Weekly Market Roundup

MG News | March 07, 2026 at 12:28 PM GMT+05:00

March 07, 2026 (MLN): Pakistan’s equity market

remained under heavy selling pressure during the outgoing week, as the

benchmark KSE-100 Index closed at 157,496.10, compared to 168,062.17

recorded on February 27, 2026.

The index lost 10,566.07 points over the week,

translating into a decline of 6.29% week-on-week (WoW), as aggressive

selling in banking, cement, fertilizer, and technology stocks dragged the

benchmark sharply lower.

Investor sentiment remained weak during the week amid rising

global uncertainty and geopolitical tensions in the Middle East.

The uncertain external environment prompted investors to

adopt a cautious stance, leading to profit-taking across major sectors and

adding to the overall selling pressure in the market._20260307072354173_1a698a.jpeg)

Market Capitalization

Market capitalization mirrored the sharp decline in the

benchmark index. The total listed market cap dropped to Rs4.62 trillion on

March 6, 2026, compared to Rs4.96tr recorded on February 27, 2026,

marked a contraction of approximately Rs333.75bn or 6.73% WoW.

In dollar terms, total market capitalization declined

by $1.19bn during the week, compared to a decline of $538.64m in the

previous week, highlighting the intensity of equity market losses._20260307070943715_07a0c0.jpeg)

Meanwhile, dollar-adjusted returns stood at negative

6.26%, compared to negative 2.92% in the prior week, indicating that

the bulk of the decline was driven by falling equity prices rather than

currency movements._20260307070936522_05d249.jpeg)

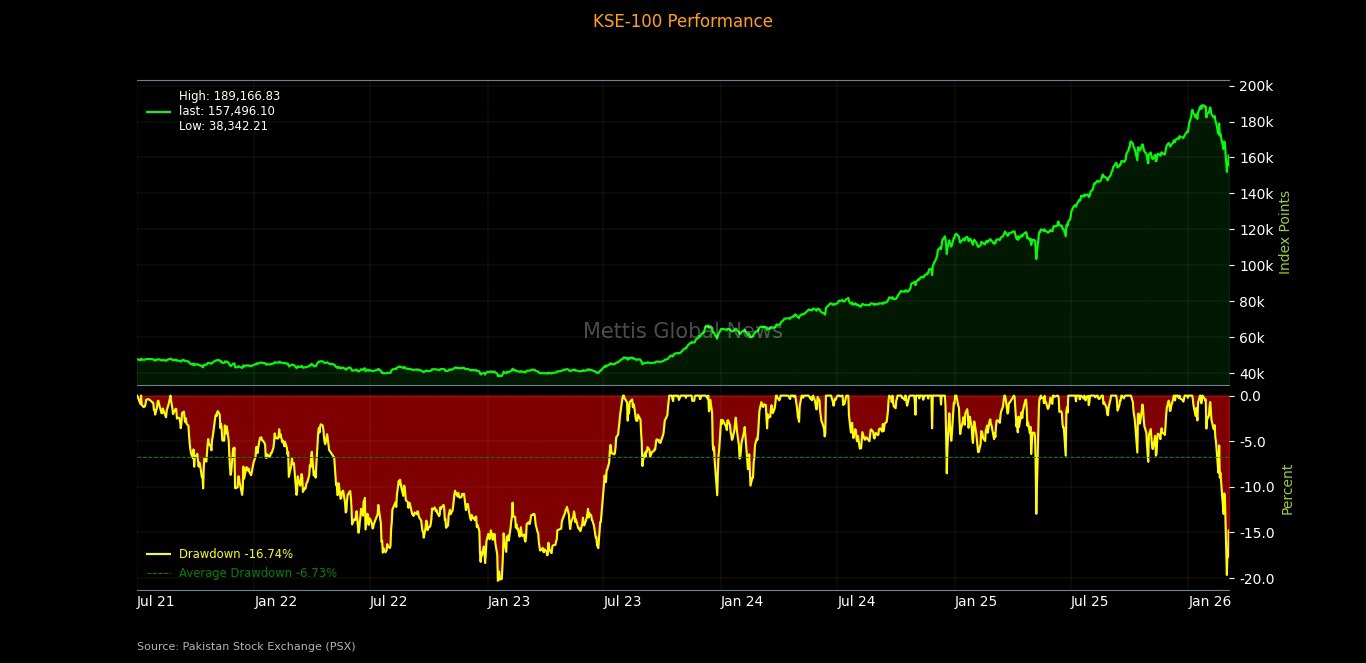

Periodic Drawdowns

The long-term performance of the KSE-100 Index reflects a

powerful multi-year bull cycle, characterized by strong upward momentum

interspersed with periodic corrections.

