Effective fiscal management propels Pakistan's economic resurgence

By MG News | December 07, 2023 at 03:25 PM GMT+05:00

December 07, 2023 (MLN): Pakistan’s economy is on a gradual but promising path to recovery as effective fiscal management through robust growth in revenues and a cautious expenditure approach will navigate potential challenges and maintain positive momentum in the fiscal sector.

The government has released the economic update and outlook report for November 2023, revealing that the ongoing economic revival initiatives are fueling a notable surge in economic activity.

On the fiscal front, healthy growth in revenues outpaced the growth in expenditure during the first quarter of FY2024.

Both tax and non-tax collection attributed to a significant rise in total revenues, however, a substantial increase in non-tax collection on the back of higher receipts from petroleum levy remained the major source of the increase.

Thus, with healthy growth in revenues relative to expenditures, the fiscal deficit reduced to 0.9% of GDP in Jul-Sep FY2024 from 1% of GDP last year.

Primary balances continued to be in surplus and improved to Rs416.8 billion (0.4% of GDP) in 1QFY24 from Rs134.7bn (0.2% of GDP) last year.

The fiscal performance in 1QFY24 reflects a positive trajectory, characterized by a notable surge in total revenues relative to expenditures.

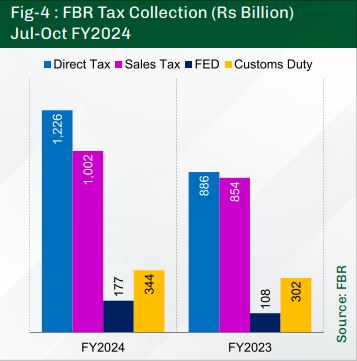

Similarly, the pace of growth in FBR tax collection remained robust sustained by various tax policy and administrative initiatives.

Encouragingly, this marks the 4th consecutive month in which FBR achieved the revenue collection target.

Performance of the KSE-Index

Positive economic signals and recovery indicators have triggered the market sentiment.

The benchmark of PSX, the KSE-100 index gained 5,724 points while the market capitalization of PSX increased by Rs666bn and settled at Rs7,552bn as of October 31, 2023.

During the period under review (Sep-Oct, 2023), the KSE-100 index posted a significant growth of 14.7%, while the S&P 500 of US declined by 7.1%, CAC 40 of France by 5.6%, SSE Composite of China by 3.7% and Sensex 30 of India by 2.3%.

The sustained monetary policy stance and successful IMF staff review in November drove the market confidence.

Owing to reforms in exchange companies and a reduction in -illicit transactions, the exchange rate remained stable thus exerting a positive impact on overall economic activity.

Real Sector

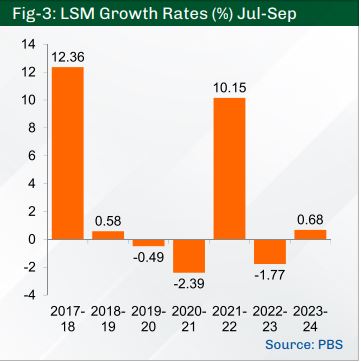

The Large-Scale Manufacturing (LSM) sector demonstrated a positive trend for the second consecutive month while posting a growth of 1% in September 2023.

After several months of decline, the industry has been on the path of recovery since August 2023.

The stability in the exchange rate, ease in supply disruptions due to the removal of import restrictions, and improved dollar liquidity contributed to this economic upswing.

The agriculture sector also enjoyed the effects of economic recovery. The farm tractor production and sales witnessed growth of 55.1% (17,098) and 86.8% (17,296), respectively during Jul-Oct FY2024 over the corresponding period last year.

During October 2023 the 6.8% growth in urea and 2.22x in DAP offtake compared to October 2022, indicated a positive growth in Rabi crops.

Inflation

With respect to consumer prices, the headline inflation sustained at 26.9% on a YoY basis in October 2023 as compared to 26.6% in October 2022.

The major drivers include Food and nonalcoholic beverages, Housing, water, electricity, gas & fuel, Transport, and Furnishing & household equipment maintenance.

