Current Account Surplus: A Hollow Success

Muhammad Ghazanfar Sakrani | May 08, 2023 at 11:21 AM GMT+05:00

May 08, 2023 (MLN): The current account balance, being an important indicator of an economy’s state, has remained a pain in the neck for policymakers. Both PML-N and PTI governments were lambasted consequent to a whopping deficit of $19.89 billion and $17.4 billion in fiscal year 2018 and 2022 respectively.

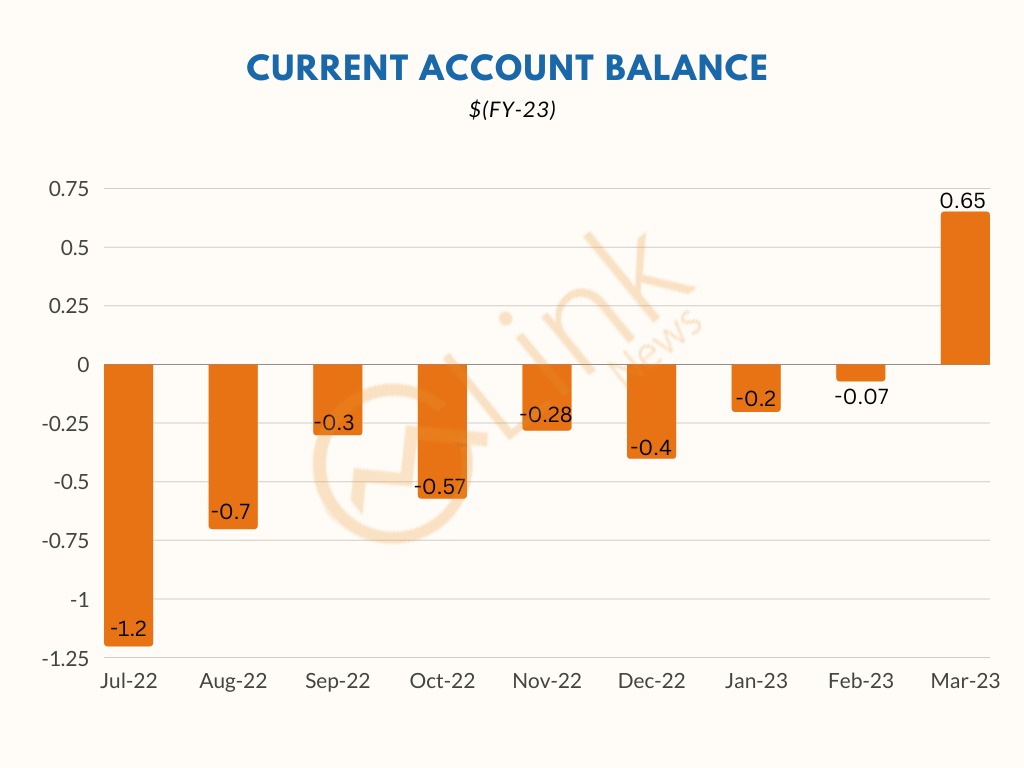

The fiscal year 2023 has seen a curtailment in the deficit which remained on a downward trajectory and is recorded at $3.4 billion for July-March FY23, compared to a $13 billion deficit in the same period last year.

A discernable development is the recording of a current account surplus in the month of March 2023 for the first time since November 2020. After lowering to a meager $0.07 billion deficit in February 2023, the current account finally turned green after a hiatus with a balance of $0.65 billion in March.

The tweet of the PML-N finance czar celebrating this news may make one believe that the economic indicators are ameliorating. So, the question arises, ‘Does the surplus depict a silver lining or the improvement is illusory?’. The answer may be the latter! There is more than meets the eye. The surplus was well anticipated by the analysts and the deficit in the proceeding months of the ongoing fiscal year remains out of sight.

