IMF flags Pakistan's narrow tax base, structural gaps

MG News | May 15, 2026 at 11:45 AM GMT+05:00

May 15, 2026 (MLN): The International Monetary Fund

has flagged Pakistan's persistently narrow tax base, undertaxed agriculture

sector, and deteriorating GST efficiency as central risks to the country's

fiscal programme, even as Pakistan pushes ahead with sweeping reforms under the

Extended Fund Facility all against the backdrop of a significant supply shock,

the Middle East war, and heightened global uncertainty.

FISCAL CONSOLIDATION AND THE REVENUE CHALLENGE

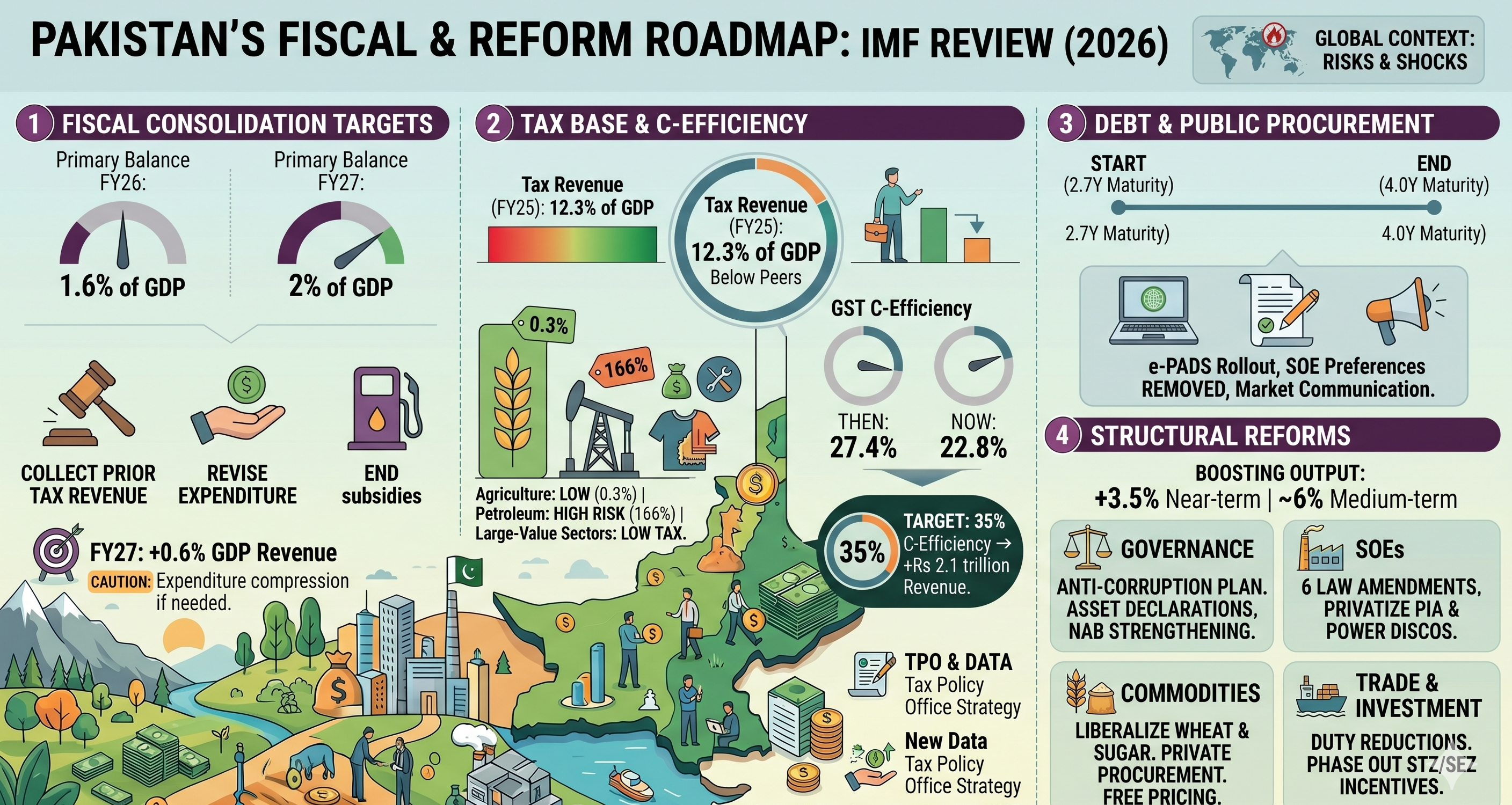

Pakistan's fiscal strategy for the near term rests on two

sequential targets. The FY26 underlying primary balance target stands at 1.6%

of GDP, while FY27 is set at 2% of GDP, a level the IMF describes as

appropriate given Pakistan's limited fiscal space and the need to bring public

debt down to more sustainable levels, according to the IMF's 2026 Staff Report

To plug a projected shortfall in Federal Board of Revenue

(FBR) collections in FY26, the authorities have moved on two fronts as prior

actions: collecting overdue tax revenue from recent court rulings in FBR's favor

worth approximately 0.3% of GDP, largely from the "super tax" and

revising expenditure ceilings by 0.1% of GDP related to unused emergency

response allocations.

Domestic fuel prices have also been aligned with

international prices as a prior action, ending subsidies the report describes

as distortionary and fiscally unsustainable. Any future fiscal response to high

fuel prices must be targeted, limited, temporary, and budget neutral.

Reaching the FY27 target requires additional revenue

