IMS lowers CY25/26f earnings by 8%, ups TPs 4% on stronger ROE outlook

MG News | April 08, 2025 at 10:24 AM GMT+05:00

April 08, 2025 (MLN): Intermarket Securities Limited (PSX: IMS) has revised its earnings estimates by incorporating updated assumptions on interest rates, provisions, and capital gains.

IMS's CY25/26f earnings estimates have been lowered by approximately 8%, but target prices are up by 4% due to higher terminal-year ROE projections.

Pakistan is complying with the IMF program and sustaining macroeconomic discipline.

US reciprocal tariffs may ultimately have a negligible headline impact given that Pakistan’s petroleum imports are the same as textile exports; both c. 4% of GDP.

The house sees normalized loan growth outpacing nominal GDP, with the cost of risk expected to remain in control.

Bank's universe trades at a CY25f P/B of 1.2x, but this masks HBL and BAFL that are trading at 0.6x P/B and offer strong rerating potential.

Sector dividend yields are in double digits, giving downside protection even in a more risk-off setting for equities.

Notable changes to IMS’s assumptions include a lower policy rate of 11.75% for CY25f vs. 12% earlier, some relief for Islamic banks in asset yield calculations, and higher capital gains going by large unrealized gains at end-CY24.

IMS keeps the tax rate constant at 52% across the projection horizon, even though this is much higher than the 10-year average of 43%.

Individual banks see their dividend payout expectations remain intact despite lower CY25f earnings, but UBL sees an increase given its strong CAR and likelihood of maintaining earnings in the near term.

The house also incorporates the acquisition of SILK for UBL, with provisions and tax rate the prominent affected line items (provisions to initially spike before recoveries kick in; SILK’s tax losses expected to be utilized in CY25/26f).

Earnings for IMS’s covered banks doubled between 2022 to 2024, largely on margin expansion as the policy rate rose to a record high 22%.

Now, with the policy rate having come off to 12% (10-year average is 10.9%), banks are likely to turn more aggressively towards volume growth to offset margin compression.

IMS see normalized loan growth at c. 15% pa going forward, greater than nominal GDP growth.

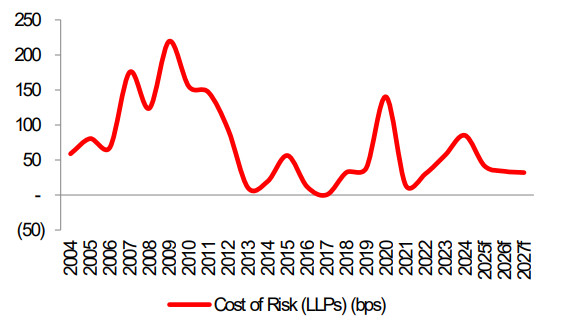

Importantly, asset quality should remain in control - LLPs more than doubled in 2024, but this was a result of IFRS-9 implementation and should not repeat to the same extent going forward.

The cost of risk is expected to come off to 45bps/35bps in CY25/26f (vs. about 90bps in CY24) before settling at c. 25bps over the medium term.

IMS has not built in any exceptional provisions for Textiles (15% of loan books; 50% of exports) as the 29% reciprocal US tariff on Pakistan is lower than for several competing textile exporters, e.g. Bangladesh, Vietnam, and China.

The brokerage house perceives several tailwinds for Pakistan banks over the medium term.

These include growing digital transactions, which account for 84% of volume but only 17% of value.

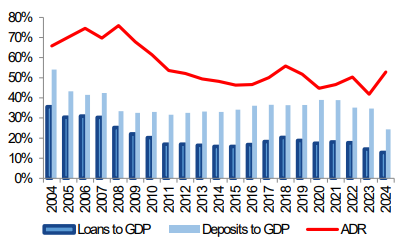

Additionally, there is potential for a step increase in deposits-to-GDP (currently around 30% compared to over 45% in the mid-2000s), driven by efforts to document the economy and the planned full conversion to an Islamic system by end-2027.

Additionally, there is potential for taxation on banks to come down as the government’s finances improve, supported by ongoing efforts to broaden the tax base.

Banks offer double-digit D/Ys, which should result in downside protection even if global equities remain under pressure.

That said, there is a wide disparity in other valuation multiples, such as P/B and P/E.

The house’s preference is for banks with the most re-rating potential. HBL and BAFL, accordingly, emerge as top picks.

IMS incorporate a lower policy rate of 11.75% for CY25f vs. 12% earlier, softer loan provisions on an improved economic outlook, and higher investment gains in CY25f based on Dec’24 unrealized balances.

The policy rate has reduced from an all-time high of 22% in May’24 to 12% at present.

IMS CY25/26f average policy rate assumptions are now 11.75%/10.5% compared to 12.0%/10.5% previously.

However, NIMs for the IMS Banks Universe are slightly higher now at 6.1%/6.0% in 2025/26f vs. c 5% previously.

This is driven by normalizing NII for banks such as UBL as negative carry on OMOs ends, while Islamic banks see some relief on asset yield calculations (in turn tied to the minimum deposit rate on their savings deposits).

Banks have also focused on current accounts in their deposit mix, which is beneficial for NIMs.

Several banks took advantage of rapidly falling interest rates by appropriately and aggressively positioning their investment books, resulting in large unrealized capital gains.

This, together with improving fee income lines, should help partially offset margin compression in CY25f (CY24 NIMs clocked in at 7.6%).

Pakistan banks adopted IFRS-9 in CY24, which affected provisioning/impairment.

LLP provisions more than doubled in CY24 but are expected to significantly decelerate in CY25f.

The brokerage house’s project cost of risk is at c. 45/35bps in CY25/26f compared to c. 60/40bps previously.

IMS has not built in any exceptional provisions for Textiles (15% of loan books; 50% of exports) as the 29% reciprocal US tariff on Pakistan is lower than for several competing textile exporters.

Copyright Mettis Link News

Related News

_20260807191109787_a461a8.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,210.00 | 65,280.00 65,035.00 | 35.00 0.05% |

| BRENT CRUDE | 82.38 | 84.44 81.50 | -0.11 -0.13% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 105.50 105.50 | -0.25 -0.24% |

| ROTTERDAM COAL MONTHLY | 116.25 | 117.00 116.25 | -0.10 -0.09% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 77.08 | 78.77 76.53 | -0.21 -0.27% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|