PSX Closing Bell: In the Dark

By MG News | September 11, 2024 at 04:22 PM GMT+05:00

September 11, 2024 (MLN): Pakistani stocks fell on Wednesday, erasing yesterday's gains ahead of the monetary policy meeting, where the central bank is widely expected to lower rates for the third consecutive time.

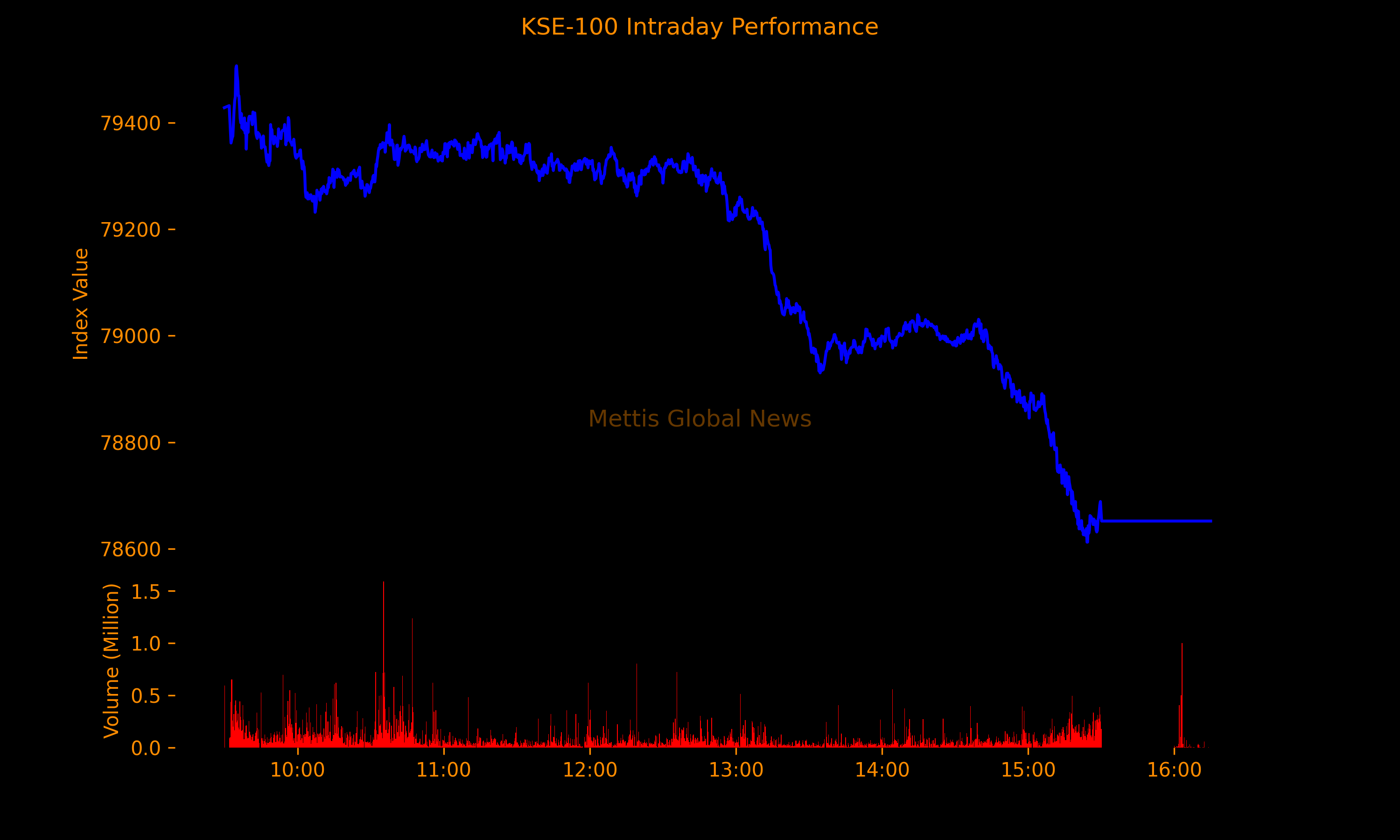

The benchmark KSE-100 Index concluded the trading session at 78,651.79, down 634.94 points or 0.80% fueled by late-session selling.

