Weekly Market Roundup

MG News | May 23, 2026 at 10:25 AM GMT+05:00

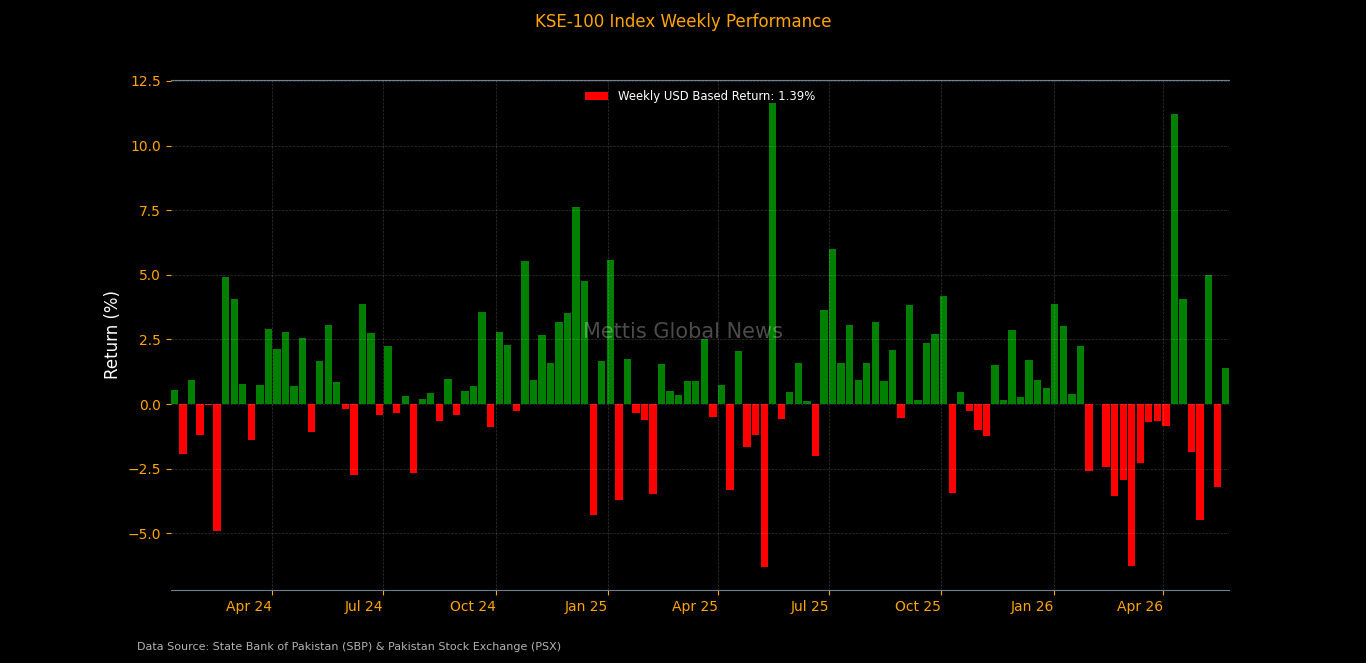

May 22, 2026 (MLN): Pakistan's equity market staged a recovery during the week ended May 22, 2026, with the benchmark KSE-100 Index closing at 167,844.25, compared to 165,596.07 recorded on May 15, 2026.

The index gained 2,248.18 points, translating into a 1.36%

week-on-week (WoW) gain, as positive global cues, declining oil prices, and

improved investor sentiment fueled broad-based buying activity across the

market.

Market Capitalization

Total market capitalization recovered in line with the

benchmark index performance. As of May 22, 2026, market capitalization stood at

Rs4.801 trillion, compared to Rs4.737tr on May 15, 2026, marking an increase of

Rs64.27bn or 1.36% WoW.

In USD terms, market capitalization rose to $17.24bn from

$17.00bn in the previous week, showing a gradual recovery in overall market

value on the back of broad-based buying interest._20260523052015924_372507.jpeg)

Dollar-adjusted returns also turned positive, clocking in at

1.39% WoW, compared to negative 3.19% in the prior week, indicating improving

investor returns in both local and foreign currency terms.

On the macroeconomic front, Pakistan’s banking spread widened

to 690bps in April 2026 as lending rates outpaced deposit returns, while

real deposit rates remained negative amid persistent inflation.

Despite a slight increase in deposit rates to 4.85%, savers

continued to face erosion in purchasing power as inflation kept real returns

below zero.

Pakistan’s

automobile financing climbed to Rs359.58bn in April 2026, marking a 36.6%

YoY surge despite high borrowing costs and persistent pressure on consumer auto

demand.

Pakistan’s

net foreign direct investment plunged to $54.5 million in April 2026,

sharply down from $178.8 million a year earlier amid rising foreign outflows

and weaker investor inflows.

