IMF urges better cash management to cut Pakistan’s borrowing

MG News | February 04, 2025 at 01:08 PM GMT+05:00

February 04, 2025 (MLN): To reduce the broader public sector’s borrowing needs and limit the sovereign-bank nexus in Pakistan, it is essential to improve cash management within the government and its entities, particularly by making better use of idle cash balances.

Additionally, public debt management should be guided by a robust medium-term strategy aimed at diversifying the investor base while carefully managing the cost-risk profile of public debt.

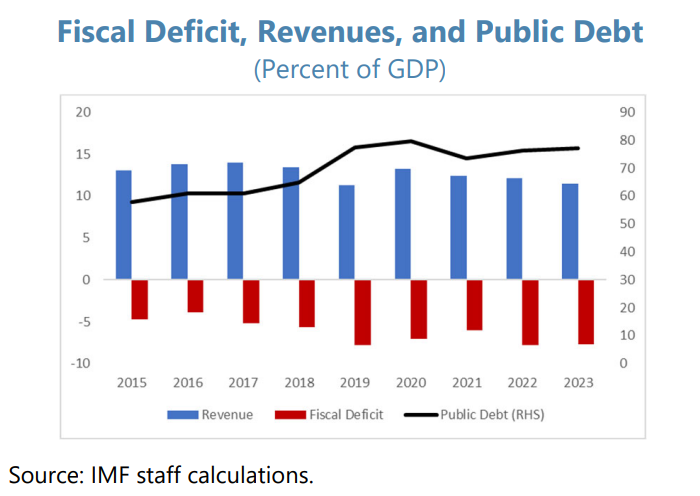

This includes prudent advance planning for the State Bank of Pakistan's (SBP) bullet repayment in 2029, especially as public debt reached nearly 80% of GDP in 2023.

Persistently high fiscal deficits over 7% of GDP since 2019 and limited external funding have led to increased reliance on the banking sector for government financing, according to a report by the International Monetary Fund (IMF) titled "The Sovereign-Bank (-Central Bank) Nexus in Pakistan".

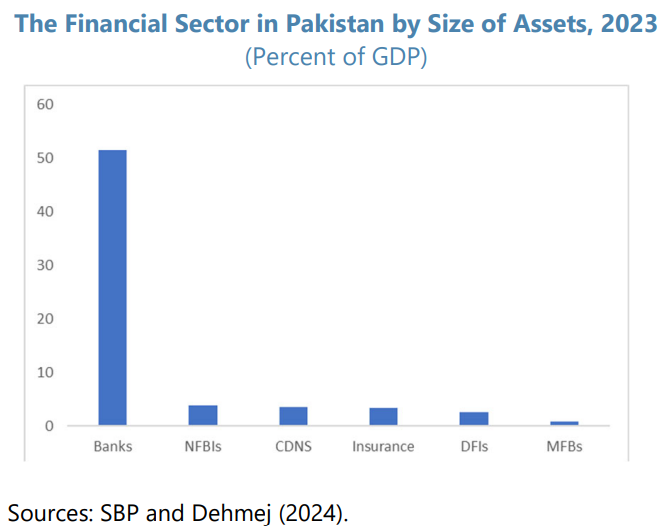

Banks’ holdings of domestic government debt have surged to around 60% of their assets, more than thrice the average for Emerging Market Economies, (EMEs).

Capital market development and the growth of domestic institutional investors will deepen the market for risk-free assets, leaving the banks to concentrate on financing the private sector.

The sovereign-bank nexus creates negative feedback loops, any concerns about sovereign debt sustainability can impact banking sector stability and vice versa.

The SBP’s efforts to meet the liquidity needs of the sector indirectly increases its interconnection with both commercial banks and the government.