The State Bank of Pakistan (SBP) has slashed interest rates by a cumulative 250 basis points in the last two meetings and is scheduled to meet again tomorrow.

Investors had earlier expected a larger rate cut than the currently anticipated 150bps, which has likely led to profit-taking.

At the same time, there is still no update on the International Monetary Fund (IMF) executive board's approval of Pakistan's $7 billion bailout package.

Earlier in July, Pakistani authorities and the IMF team reached a staff-level agreement. However, the agreement is subject to approval by the IMF’s Executive Board and the timely confirmation of necessary financing assurances from Pakistan’s development and bilateral partners.

Throughout today's trading session, the index traded in a range of 895.01 points showing an intraday high of 79,507.17 (+220.44) and a low of 78,612.16 (-674.57) points.

The total volume of the KSE-100 Index was 146.52 million shares.

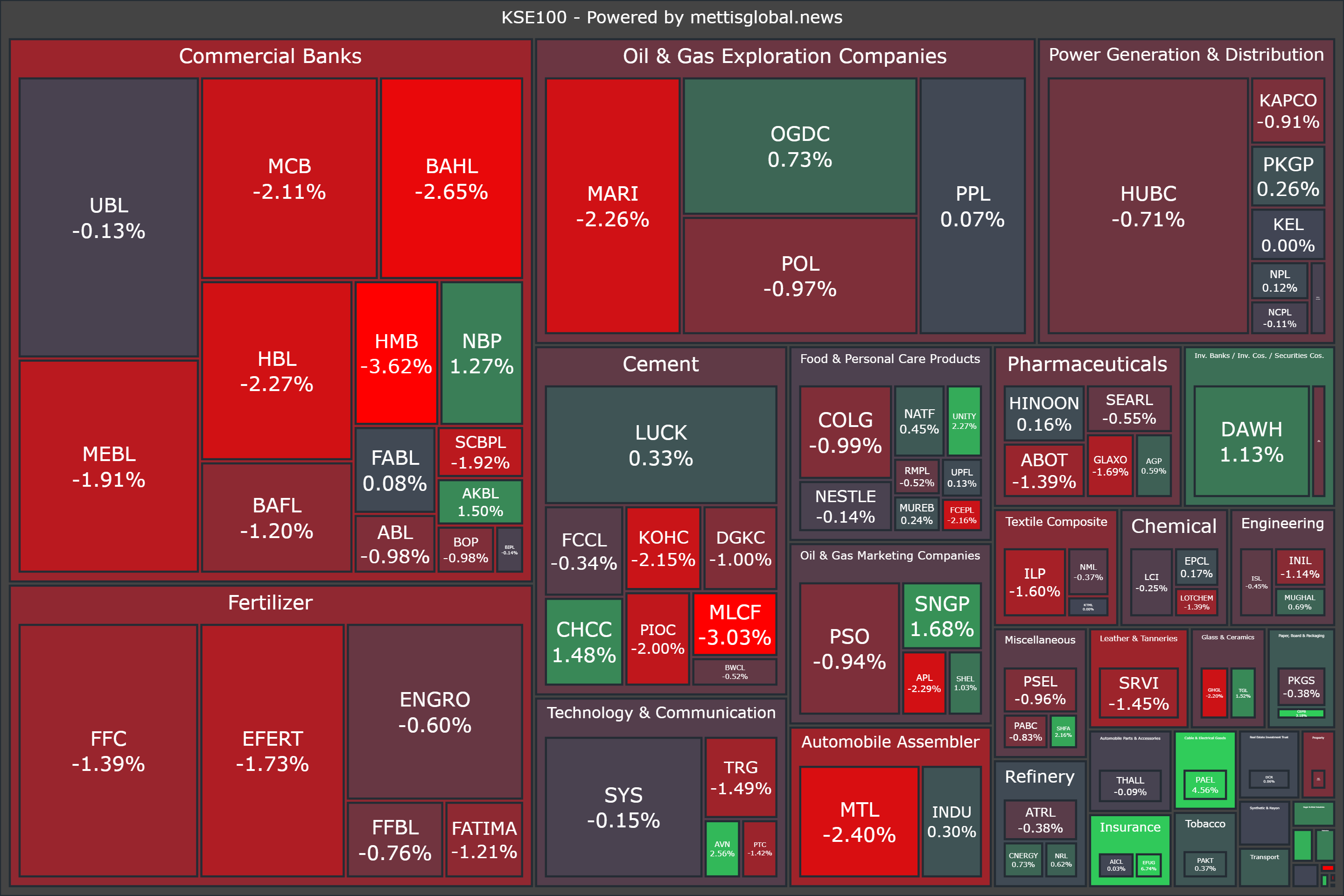

Of the 100 index companies 37 closed up, 59 closed down, while 4 were unchanged.

Top losers during the day were YOUW (-3.72%), HMB (-3.62%), BNWM (-3.04%), MLCF (-3.03%), and PGLC (-2.84%).

On the other hand, top gainers were EFUG (+6.74%), PAEL (+4.56%), CEPB (+3.18%), POML (+2.58%), and AVN (+2.56%).

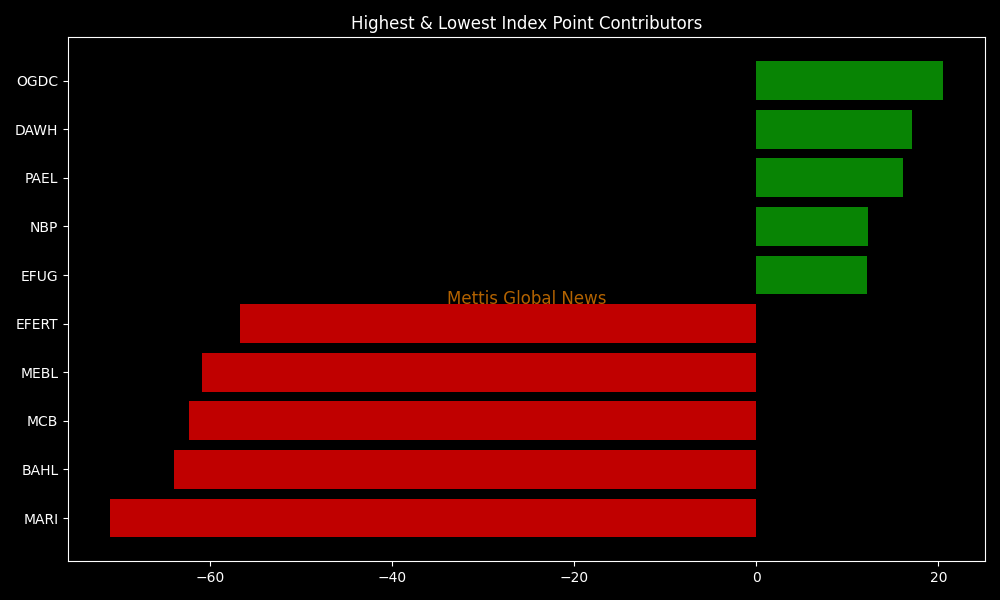

In terms of index-point contributions, companies that dragged the index lower were MARI (-71.05pts), BAHL (-64.01pts), MCB (-62.39pts), MEBL (-60.88pts), and EFERT (-56.78pts).

Meanwhile, companies that added points to the index were OGDC (+20.53pts), DAWH (+17.11pts), PAEL (+16.09pts), NBP (+12.28pts), and EFUG (+12.13pts).