From mid-2023 onward, the index entered a steep upward

trajectory, supported by improving macroeconomic stability, easing external

account pressures, and robust domestic liquidity.

This rally eventually pushed the benchmark to an all-time

high near 189,167 points.

However, the latest reading of around 157,496 points

indicates a drawdown of approximately 16.7% from the peak, marking one

of the sharper corrections within the recent bull cycle.

While the decline appears significant in the short term, the

chart shows that the average drawdown historically hovers around the

mid-single-digit range (roughly 6–7%), suggesting that such pullbacks are

not unusual during extended market uptrends.

Historically, the Pakistan Stock Exchange has witnessed even

deeper and more prolonged corrections, particularly during episodes of

political uncertainty, currency volatility, or tightening financial conditions.

The current pullback therefore represents a meaningful

but still cyclical correction within a broader long-term uptrend,

highlighting the market’s tendency to experience sharp interim declines even

during sustained bullish phases.

On the macroeconomic front, National Savings Schemes (NSS)

mobilization rebounded 545%

MoM to Rs27.01bn in January, recovering from December’s sharp slowdown

but remaining 28.8% lower YoY for FY2025-26.

Pakistan’s central government debt rose 9.98%

YoY to Rs79.32tr in January 2026, driven by higher domestic and

external borrowing to finance the fiscal deficit.

SBP raised Rs581.7bn

through MTBs in the latest auction, while rejecting all bids for

10-year floating-rate PIBs, as cut-off yields jumped up to 39bps across

tenors, signaling rising rate expectations.

Pakistan’s

trade deficit widened 8.4% MoM to $2.98bn in February 2026 as

exports plunged 25.6%, outweighing the decline in imports.

Pakistan’s

CPI inflation rose to 7% YoY in February 2026, the highest

since October 2024, as price pressures picked up from 5.8% in January.

