDAM COAL MONTHLY | 124.00 | 124.00 124.00 | -4.00 -3.13% |

| USD RBD PALM OLEIN | 1,083.50 | 1,083.50 1,083.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 75.61 | 77.23 74.37 | 1.05 1.41% |

| SUGAR #11 WORLD | 14.01 | 14.06 13.93 | 0.08 0.57% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|