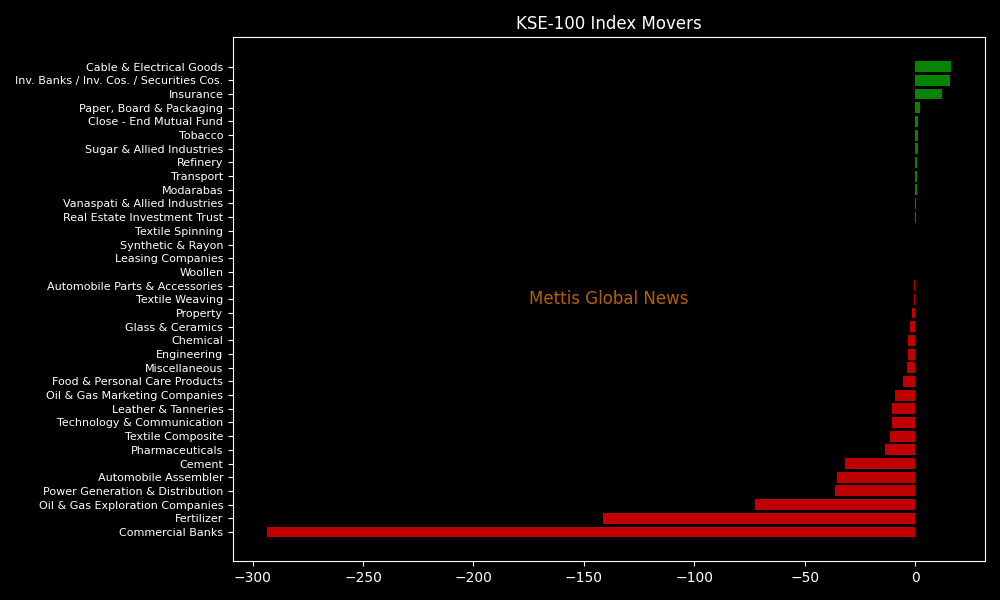

Sector-wise, KSE-100 Index was let down by Commercial Banks (-293.40pts), Fertilizer (-141.36pts), Oil & Gas Exploration Companies (-72.76pts), Power Generation & Distribution (-36.34pts), and Automobile Assembler (-35.40pts).

While the index was supported by Cable & Electrical Goods (+16.09pts), Inv. Banks / Inv. Cos. / Securities Cos. (+15.87pts), Insurance (+12.20pts), Paper, Board & Packaging (+2.13pts), and Close - End Mutual Fund (+1.28pts).

In the broader market, the All-Share Index closed at 50,777.65 with a net loss of 264.23 points or 0.52%.

Total market volume was 532.73 million shares compared to 509.49m from the previous session while traded value was recorded at Rs14.74 billion showing an increase of Rs0.97bn.

There were 232,507 trades reported in 439 companies with 178 closing up, 206 closing down, and 55 remaining unchanged.

| Symbol | Price | Change % | Volume |

|---|---|---|---|

| WTL | 1.5 | -1.32% | 80,930,490 |

| PAEL | 26.85 | 4.56% | 42,596,524 |

| WAVESAPP | 9.42 | 10.95% | 34,023,632 |

| KOSM | 9.72 | -3.38% | 32,247,600 |

| SLGL | 18.17 | -1.30% | 17,406,824 |

| CNERGY | 4.13 | 0.73% | 14,944,941 |

| PACE | 6.4 | -0.93% | 14,794,158 |

| HUMNL | 10.94 | 1.96% | 14,490,082 |

| SYM | 10.72 | 2.98% | 13,467,741 |

| AGL | 38.84 | 10.00% | 12,831,810 |

To note, the KSE-100 has gained 207 points or 0.26% during the fiscal year, whereas the ongoing calendar year has witnessed a cumulative increase of 16,201 points, equivalent to 25.94%.

Copyright Mettis Link News

Related News

.jpeg)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 129,752.39 186.68M |

1.21% 1552.96 |

| ALLSHR | 80,753.00 518.04M |

1.21% 965.38 |

| KSE30 | 39,717.27 75.33M |

1.57% 612.28 |

| KMI30 | 189,007.73 66.58M |

1.12% 2092.12 |

| KMIALLSHR | 54,657.95 243.13M |

0.84% 456.07 |

| BKTi | 34,585.44 34.04M |

3.31% 1108.76 |

| OGTi | 28,259.10 7.49M |

1.06% 296.52 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 107,425.00 | 107,430.00 105,440.00 |

1675.00 1.58% |

| BRENT CRUDE | 67.04 | 67.29 66.98 |

-0.07 -0.10% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 97.50 97.50 |

0.70 0.72% |

| ROTTERDAM COAL MONTHLY | 103.80 | 0.00 0.00 |

-3.70 -3.44% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 65.33 | 65.65 65.26 |

-0.12 -0.18% |

| SUGAR #11 WORLD | 15.70 | 16.21 15.55 |

-0.50 -3.09% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|