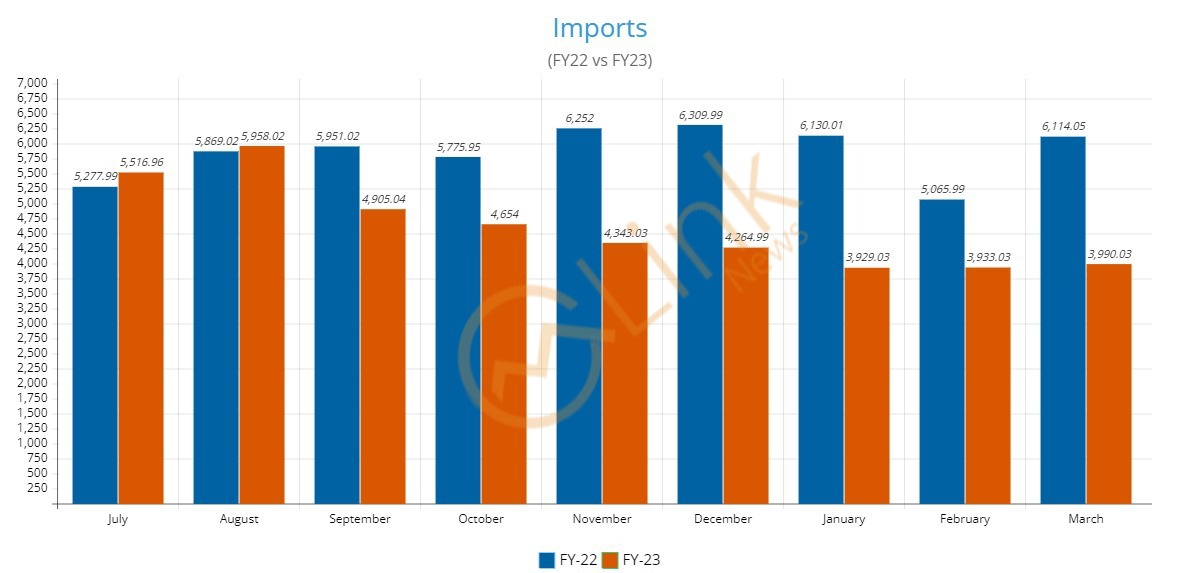

This owes to a hawkish policy stance and stringent import curb measures introduced by the incumbents to keep the reserves in check, which remain at a nadir of $4 billion, just enough to cover one month of import bills. Had the balance improved amid a surge in exports would have been a rosy scenario, however, exports diminished by 20% year-on-year in March.

Remittances posted healthy growth on a monthly basis clocking in at $2.53 billion amid the Ramadan factor. These are expected to remain elevated above $2 billion for the month of April too which may prove conducive for a surplus.

The surplus may provide respite to the cash-strapped economy albeit its sustainability remains a question mark. The slump in imports is temporary, a removal of administrative control allowing banks to clear LCs without any hesitance may fuel up the deficit.

The imports may fall short of the target of $65.6 billion touching just $55 billion for FY23. On one hand, import curb provides a means of window dressing by posting a current account surplus. On the contrary, these curbs take a heavy toll on the economy.

The industries dependent on raw material imports are breathing for survival. Many businesses are scaling back their operations or have announced multiple and continuous production halts, especially in the automobile sector.

Unemployment is expected to touch 10% for the first time ever which is the ramification of the policies reminiscent of throwing the baby out of the bathwater.

The growth outlook is also grim as depicted by the World Bank and Asian Development Bank's revised growth forecast south of 1%.

The informal economy is expanding at the hands of import curbs where import payments are flourishing through hawala/hundi.

The port has turned into a city of containers. Industrialists are fretting and businesses are facing double-whammy setbacks owing to import restrictions and high costs of doing business.

The export figures too remain dismal, contracting by 11.7% during the July-April period and reaching just 61% of the annual export target set at $38 billion. The final figures are expected to remain lower than the previous year and record at $28 billion, missing the target by a huge figure. Unless the export base is increased, any artificial surplus resulting from the import curb may not entice.

With reserves at a nadir of $4 billion and limbo in the revival of the IMF program, the reliance on import curbs may prove to be counterproductive. They may help the country maintain the reserves but may result in social unrest and business closures, posing a far more serious economic challenge from which there will be no escape.

THE CLOCK IS TICKING!

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|