Even Rising Interest Rate Could be Good for Equity Investment!

Abu Ahmed | March 29, 2023 at 11:01 AM GMT+05:00

March 29, 2023 (MLN): The coincidence of lower stock prices with higher interest rates is one of the prime postulates in the theory of investing. This article offers a deeper look into the relationships between the two and questions the wisdom of avoiding investing in shares when interest rates are anticipated to increase.

Recession, higher interest rates, and political uncertainty are bad for the stock market. Investors usually shy away from investing in shares whenever they anticipate such changes in economic fundamentals or the political landscape.

It is because the fair value of a stock is the present value of its future earnings; therefore, when a higher interest rate is applied to discount future earnings, it reduces the fair value of a stock, leading to a loss of incentive for investors to bid up the price and value of benchmark indices declines in consequence.

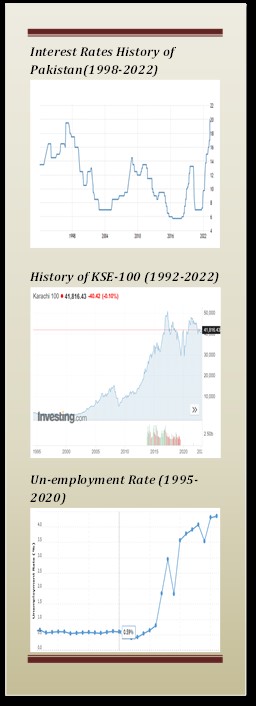

That is why the behavior of KSE-100 mostly happened to be the mirror image of the rise & fall in interest rates. The following table offers a glimpse of the movement of the benchmark index in relation to changes in interest rates from 2008 to 2023:

|

Year |

2008 |

2009 |

2017 |

2019 |

2022 |

2023 |

|---|---|---|---|---|---|---|

|

Interest rate |

8.0% |

14.0% |

6.0% |

13.5% |

6.5% |

20.0% |

|

Delta IR |

------ |

6.0% |

(8%) |

5.5% |

(7.0%) |

13.5% |

|

KSE-100 |

15,000 |

5,000 |

51,000 |

29,000 |

47,000 |

41,000 |

|

Delta KSE |

------ |

(10,000) |

46,000 |

(22,000) |

18,000 |

(6,000) |

What else could be more logical to expect from investors than selling off shares at every opportunity that comes their way or not to bidding up the stock price when happening of any event seems imminent? Both of them push stock prices and the indices downward.

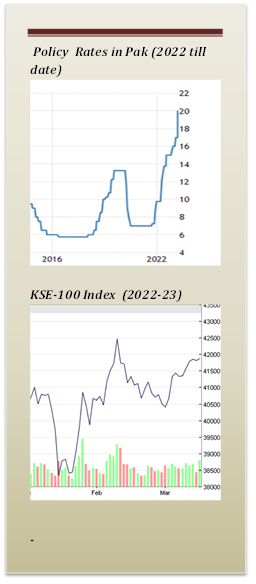

The prevailing interest rates environment in Pakistan is no different than the ones stated above. Political activism and economic uncertainty together drive the interest rates to 20% since the last quarter of 2022, the highest in the country’s history. Further rise in interest rate seems on the card due to un-abated inflation, 31.5% for the month of March 23, weakening PKR against USD, insufficient foreign exchange reserves to pay off forthcomings repayment of foreign debt obligations, and finance imports.

So, investors should stay away from investing in shares?

“Yes” appears as the only option when searching for an answer within the axiom of the inverse relationship between stock prices and interest rates. Then;

Then how run-up in PSX-100 in parallel to the rise in interest rate from the last quarter of 2022 to till date, the period in which the interest rate ascended to 20% from 6.5%, be explained?

The examinations of past data reveal stock price propensity to increase in anticipation of a rise in interest rates for companies or sectors that appear as beneficiaries of interest rate hikes, such as insurance companies and banks. However, such finds have never been used as a pretext to generalize a positive correlation between the two.

Are there incidents of positive correlation between the two elsewhere?

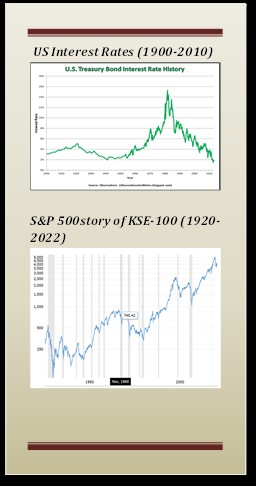

The outcomes of the study of S&P 500 indices relative to changes in 10-year Treasury Bills’ yield within a segmented time frame covering the period from 1946 to 1981 appear as a case in favor of a positive relationship between the two. During this period S&P 500 continually marched upward and peaked at 875 in 1981 from the level of 194 in 1964 in tandem with the rise in interest rate from 2.08% in 1964 to 15.58% in 1981.

Does this mean that the behavior of the S&P 500 between 1964 to 1981 and of PSX-100 since the last quarter of 2022 to till date may be taken as a paradigm to explain an otherwise relationship between interest rates and benchmark indices?

Before affirming such a relationship, it is to note that the year 1946 was the year when the US economy started coming out of the great depression. Increasing economic activities have created a demand for capital. The crowding out effect for capital had pushed the interest rate up to 15.58% in 1981 from 2.08% p.a. in 1946.

Investing psychology has an explanation for the positive relationship between the two as well. According to the theory, once investors are out of the initial shocks of the rise in interest rates and realize that it is going to stay for a foreseeable future, they start buying stocks that offer an additional return to compensate for the extra risk that emerges with the rise in interest rates.

The spill-over effect of bidding up stock at higher prices is the rise in benchmark indices despite higher interest rates.

These two examples simplify the answer. When efforts are obvious to put the economy on the path, or signs of economic recovery are everywhere, future earnings of the companies are expected to grow. This encourages investors to bid up stock prices which resulted in the rise in benchmark indices despite the rise in interest rates.

Similarly, when investors realized that high-interest rates are going to stay for the foreseeable future, survival instinct within investors initially motivates them to go bargain hunting of shares for extra return, which gradually transforms into a general behavior.

Gains in the PSX-100 index due to the psychological adjustment of investors to higher interest rates may be presumed as a progressive move to test the new peak when supported by favorable changes in economic fundamentals, otherwise, simply a ripple.

According to Mr. Morgan Housel, the writer of the book “The Psychology of Money”, outcomes of investment depend on luck. He wrote in his book that when I asked economist Robert Shiller;

“What do you want to know about investing that we can’t know?”

And the reply came as:

“The exact role of luck in successful outcomes.”

It is good to have luck on the side, but it will still be prudent to take into consideration the structural difference between the economies and politics of the two countries before drawing a paradigm for PSX-100 behavior in rising interest rate in parallel to how the S&P 500 behaved in rising interest rates in between 1945 to 1981, as they stand apart in term of market capitalization, level of financial literacy, depth of trading volume, degree of price volatility and capacity of the economy to recover from economic shocks.

*The writer is a business graduate in Finance and MIS from IBA, Karachi with an MSc in Statistics from the University of Karachi and a fellowship in Life Insurance from LOMA, USA, and a certified trainer by the US-AID Programme. He has been associated with business schools as a visiting faculty teaching courses on investment, finance, and financial risk management.

He is currently engaged in investment research and policy with one of the leading life insurance companies in Pakistan.

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|