Economies to face inflationary pressure in 2023: WEF

MG News | January 12, 2023 at 10:07 AM GMT+05:00

January 12, 2023 (MLN): The year 2023 has begin with eerily familiar risks of inflationary pressures, cost of living crises, trade wars, capital outflows from emerging market, widespread social unrest, geopolitical confrontation, and the spectre of nuclear warfare which few of this generation’s business leaders and public policy-makers have experienced.

According to a recent insight report by World Economic Forum on 'The Global Risks Report 2023' stated, "Governments and central banks could face stubborn inflationary pressures over the next two years."

"The global forum said that Pakistan was also among larger emerging markets exhibiting a heightened risk of default. Other countries include Argentina, Egypt, Ghana, Kenya, Tunisia, and Türkiye", the report highlighted.

These global problems are amplified by new developments in the global risks landscape, including unsustainable levels of debt, a new era of low growth, low global investment and de-globalization.

In addition, a decline in human development after decades of progress, rapid and unconstrained development of dual-use (civilian and military) technologies, and the growing pressure of climate change impacts and ambitions in an ever-shrinking window for transition to a 1.5°C world which led economies in recession.

“Together, these are converging to shape a unique, uncertain and turbulent decade to come”, the report highlighted.

This report has presented the results of the latest Global Risks Perception Survey (GRPS), which is consisted of three frames for understanding global risks.

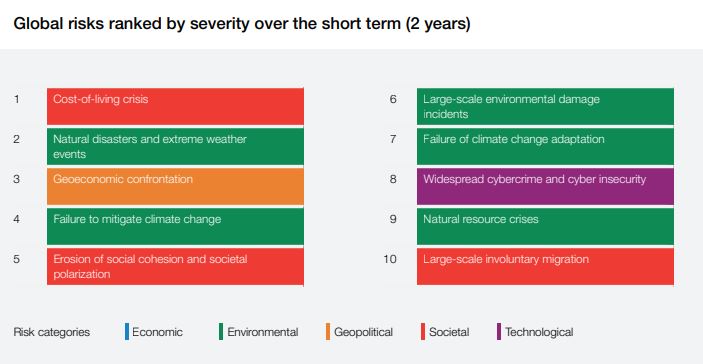

According to survey, most respondents to the 2022-2023 GRPS chose energy supply crisis, cost-of-living crisis, rising inflation, food supply crisis, and cyberattacks on critical infrastructure as among the top risks for 2023 with the greatest potential impact on a global scale.

Those that are outside the top five for the year but remain concerns include: failure to meet net zero targets, weaponization of economic policy, weakening of human rights, a debt crisis, and failure of non-food supply chains.

The complex and rapid evolution of the global risks landscape is adding to a sense of unease. More than four in five GRPS respondents anticipated consistent volatility over the next two years at a minimum, with multiple shocks accentuating divergent trajectories, it noted.

Respondents to the GRPS see the path to 2025 dominated by social and environmental risks, driven by underlying geopolitical and economic trends.

There were some notable differences between the responses of government and business respondents, with debt crises, failure to stabilize price trajectories, failure to mitigate climate change, and failure of climate change adaptation featuring more prominently for governments, and widespread cybercrime and cyber insecurity, and large-scale environmental damage incidents featuring higher for business.

The following sections explore the most severe global risks that many expect to play out over the next two years, within the context of the mounting impacts and constraints being imposed by the numerous crises felt today.

Cost of Living Crisis

Ranked as the most severe global risk over the next two years by GRPS respondents, a global Cost-of living crisis is already here, with inflationary pressures disproportionately hitting those that can least afford it.

Cost-of-living crisis was broadly perceived by GRPS respondents to be a short-term risk, at peak severity within the next two years and easing off thereafter.

But the persistence of a global cost-of living crisis could result in a growing proportion of the most vulnerable parts of society being priced out of access to basic needs, fueling unrest and political instability.

Continued supply-chain disruptions could lead to sticky core inflation, particularly in food and energy. This could fuel further interest rate hikes, raising the risk of debt distress, a prolonged economic downturn and a vicious cycle for fiscal planning.

Economic downturn

Last year’s edition of the Global Risks Report warned that inflation, debt and interest rate rises were emerging risks.

Today, governments and central banks led by developed markets, notably the United States of America, Eurozone and the United Kingdom of Great Britain are walking a tightrope between managing inflation without triggering a deep or prolonged recession, and protecting citizens from a cost-of-living crisis while servicing historically high debt loads.

Public-sector respondents to the GRPS ranked debt crises, failure to stabilize price trajectories, and prolonged economic downturn in the top 10 risks over the next two years.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 138,597.36 256.32M | -0.05% -68.14 |

| ALLSHR | 85,286.16 608.38M | -0.48% -413.35 |

| KSE30 | 42,340.81 77.13M | -0.03% -12.33 |

| KMI30 | 193,554.51 76.19M | -0.83% -1627.52 |

| KMIALLSHR | 55,946.05 305.11M | -0.79% -443.10 |

| BKTi | 38,197.97 16.53M | -0.59% -225.01 |

| OGTi | 27,457.35 6.73M | -0.94% -260.91 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 117,670.00 | 121,165.00 117,035.00 | -1620.00 -1.36% |

| BRENT CRUDE | 69.23 | 70.77 69.14 | -0.29 -0.42% |

| RICHARDS BAY COAL MONTHLY | 96.50 | 0.00 0.00 | 2.20 2.33% |

| ROTTERDAM COAL MONTHLY | 104.50 | 104.50 104.50 | -0.30 -0.29% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 66.03 | 67.54 65.93 | -0.20 -0.30% |

| SUGAR #11 WORLD | 16.79 | 17.02 16.71 | 0.05 0.30% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|