However, keeping in view the crop cycle of perishables, the supply pressures are expected to be relieved from the end of November and onwards.

Moreover, the reduction of fuel prices by the government would help further easing out inflationary pressures.

External Sector

On the external front, in Jul-Oct FY2024, the Current Account marked a deficit of $1.05 billion as against a deficit of $ 3.1bn last year, largely reflecting an improvement in the trade balance.

The country’s earnings through exports increased by 21.1% to $2.8bn in October 2023 as compared to $ 2.3bn in September 2023, owing to ease in import restrictions resulting in a smooth supply of raw material for export-oriented industries.

Foreign Investment

The Foreign Direct Investment (FDI) in the country reached $524.7m during Jul-Oct FY24, compared to $489.9m direct investment reported in the SPLY, reflecting an increase of 7.1% mainly on account of Chinese investment.

Foreign Private Portfolio Investment has registered a net inflow of $10.9m. Foreign Public Portfolio Investment recorded a net inflow of $ 3.2m. The total FPI recorded an inflow of $14.1m as against an outflow of $32.6m last year.

Worker's Remittances

The inflow through remittances also increased by 11.5% MoM in October 2023 to $2.5bn as compared to $2.2bn in September 2023.

On a yearly basis, it grew by 9.1% because of structural reforms related to the FX market and the convergence of exchange rates in interbank and open markets.

In Jul-Oct FY2024, workers' remittances decreased by 13.3% YoY to $8.8bn, compared to $10.1bn in SPLY.

Monetary Sector

On the policy front, the monetary policy rate was maintained at 22%, owing to the significant performance of high-frequency indicators and improved inflation outlook.

The decision was based on observed significant improvement in high-frequency indicators including crop performance, revival in the LSM sector and aligned indicators, fiscal consolidation, and external sector stability.

Overall, positive economic signals and recovery indicators steering the improvement in the GDP outlook for the fiscal year.

Foreign Exchange Reserves

Pakistan's total liquid foreign exchange reserves increased to $12.4bn on November 23, 2023, with SBP's reserves standing at $7.3bn and Commercial banks' reserves remaining at $5.1bn.

Developments with IMF

International Monetary Fund (IMF) staff and the Pakistani authorities reached a staff-level agreement on the first review under Pakistan's Stand-By Arrangement (SBA) on November 15, 2023.

Upon approval, Pakistan will have access to $700m. The SBA supports the government's commitment to advance the planned fiscal consolidation, accelerate cost-reducing reforms in the energy sector, complete the return to a market-determined exchange rate, pursue SOEs and governance reforms to attract investment and support job creation while continuing to strengthen social assistance.

The government's execution of the FY24 budget with continued adjustment of energy prices, and renewed flows into the foreign exchange (FX) market have lessened fiscal and external pressures.

Furthermore, the inflationary pressures are receding and the outlook has improved Inflation is expected to decline over the coming months amid receding supply constraints and modest demand.

With all these positive developments, further improvement in domestic economic activities is anticipated in upcoming months.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 131,949.07 198.95M |

0.97% 1262.41 |

| ALLSHR | 82,069.26 730.83M |

0.94% 764.01 |

| KSE30 | 40,387.76 80.88M |

1.11% 442.31 |

| KMI30 | 191,376.82 77.76M |

0.36% 678.77 |

| KMIALLSHR | 55,193.97 350.11M |

0.22% 119.82 |

| BKTi | 35,828.25 28.42M |

3.64% 1259.85 |

| OGTi | 28,446.34 6.84M |

-1.02% -293.01 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 108,125.00 | 110,525.00 107,865.00 |

-2290.00 -2.07% |

| BRENT CRUDE | 68.51 | 68.89 67.75 |

-0.29 -0.42% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

0.75 0.78% |

| ROTTERDAM COAL MONTHLY | 106.00 | 106.00 105.85 |

-2.20 -2.03% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.50 | 67.18 66.04 |

-0.50 -0.75% |

| SUGAR #11 WORLD | 16.37 | 16.40 15.44 |

0.79 5.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|