The Twilight of Pakistan’s Economy

By Muhammad Ghazanfar Sakrani | June 05, 2023 at 11:15 AM GMT+05:00

June 05, 2023 (MLN): The fiscal year 2023 is about to bid farewell, a year that proved to be gloomy for Pakistan’s economy. Amid political uncertainty along with the Russia-Ukraine war, the economic performance of the country is no less than a fiasco.

The foremost reason for the incumbents initiating an ouster campaign against then prime minister Imran Khan was the heating inflation. CPI for March 2022, the last month of Khan’s rule was recorded at 12.7%; however, CPI for April ballooned to 38%, the highest level in the country’s history.

Prices of essential items even doubled during this period, attriting the purchasing power of people. This was also evidenced by Eid celebrations with empty pockets, where shopkeepers described this year as the worst ever in at least a decade.

The current account deficit of the country stood at $3.25 billion in the first 10 months of the fiscal year 2023 compared to $13.65 billion in the same period last year. On the face of it, this seems upbeat.

However, the reduction in deficit was on the backdrop of import compression measures, which resulted in a shortage of raw materials for industries causing unemployment of at least 8 million workers and even the closure of industries. In the same period, exports and remittances also slumped by almost 13%.

The policy rate, which settled at 13.75% towards the end of fiscal year 2022 has now touched the record high level of 21% with a hawkish stance to persist amid rising inflation and IMF stipulations.

Though the rising policy rate has failed to arrest the surging inflation, it has jeopardized businesses with many units shutting down and people losing their livelihoods.

The Business Confidence Index, published monthly by the SBP in collaboration with the Institute of Business Administration, Karachi, has been on a downward spiral since October 2022, as it decreased from 46.3 points to 37.5 points in March 2023.

After the successful completion of the seventh and eighth reviews by the IMF board resulting in the release of a tranche worth $1.17bn, the successful completion of the ninth review remains in limbo since January.

The dilly-dally of Dar in adhering to the proviso of the fund initially led to the delay. However, in January, the government removed the artificial cap on the exchange rate which led to the arrival of the IMF staff mission in January.

In February, the government introduced a mini-budget to comply with the fund’s requirement which brought it a step closer to the unlocking of funds.

The bone of contention now lies in the external funding requirements where the fund demands additional commitments to the tune of $6bn. IMF will also keep a close eye on the budget document to avert any variance by the authorities.

To say the least, PKR has been one of the worst-performing currencies since April 2022. In the last 14 months, the local currency shed almost 50% against the greenback.

The gap between open market and inter-bank rates cost the country almost $2bn in remittances. Once again, this widening gap with the dollar hovering around Rs315 in the open market lures hawala/hundi for remittances, adversely affecting the already dollar-starved economy.

The currency depreciation is the antithesis to Dar’s claims who boastfully pretended to bring the dollar south of Rs.200 as he assumed office. The appreciation of PKR as Dar assumed office was ephemeral, it is again in a precarious state with revival mainly dependent on the release of the IMF 9th tranche.

The government released the National Account Numbers for FY23 which reveal the performance of other major economic indicators, though the validity of these figures remains dubious. As per the press release, the provisional growth in the industrial sector is -2.94%.

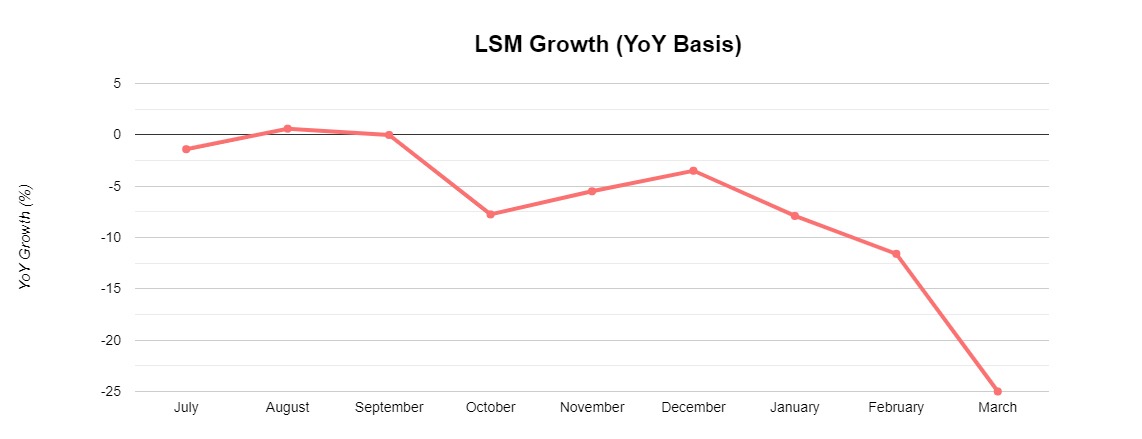

The heydays of Large Scale Manufacturing (LSM) in FY21 and FY22 where for the first time since FY05 LSM witnessed back-to-back double-digit growth is now over.

In FY23, LSM contracted by almost 8%. This owes largely to the government’s demand contraction policies by curbing imports to check the fragile external account position.

This nosedive in LSM growth raises eyebrows on the 9% growth figure of small-scale manufacturing as they both are vertically linked.

The months of July-September created havoc for the backbone of the country’s economy. This resulted in colossal damage of an estimated $30bn as per the assessments report. 45% of the total cotton crop followed by 31% of rice and 7% of the sugarcane crop fell into ruin.

As per the latest statistics, the uptick in wheat, cotton and maize production together with other crops led to a provisional growth of 1.55% in this pivotal sector.

Considering the damages stated by the government itself in its report which estimated the total damage to the country amid floods, experts look at this figure with askance.

As per official statistics, GDP grew at a rate of 0.29% after a couple of years of growth of nearly 6%. Considering the ground realities, the 0.29% growth figure seems perfidious, GDP must have been contracted by 2-3 percent.

The bleak economy coupled with political uncertainty makes foreign investors chary while investing. Net FDI has declined by almost 22.5% in the nine months of the fiscal year 2023 compared to the same period last year. Investors are biding their time for the dust to settle down and the economy to thrive again.

Does the future of the economy remain sanguine? It depends on the revival of the IMF program and the settling down of political instability.

Until then, the government seems devoid of any plan to circumvent the ongoing crisis.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 130,686.66 280.01M |

0.26% 342.63 |

| ALLSHR | 81,305.25 897.01M |

0.35% 281.26 |

| KSE30 | 39,945.45 114.02M |

0.09% 37.19 |

| KMI30 | 190,698.05 148.61M |

0.61% 1163.05 |

| KMIALLSHR | 55,074.15 495.43M |

0.53% 290.50 |

| BKTi | 34,568.40 28.73M |

-1.07% -372.33 |

| OGTi | 28,739.35 22.59M |

1.57% 443.29 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 110,160.00 | 110,525.00 110,055.00 |

-255.00 -0.23% |

| BRENT CRUDE | 68.70 | 68.89 68.66 |

-0.10 -0.15% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

-0.75 -0.76% |

| ROTTERDAM COAL MONTHLY | 108.45 | 109.80 108.45 |

-0.55 -0.50% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.98 | 67.18 66.95 |

-0.02 -0.03% |

| SUGAR #11 WORLD | 16.37 | 16.40 15.44 |

0.79 5.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|