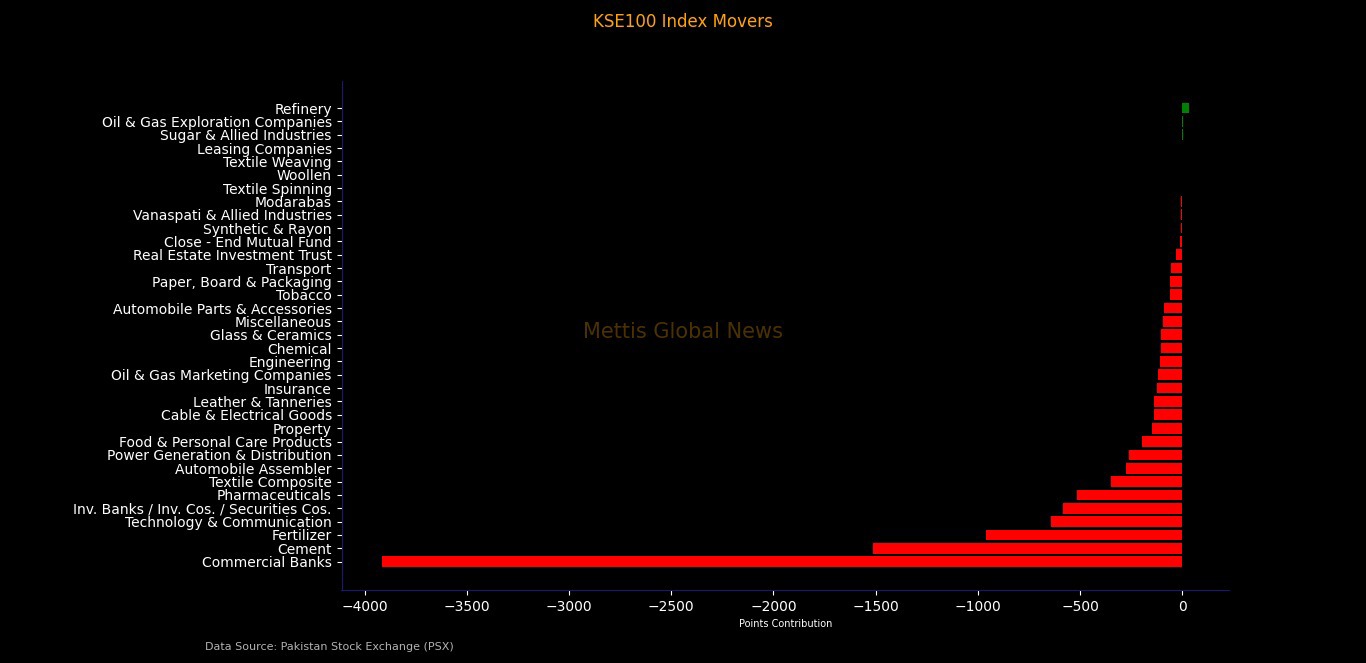

Index Movers

Sector-wise performance highlighted widespread selling

pressure across the market.

Commercial banks emerged as the largest drag, erasing

3,916.43 index points, followed by cement which shaved 1,511.18

points from the benchmark.

Fertilizer stocks reduced the index by 959.32

points, while technology and communication trimmed 642.84 points.

Investment banks and securities companies dragged the index down by 584.02

points, while pharmaceuticals contributed a decline of 515.10

points.

Other sectors that weighed heavily on the benchmark included

textile composite, automobile assemblers, power generation companies, food

and personal care products, oil marketing companies, engineering, and chemicals,

reinforcing the broad-based nature of the market downturn.

On the positive side, gains were extremely limited. Refineries

added 33.63 points, while oil and gas exploration companies contributed

a marginal 5.91 points, and sugar sector stocks provided a small

positive contribution of 2.03 points.