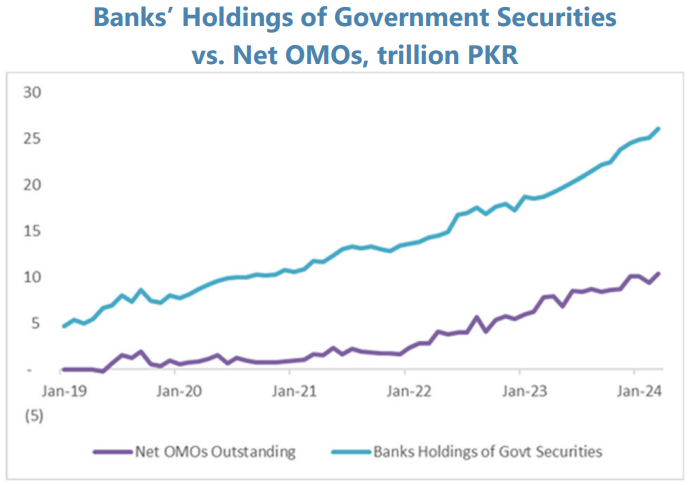

This was mainly achieved through OMOs, accepting government securities as collateral in 7- to 28-day reverse repo transactions.

In January 2024, banks' holdings of government securities reached their highest level, exceeding Rs25 trillion, while net OMOs outstanding also remained elevated reaching nearly Rs10tr.

A time-bound relaxation of the Leverage Ratio requirement below 3% for some financial institutions likely facilitated their purchase of additional government bonds with any marginal increase in banks’ holdings of government debt funded via SBP’s short-term liquidity provision.

As a result, the SBP’s total share in outstanding government debt has been stable since 2019, when securities received as collateral from banks are considered.

Successful implementation of the SBP’s 2023-28 Strategy, which prioritizes achieving greater inclusive access to financial services, including through innovative digital solutions, will also help with financial market development.

Addressing the structural impediments to financial sector development, leveling the playing field between conventional and Islamic accounts, and encouraging increased bank deposits, as well as reducing the extent of the informal economy, are also critical.

In the interim, it is critical for the authorities to closely monitor the health of the banking sector.

Prudential measures could also be considered to address the high degree of concentration of assets of certain banks in government bonds and to mandate more robust levels and quality of bank capital to ensure that banks’ capital is adequate to cover those concentration levels and potential stress events.

The SBP should progress with its plans to enhance credit risk management in OMOs, as it currently lacks a well-developed framework to safeguard its balance sheet from potential credit risks.

It does not apply haircuts on bonds taken as collateral, nor does it have sound counterparty eligibility conditions. The range of eligible counterparties has been expanded to include development finance institutions. A

Monetary financing accelerated between 2017 and 2019, and by end-2019, the volume of government debt held by the SBP reached around 20 percent of GDP, constituting close to 40% of domestic debt outstanding.

This fiscal dominance compromised the SBP’s operational independence, jeopardizing the achievement of the inflation target.

In mid-2019, the authorities committed to refrain from any new direct financing of the budget by the SBP and to gradually reduce government debt held in the SBP balance sheet.

In 2022, this policy was institutionalized and became legally binding through amendments to the SBP Act, prohibiting any direct lending to the government and any purchases of government-issued securities in the primary market.

Commercial banks increasingly financed the government even as the government committed to pursuing tight fiscal policies to reduce its borrowing requirement.

Copyright Mettis Link News

Related News

.png?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 167,085.58 225.68M | 0.48% 802.03 |

| ALLSHR | 101,220.72 685.91M | 0.47% 477.65 |

| KSE30 | 50,772.02 134.57M | 0.57% 290.16 |

| KMI30 | 239,923.35 145.03M | 0.77% 1831.31 |

| KMIALLSHR | 66,042.80 345.76M | 0.65% 425.34 |

| BKTi | 45,106.39 29.18M | 0.06% 24.91 |

| OGTi | 33,583.05 26.44M | 1.52% 502.39 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 89,425.00 | 0.00 0.00 | -175.00 -0.20% |

| BRENT CRUDE | 63.86 | 64.09 63.06 | 0.60 0.95% |

| RICHARDS BAY COAL MONTHLY | 91.00 | 0.00 0.00 | 0.10 0.11% |

| ROTTERDAM COAL MONTHLY | 97.25 | 97.25 97.25 | 0.05 0.05% |

| USD RBD PALM OLEIN | 1,016.00 | 1,016.00 1,016.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 60.14 | 0.00 0.00 | 0.06 0.10% |

| SUGAR #11 WORLD | 14.82 | 15.02 14.73 | -0.06 -0.40% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|