Pakistan’s

REER climbed to 105.8 in April 2026, showing a decline in trade

competitiveness as the rupee strengthened in real terms against major trading

partner currencies.

Pakistan’s

current account posted a deficit of $324m in April 2026 as a sharp surge in

imports widened the trade gap despite strong remittance inflows.

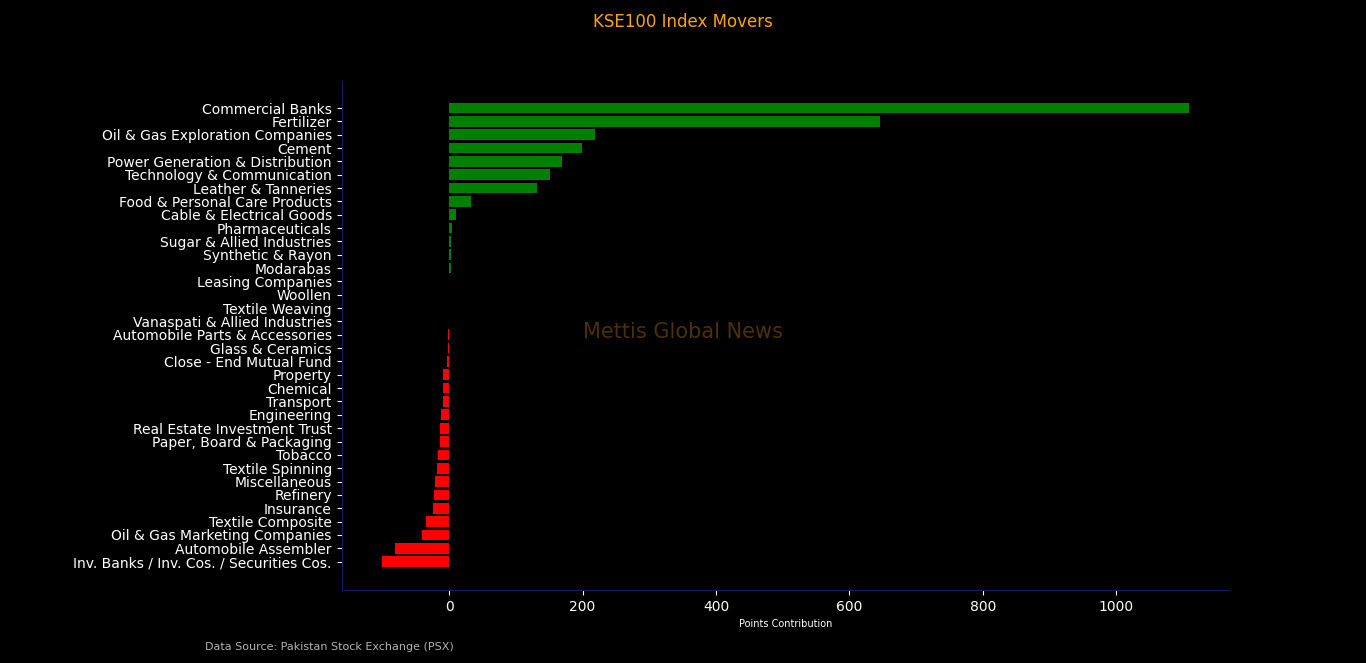

Index Movers

Sector-wise, the recovery was broad-based and led by

index-heavy sectors.

Commercial banks emerged as the largest positive contributor

to the benchmark index, adding 1,109.13 points amid strong buying in major

banking names. Fertilizer stocks contributed 646.30 points to the index, while

oil & gas exploration companies added 219.17 points during the week.

Cement stocks contributed 198.78 points, followed by power

generation & distribution (+168.88 points), technology & communication

(+151.48 points), leather & tanneries (+132.36 points), food & personal

care products (+32.06 points), cable & electrical goods (+10.66 points),

pharmaceuticals (+4.02 points),

Sugar & allied industries (+3.33 points), synthetic

& rayon (+2.43 points), and modarabas (+2.31 points), reflecting the

broad-based nature of the market recovery.

On the negative side, investment banks/investment

companies/securities companies remained the largest drag on the benchmark

index, erasing 100.87 points, followed by automobile assemblers (-81.00

points), oil & gas marketing companies (-41.44 points), textile composite

(-34.93 points), and insurance (-23.78 points).

Additional negative contributions came from refinery (-22.52

points), miscellaneous (-20.84 points), textile spinning (-18.84 points),

tobacco (-16.61 points), paper, board & packaging (-13.43 points), real

estate investment trust (-13.23 points), engineering (-11.55 points), transport

(-9.55 points), chemical (-9.04 points),

Property (-8.85 points), close-end mutual fund (-3.06

points), glass & ceramics (-1.43 points), automobile parts &

accessories (-1.11 points), vanaspati & allied industries (-0.45 points),

textile weaving (-0.09 points), woollen (-0.06 points), and leasing companies

(-0.05 points), indicating pockets of persistent weakness.