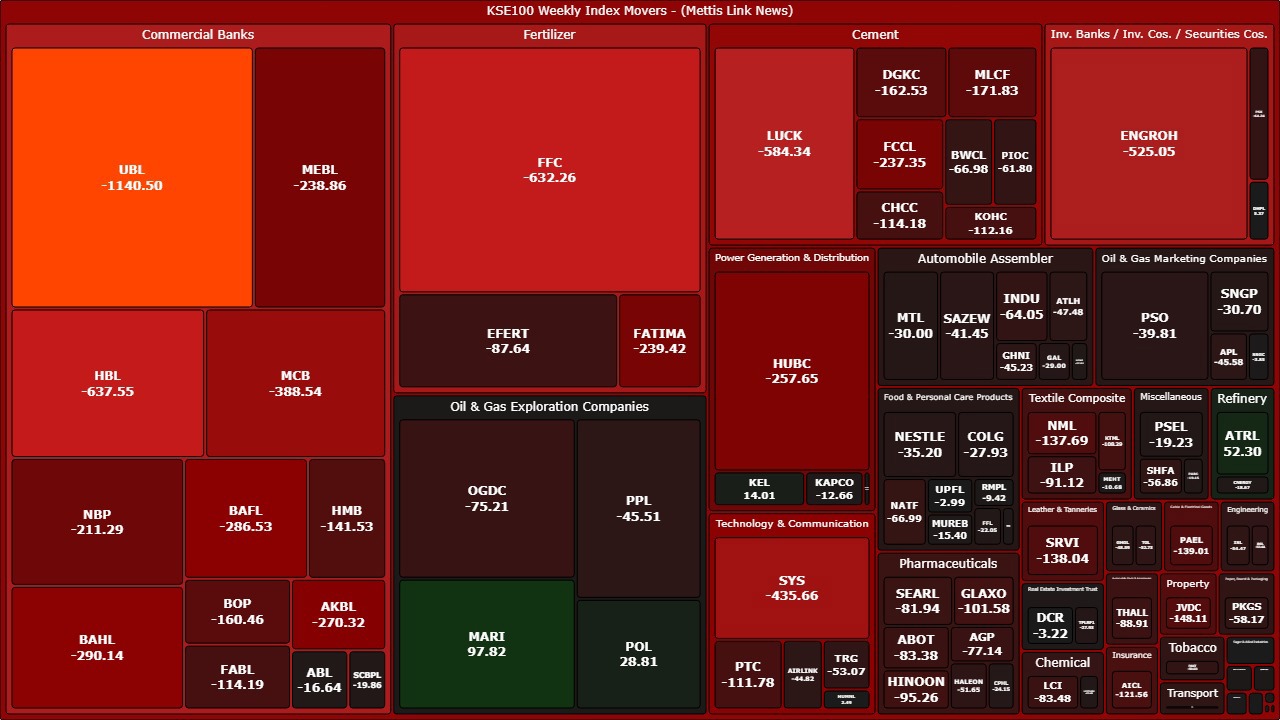

At the company level, only a handful of stocks managed to

record positive contributions.

Among the gainers, MARI added 97.82 points,

followed by ATRL which contributed 52.30 points, and POL

which added 28.81 points. K-Electric (KEL) also provided modest

support to the index with 14.01 points.

Despite these gains, the benchmark remained under

significant pressure due to sharp declines in several heavyweight stocks.

UBL emerged as the largest drag, wiping out 1,140.50

points from the index. HBL followed with a 637.55-point decline,

while FFC erased 632.26 points.

LUCK dragged the index down by 584.34 points,

while ENGROH reduced it by 525.05 points. Systems Limited

(SYS) also weighed heavily on the benchmark with a decline of 435.66

points.

Other notable decliners included MCB, BAHL, BAFL, AKBL,

HUBC, FATIMA, MEBL, FCCL, and DGKC, reflecting strong selling pressure in

major large-cap stocks.

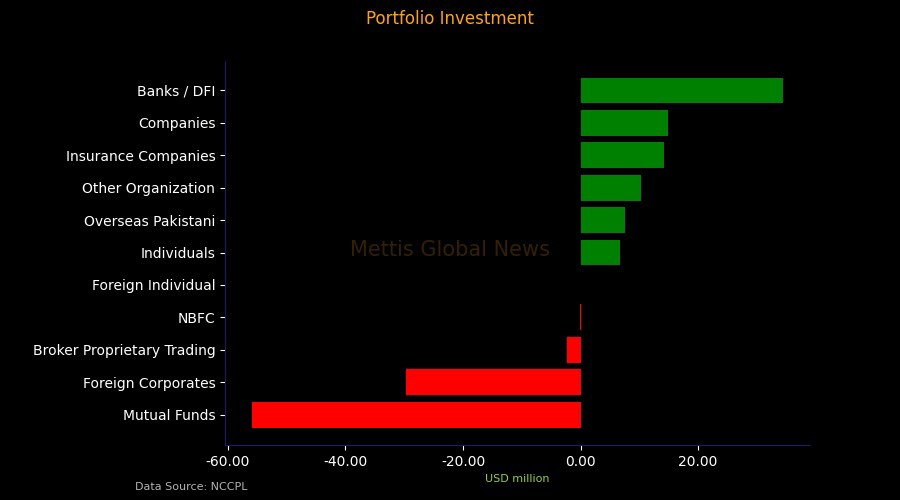

FIPI / LIPI

Foreign investment flows continued to exert pressure on the

market during the week.

Under Foreign Portfolio Investment (FIPI), foreign

investors remained net sellers with an outflow of $22.11m.

The majority of the selling came from foreign corporates,

which offloaded $29.69m worth of equities, while overseas Pakistanis

provided buying support of $7.56m. Foreign individuals recorded marginal

net buying of $23.7k.

On the other hand, local investors absorbed the entire

foreign outflow, resulting in a matching net inflow of $22.11m under

Local Portfolio Investment (LIPI).

Within local participants, banks and DFIs emerged as the

largest buyers with net purchases of $34.51m, followed by insurance

companies ($14.12m), companies ($14.95m), other organizations

($10.25m), and individual investors ($6.75m).

Meanwhile, mutual funds recorded the largest selling with

an outflow of $55.97m, followed by broker proprietary trading desks

($2.37m) and NBFCs ($0.14m).

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,040.00 | 64,680.00 62,605.00 | -1045.00 -1.63% |

| BRENT CRUDE | 78.54 | 79.80 77.28 | 2.53 3.33% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.85 | 75.08 72.61 | 2.44 3.42% |

| SUGAR #11 WORLD | 14.84 | 14.98 14.65 | -0.04 -0.27% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|