AGP eyes up to 49% upside on mega OBS merger plan

MG News | June 09, 2026 at 01:14 PM GMT+05:00

June 09, 2026 (MLN): AGP Limited is set to become a significantly larger pharmaceutical entity following OBS Group's planned consolidation of its three subsidiaries into the listed company, JS Global Capital reiterating its Buy rating and flagging up to 49% upside from current levels.

At a last closing price of Rs184.09, the stock offers 36%

upside to JS Global's base-case target price of Rs250 per share, with an

additional 10% potential taking the post-merger target to Rs275 contingent on

the successful completion of the consolidation.

The stock's 52-week range stands at Rs168.53–Rs243.29, with

a market capitalisation of Rs51.8bn ($86.1m) and a free float of 30.

|

Key statistics |

|

|

Target Price PKR |

250 |

|

Current Price PKR |

184.09 |

|

Sector |

Pharmaceuticals |

|

52w high / Low (PKR) |

243.29 / 168.53 |

|

3m avg. turnover (USD

'000) |

458.9 |

|

Free float (%) |

30 |

|

Issued shares (mn) |

280 |

|

Market capitalization |

PKR 51.8Bn / USD 86.1Mn |

|

Source: Company

accounts, JS Research |

|

The Merger Scheme

OBS Group is planning to merge three entities into AGP Ltd

OBS Pharma (Private) Limited, in which the Group holds an 80% stake, along with

AGP's two existing subsidiaries, OBS AGP (Private) Limited and OBS Pakistan

(Private) Limited.

The objective is to unlock synergies across supply chain,

marketing, financial optimisation, product portfolio, and risk diversification,

ultimately creating value for shareholders.

The merger scheme was originally intended to become

effective from January 2026, subject to court approval.

Management expects all requisite regulatory approvals from

shareholders, regulators, and the courts to be obtained within calendar year

2026. Notably, AGP has called an Extraordinary General Meeting (EOGM) on June

29, 2026 to seek shareholder approval for the merger scheme, an increase in

authorised capital, and a proposed name change from AGP Limited to OBS AGP

Limited.

Financial Impact

JS Global's crude estimates pending further regulatory

clarity and inter-company transaction details suggest the merger will

materially expand AGP's financial base.

On a consolidated post-merger basis, CY26E and CY27E

revenues are projected at Rs41.4bn and Rs48.1bn respectively, representing a

30% and 28% increase over the pre-merger base-case estimates of Rs31.8bn and

Rs37.5bn.

Profit after tax (PAT) attributable to shareholders is

expected to rise 52% in CY26E and 55% in CY27E, reaching Rs6.6 billion and

Rs8.0bn compared to Rs4.3bn and Rs5.1bn under the pre-merger case.

The elimination of minority interest (NCI) following full

consolidation is a key driver of this improvement.

However, EPS accretion is partially diluted by the issuance

of approximately 108 million new shares, bringing total outstanding shares to

388.7 million post-merger from the current 280 million.

Post-merger EPS is estimated at Rs16.97 and Rs20.55 for

CY26E and CY27E respectively, representing a 10–12% uplift over the pre-merger

EPS of Rs15.47 and Rs18.36.

On the balance sheet, total assets are projected to expand

37% in CY26E to Rs45.9bn, with total liabilities rising 49% to Rs20.7 billion.

The gearing ratio (debt to debt-plus-equity) is expected to

increase from 30% to 36% in CY26E before declining to 29% by CY27E, showing the

absorption of approximately Rs2.7bn in new debt alongside OBS Pharma's existing

Rs4bn long-term debt.

Gross margins are expected to remain broadly stable at

around 57.6–58.0% post-merger.

Financial charges are estimated to double in CY26E to Rs2.1bn

from Rs1.0bn, normalising to Rs1.7bn in CY27E, compared to Rs867m in the

pre-merger scenario.

|

Impact of the merger on

AGP Financials |

||||||

|

AGP Ltd (Current) |

AGP Ltd (Post merger) |

% Change |

||||

|

Rs(million) |

CY26E |

CY27E |

CY26E |

CY27E |

CY26E |

CY27E |

|

P&L Summary |

||||||

|

Revenue |

31,760 |

37,483 |

41,387 |

48,058 |

30% |

28% |

|

Gross Profit |

18,424 |

21,841 |

23,830 |

27,852 |

29% |

28% |

|

Financial Charges |

1,035 |

867 |

2,073 |

1,697 |

100% |

96% |

|

PAT |

5,054 |

6,048 |

6,598 |

7,985 |

31% |

32% |

|

NCI |

724 |

907 |

0 |

0 |

-100% |

-100% |

|

PAT after NCI |

4,330 |

5,141 |

6,598 |

7,985 |

52% |

55% |

|

Gross margin |

58.00% |

58.30% |

57.60% |

58.00% |

-0.40% |

-0.30% |

|

PAT margin |

15.90% |

16.10% |

15.90% |

16.60% |

0.00% |

0.50% |

|

EPS (Rs) |

||||||

|

@280m shares |

15.47 |

18.36 |

||||

|

@389m shares |

16.97 |

20.55 |

10% |

12% |

||

|

Balance Sheet Summary |

||||||

|

Total Assets |

33,557 |

37,252 |

45,896 |

49,399 |

37% |

33% |

|

Total Liabilities |

13,859 |

14,367 |

20,700 |

20,362 |

49% |

42% |

|

Equity |

19,698 |

22,886 |

25,196 |

29,037 |

28% |

27% |

|

Gearing ratio = D/ (D+E) |

30% |

26% |

36% |

29% |

5.80% |

3.00% |

|

Source: JS estimates |

||||||

Valuation

At the post-merger CY27E P/E of 11x, AGP trades at a 25%

discount to its historical average P/E of 14.4x. On a pre-merger CY26E P/E

basis, AGP trades at 11.9x, below the sector's trailing four-quarter average

P/E of 12.7x. The post-merger CY26E P/E compresses further to 10.8x.