collection measures of 0.6% of GDP. An FBR revenue collection floor is proposed

as a quantitative performance criterion beginning December 2026.

IMF warns that further expenditure compression, including

cuts to lower-priority capital spending, may be necessary if revenue risks materialize.

It also stresses that any interest-bill savings should be set aside rather than

spent, to protect the consolidation path and build fiscal buffers.

THE TAX BASE PROBLEM

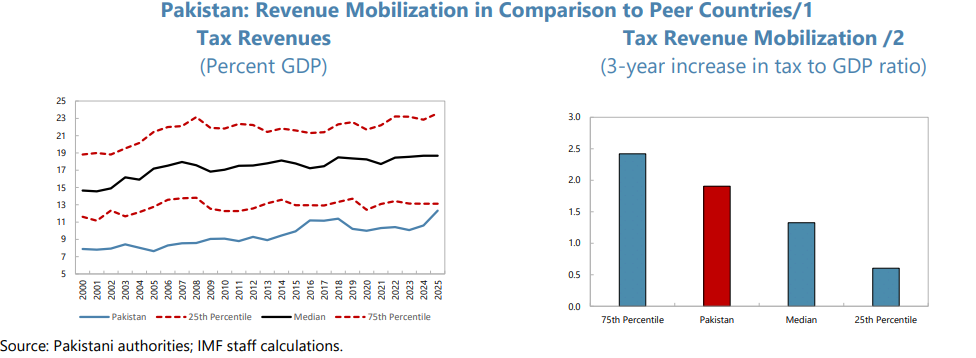

Despite reaching their highest tax-to-GDP ratio since at

least 2000, Pakistan's tax revenues, at 12.3% of GDP in FY25 including

provincial taxes and the petroleum development levy, remain below the 25th

percentile of peer countries.

The IMF identifies deep structural distortions in the tax

base:

|

Sector |

Share of Value Added |

Effective Tax Rate |

|

Agriculture |

24.6% |

0.3% |

|

Petroleum Products |

- |

166% |

|

Textiles, Real Estate, Business Services |

High |

Low relative to value added |

Agriculture is identified as the single largest undertaxed sector. Although provincial agricultural income tax rates were raised significantly in 2025 to align with rates applied to other income, revenues fell below expectations due to implementation delays and enforcement gaps. At the other extreme, petroleum products carry an effective tax rate of 166%, leaving the revenue base dangerously concentrated and exposed to commodity price shocks.

GST efficiency has also deteriorated. The GST C-efficiency

ratio has fallen from 27.4% to 22.8% over the past decade.

Pakistan's 18% standard rate is not low by regional

standards, yet barely one quarter of the theoretical tax base is actually

taxed.