Scrip-wise, the upside was dominated by heavyweight banking,

fertilizer, and energy stocks.

United Bank Limited emerged as the largest positive

contributor, lifting the index by 752.20 points, followed by Fauji Fertilizer

Company (+528.44 points), HUBCO (+190.45 points), Pakistan Petroleum Limited

(+184.65 points), and Bank AL Habib (+145.99 points).

Other major gainers included Pakistan Telecommunication

Company (+140.41 points), Service Industries (+132.36 points), Engro

Fertilizers (+104.82 points), National Bank of Pakistan (+103.23 points), MCB

Bank (+88.88 points), Lucky Cement (+67.29 points), Standard Chartered Bank

Pakistan (+46.35 points),

Oil & Gas Development Company (+39.69 points),

Colgate-Palmolive Pakistan (+35.46 points), DG Khan Cement (+35.30 points), and

Sui Northern Gas (+34.59 points), showing renewed confidence in blue-chip

names.

Additional positive contributions came from AGP Limited,

Habib Bank Limited, Fauji Cement, POWER Cement, Pioneer Cement, Fatima

Fertilizer, Cherat Cement, Kohat Cement, Askari Bank, Systems Limited, Pak

Elektron, TGL, Kohat Textile, Indus Motor, Air Link Communication,

Maple Leaf Cement, Haleon Pakistan, Mari Petroleum, and

Rafhan Maize Products, reflecting broad-based buying across banking,

fertilizer, cement, technology, and energy sectors.

On the downside, losses remained concentrated in investment

companies, automobile assemblers, and oil marketing stocks.

Engro Holdings emerged as the largest negative contributor,

dragging the index by 103.05 points, followed by Pakistan State Oil (-64.00

points), Millat Tractors (-56.84 points), Sazgar Engineering Works (-40.20

points), and Bank Alfalah (-29.77 points).

Other notable laggards included Habib Metropolitan Bank

(-23.90 points), Adamjee Insurance (-23.78 points), GlaxoSmithKline Pakistan

(-23.53 points), Mehmood Textile (-21.98 points), Cnergyico PK (-20.64 points),

Gadoon Textile (-18.84 points), Pakistan Tobacco (-16.61 points),

PSEL (-17.67 points), NML (-15.60 points), Packages Limited

(-13.43 points), LCI (-12.88 points), Bank of Punjab (-11.59 points), KEL

(-11.58 points), GHGL (-11.25 points), BWCL (-10.98 points), NPL (-10.47

points),

TRG Pakistan (-9.42 points), and Treet Corporation (-9.55

points), highlighting residual pressure in oil marketing, automobile,

insurance, and pharmaceutical segments._20260523051947646_d564f8.jpeg)

FIPI/LIPI

Foreign investors turned net sellers during the week, with

total net foreign selling in the equity segment standing at Rs3.94bn ($14.15m).

Within foreign flows, foreign corporates recorded heavy net

selling of Rs4.09bn ($14.69m), only partially offset by net buying from

overseas Pakistanis amounting to Rs145.16m ($520,549). Foreign individuals

remained marginal net buyers at Rs6.08m ($21,856).

On the local side, insurance companies emerged as the

largest net buyers with inflows of Rs3.73bn, followed by individuals at

Rs1.03bn, banks/DFIs at Rs855.01m, and NBFCs at Rs72.73m.

Meanwhile, broker proprietary trading remained the largest

net seller, offloading equities worth Rs836.98m, followed by companies with net

selling of Rs716.99m.

Other organizations and mutual funds also remained net

sellers, offloading Rs117.57m and Rs76.51m respectively during the week._20260523051953159_20f7b0.jpeg)

Copyright Mettis Link News

Related News

_20260430120221816_68194f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 175,734.95 112.79M | 2.76% 4713.75 |

| ALLSHR | 106,503.33 301.75M | 2.57% 2666.95 |

| KSE30 | 52,480.44 49.24M | 3.00% 1528.45 |

| KMI30 | 247,935.35 44.71M | 3.03% 7301.48 |

| KMIALLSHR | 68,316.39 142.88M | 2.62% 1743.64 |

| BKTi | 50,028.65 14.91M | 2.78% 1355.42 |

| OGTi | 34,819.37 3.89M | 3.31% 1117.12 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,420.00 | 65,570.00 63,875.00 | 1205.00 1.88% |

| BRENT CRUDE | 92.05 | 93.60 89.58 | -4.73 -4.89% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 0.00 0.00 | 0.85 0.71% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 84.70 | 86.20 83.10 | -4.61 -5.16% |

| SUGAR #11 WORLD | 14.76 | 0.00 0.00 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|