Sector comparative data shows AGP leading peers on gross

margin at 60%, with an operating margin of 28% and net margin of 13% on a

trailing basis, against a sector sample average of 42%, 22%, and 12%

respectively.

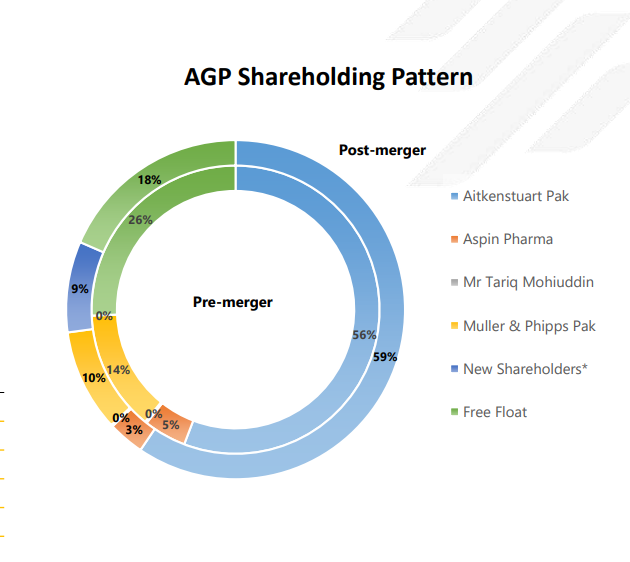

Ownership Structure

Post-merger, 91m new AGP shares will be issued to

shareholders of OBS Pharma, 22m to minority shareholders of OBS AGP, and 2.73m

to minority shareholders of OBS Pakistan.

Aitkenstuart Pakistan's shareholding will rise from 156.25m shares

to 231.20m shares, increasing OBS Group's effective holding in AGP from 60.8%

to 63%.

Newly admitted shareholders being current minorities of the

three merging entities will be subject to a lock-in period and will not form

part of free float immediately post-issuance.

Free float remains unchanged at 71.83m shares, declining as

a percentage from 26% to 18% of expanded total capital.

Revenue Profile and Product Portfolio

The merged entity's top-10 products will contribute 65% of

total revenues, led by Azomax (Rs5.0bn, 14% share), Rigix (Rs3.9bn, 11%),

Gravibinan (Rs3.0bn, 8%), Osnate D (Rs2.4bn, 7%), and Norvasc (Rs2.1bn, 6%).

|

AGP (post merger) - Top

10 Products |

||

|

Product |

Revenue (Rs.000) |

% contribution |

|

Azomax |

5,003 |

14% |

|

Rigix |

3,928 |

11% |

|

Gravibinan |

2,959 |

8% |

|

Osnate D |

2,419 |

7% |

|

Norvasc |

2,051 |

6% |

|

Primolut N |

1,913 |

5% |

|

Ceclor |

1,773 |

5% |

|

Ciproxin |

1,487 |

4% |

|

Travocort |

1,052 |

3% |

|

Spasler-P |

884 |

2% |

|

Others |

12,761 |

35% |

|

Source: AGP CBS Presentation, Company accounts, Company notice, JS Research | ||

The addition of OBS Pharma will shift the non-essential

(deregulated) drug share from 65% to 68% of consolidated revenues.

AGP Ltd (Standalone Former Eli Lilly Business)

contributed net sales of Rs20.5bn in CY25, with gross margins of approximately

49% and PAT margins of 11%.

Over 90% of its revenues come from non-essential drugs.

Rigix is the largest standalone revenue contributor at 25% and is expected to

be the second-largest in the merged entity.

OBS Pharma (Former Bayer's Business), Pakistan's

leading women's healthcare company, posted net sales of Rs9.1 billion in CY25

(Rs8.7bn post inter-group transactions) and a gross margin of 53%. Its top

products Gravibinan and Primolut N dominate their respective domestic segments.

The company recently won a hardship case for Resochin, its

anti-malaria product, providing a potential upside to estimates. OBS Pharma's

CY26E net sales are projected at Rs10.1bn with a PAT of Rs1.7bn.

OBS AGP (Former Sandoz Business), formed in 2021

through the acquisition of the Sandoz AG portfolio, derives 63% of its revenues

from Azomax alone (Rs4.8bn in CY25), with gross margins exceeding 50%. AGP

currently holds a 65% stake in this entity.

OBS Pakistan (Former Viatris/Pfizer Business), a 92%

owned AGP subsidiary, enjoys the highest gross margins among group companies

above 70% driven by the internalisation of key products. Norvasc (Rs2bn in

sales) is its largest revenue contributor, accounting for 26% of its portfolio.

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.51 | 79.80 77.28 | 2.50 3.29% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.84 | 75.08 72.61 | 2.43 3.40% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|