Exemptions on residential property sales and certain foods,

historical zero-rating in export sectors, and post-devolution fragmentation

into four separate provincial GST-on-services regimes have compounded the

problem.

The IMF estimates that raising C-efficiency to just 35%

still well below peers such as Turkey, Morocco, and Indonesia would generate

roughly Rs 2.1 trillion in additional GST revenue, equivalent to 1.8% of GDP.

A newly created Tax Policy Office (TPO) is intended to drive

medium-term tax reform strategy. A data sharing arrangement between the TPO and

FBR has been signed, and the office has begun consulting stakeholders. However,

the report cautions that any proposals must be carefully calibrated, tested,

and communicated to ensure long-term policy stability.

DEBT MANAGEMENT AND PUBLIC PROCUREMENT

The average time to maturity of Pakistan's local currency

domestic debt stock rose to approximately 4 years by end-December 2025, up from

2.7 years at the programme's outset, reflecting efforts to extend domestic

maturities and reduce rollover risk.

The authorities are also working toward publishing an action

plan for local currency bond market development by end-September 2026, with

investor base diversification listed as a priority given what the report

describes as a significant sovereign-bank nexus.

A new fiscal risk monitoring framework published in December

2025 establishes a consistent approach for tracking contingent liabilities in

public-private partnership projects. The report stresses that market

communication around the debt management strategy must be strengthened,

particularly amid heightened uncertainty, while fully respecting

market-determined interest rates.

On public procurement, the digitised e-PADS system continues

to be rolled out across federal and provincial agencies. Proposed legal

amendments to Public Procurement Regulatory Authority rules would eliminate

preferences for state-owned enterprises in procurement contract awards without

competition, subject to limited and reasonable exceptions, with an

end-September 2026 deadline.

STRUCTURAL REFORMS: GOVERNANCE, SOEs, AND MARKETS

Cross-country evidence cited by the IMF suggests that a

comprehensive structural reform package could boost Pakistan's near-term output

by up to 3.5% and medium-term output by nearly 6%, with governance and external

sector reforms delivering particularly large returns.

On governance, the Prime Minister's Economic Governance

Reform Plan, published in December 2025 based on the IMF's Governance and

Corruption Diagnostic, sets out 15 reform actions with key performance

indicators and monitoring modalities.

Civil servant conduct rules have been revised to require

online publication of asset declarations for senior federal officials.

Amendments to the National Accountability Bureau Ordinance intended to

strengthen the appointment process for the NAB chairman and require publication

of investigation and prosecution rules are to be submitted to parliament by

end-January 2027.

On state-owned enterprises, six amendments to SOE-dedicated

laws were sent to parliament in January 2026.

Pakistan International Airlines is among two privatizations

agreed upon since October 2025. IMF urges the authorities to finalize a new

financial advisor appointment for the Roosevelt Hotel and to move forward with

private sector participation in power distribution companies (DISCOs).

Sovereign Wealth Fund law amendments, described as essential

to maintaining reform momentum, are pending parliamentary adoption.

In commodity markets, reducing government intervention in

wheat and sugar is highlighted as essential.

A new national sugar sector policy is being developed with a

target of end-June 2026, envisaging the removal of zoning and licensing

restrictions, an end to administered pricing of cane and sugar, and the liberalization

of imports and exports. Wheat reserve governance is to be kept robust, with

procurement conducted through the private sector at internationally aligned

prices.

The next phase of duty reductions under the National Tariff Policy is to be legislated in the FY27 budget. Fiscal incentives for special economic zones, special technology zones, and export processing zones are to be phased out by 2035 to reduce fiscal costs and level the playing field for trade and investment.

Copyright Mettis

Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,850.00 | 66,020.00 64,290.00 | 230.00 0.36% |

| BRENT CRUDE | 83.50 | 84.44 81.50 | 1.01 1.22% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 105.50 105.50 | -0.25 -0.24% |

| ROTTERDAM COAL MONTHLY | 116.25 | 117.00 116.25 | -0.10 -0.09% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.20 | 78.77 76.53 | 0.91 1.18% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|