Effect of US election outcome on sovereign credit profiles will vary, Fitch says

MG News | November 11, 2024 at 10:40 AM GMT+05:00

November 11, 2024 (MLN): The re-election of Donald Trump as US president, supported by likely Republican majorities in both houses of Congress, will have ramifications for many sovereign credit profiles, but the scale of any effects on ratings will ultimately depend on the policies pursued by his administration, says Fitch Ratings.

The ratings agency believes the key channels of influence for sovereigns are likely to be through US policies affecting trade, immigration, fiscal performance, financial markets (including borrowing costs), and geopolitical risk.

The policy responses of affected sovereigns and their rating headroom will also be relevant for the overall effect on their credit profiles.

It believes that the US will raise tariffs under a Trump administration, with China likely to be a particular target. However, the impact of higher tariffs on countries that export to the US will vary significantly - depending on the size of any tariff increases, their timing and whether they are targeted or broad-based.

Fitch has conducted a scenario analysis around the potential effect of US tariff hikes on the GDP of its trade partners.

This illustrates that Mexico, Canada, China, Vietnam and Korea are among the most exposed to aggressive increases, though the hit to GDP is significant for many more economies - including developed markets in Europe - in scenarios where US tariff hikes prompt wider tariff escalation.

Weaker growth prospects or external finances because of increased protectionism would weigh on the credit metrics of affected sovereigns.

Tighter immigration policies also appear likely, though they could face implementation challenges, Fitch Ratings said.

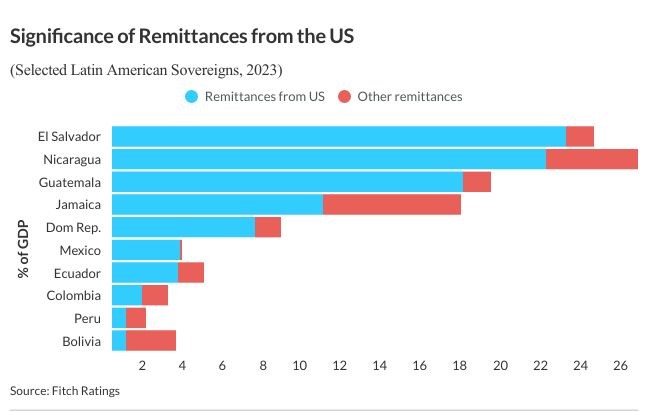

This could lead to lower remittance inflows for many emerging markets (EMs).

The US is the dominant source of remittances for most Latin American EMs, notably those where remittances are large relative to GDP, including El Salvador, Nicaragua, Guatemala, Jamaica, and the Dominican Republic, as well as Mexico.

It is also an important source for some non-Latin American EMs with large remittance exposure, such as the Philippines.

Fitch believes that if US fiscal policy is loosened - particularly in the context of tariff increases and tighter immigration controls - this could lead to higher US bond yields, which could in turn lead to US dollar appreciation.

Yields on the 10-year treasury yield have risen almost 80bp since September, despite a 50bp cut to the Fed Funds rate that same month (the Fed cut by a further 25bp on November 07).

However, the medium-term path of US interest rates would depend on multiple factors, including the Federal Reserve’s assessment of labour market and inflation prospects.

Higher US bond yields and/or a stronger US dollar would increase US dollar borrowing costs and associated debt-repayment burdens for sovereigns with US dollar-denominated debt. Refinancing US dollar debt could also become more challenging.

"We have previously stated that sustained periods of US dollar strength against EM currencies can weigh on some EM sovereign credit profiles - particularly weaker EMs with a large share of their debt denominated in foreign currency or those that manage their currencies tightly against the US dollar."

The next US administration may call for greater contributions from its allies to global security. "We think several NATO partners in Europe as well as Korea and Taiwan in Asia could face pressure from the US to raise defence spending," the ratings agency added.

This, in turn, would further complicate their efforts to advance fiscal consolidation. "We expect US foreign policy to become more transactional and unpredictable, increasing geopolitical risks," it said.

There are also likely to be some significant changes in US climate policy under a Trump administration, with reduced prospects for greenhouse gas reduction.

Fitch believes climate change exposes many sovereigns to physical risks that could affect credit profiles over the medium-term.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,758.68 230.33M | 2.33% 3914.43 |

| ALLSHR | 103,210.42 446.53M | 2.00% 2019.96 |

| KSE30 | 51,538.68 121.33M | 2.45% 1230.67 |

| KMI30 | 246,655.10 99.60M | 2.33% 5613.93 |

| KMIALLSHR | 67,042.93 242.70M | 1.94% 1274.01 |

| BKTi | 47,335.06 38.60M | 3.11% 1429.89 |

| OGTi | 36,333.34 9.28M | 2.18% 775.42 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 77,635.00 | 77,720.00 76,105.00 | 1860.00 2.45% |

| BRENT CRUDE | 97.72 | 100.73 97.10 | -5.82 -5.62% |

| RICHARDS BAY COAL MONTHLY | 110.00 | 0.00 0.00 | -8.75 -7.37% |

| ROTTERDAM COAL MONTHLY | 113.00 | 0.00 0.00 | 0.30 0.27% |

| USD RBD PALM OLEIN | 1,191.50 | 1,191.50 1,191.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 91.08 | 93.90 90.32 | -5.52 -5.71% |

| SUGAR #11 WORLD | 14.68 | 14.91 14.59 | -0.22 -1.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|