PKR: A nightmare to remember

By MG News | October 04, 2021 at 03:26 PM GMT+05:00

October 4, 2021 (MLN): The so-called growth-oriented strategies coupled with decent macros seem helpless when it comes to the interbank market in the presence of external errors as they cannot be fixed instantly.

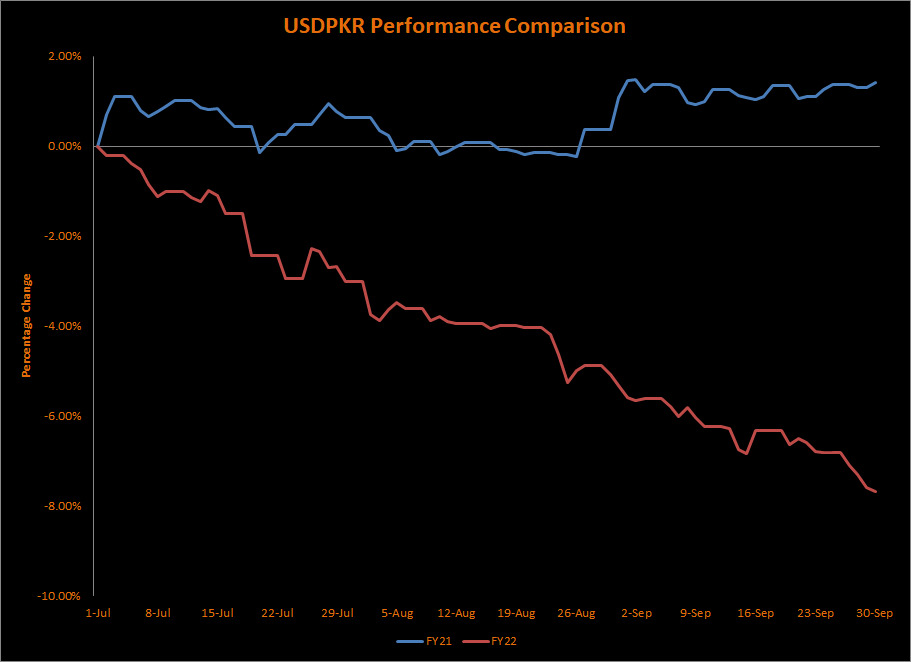

After witnessing an epoch of optimism in FY21, PKR nosedived by 7.68% or depreciated by Rs13.11 against the greenback in 1QFY22.

The month of September has been the roughest month for PKR where the currency saw its all-time low of Rs169.97 on September 28, 2021. During the month, the domestic unit dropped by 2.50% to close the trade at PKR 170.66 per USD compared to the PKR appreciation of 0.32% in September’20.

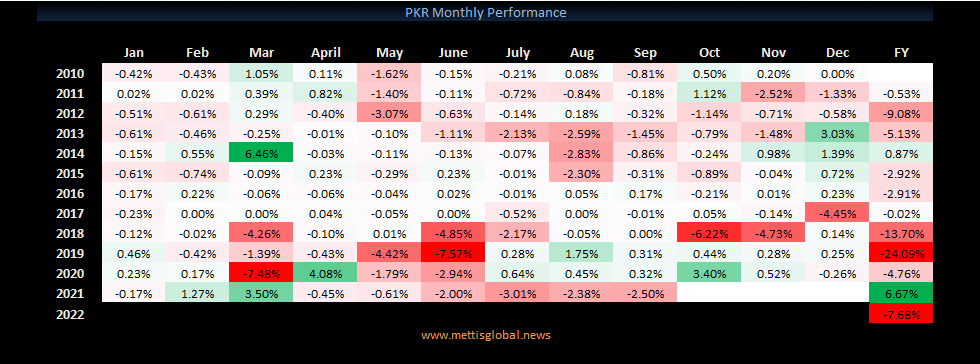

To note, the rupee took a breather in March’21 as it recorded a remarkable performance during the calendar year, wherein, the local unit had managed to gain some ground by 3.50%.

Amid geopolitical situation with regards to Afghanistan, and rising international commodity prices have played well to create havoc in the interbank market. Given the situation, the due pressure on PKR has pushed the speculative behavior of market players which also plunges the value of the rupee throughout the 1QFY22.

Experts and policymakers have raised their brows over the ongoing situation in Afghanistan and its dwindling relations with the western world as it has created not only political but also economic turbulence throughout the region. Particularly, the developing countries with sensitive currency movements have found the circumstances quite disruptive.

Furthermore, the widening trade deficit and deteriorating current account balance have pushed the rupee to swung wildly amid chaotic trading.

Fitch Solutions, in its latest report, has revised weaker its forecast for the Pakistani rupee to average PKR164.00/USD in 2021 and PKR180.00/USD in 2022, from PKR158.00/USD and PKR165.00/USD previously.

The expectation for the currency to weaken further is based on Pakistan’s worsening terms of trade, tighter US monetary policy, alongside the flow of USD out of Pakistan and into Afghanistan.

Since its last update in June 2021, PKR has depreciated by 7.1% to PKR169.31/USD and the rupee has averaged PKR159.23/USD over the first nine months of 2021. The sell-off can largely be attributed to the country’s increasing import bills, alongside external factors stemming from neighboring Afghanistan, the report added.

PKR is enduring undue pressure of Afghanistan’s turbulence. Since the international agencies have ceased their account, the country has no source to fulfill the dollar demand other than Pakistan. Previously, the bilateral trade between Pakistan and Afghanistan was carried out in US Dollars but now the same is being conducted in Pak Rupees which has also halted the supply of dollars to Pakistan, Malik Bostan, President of Forex Association of Pakistan stated while speaking to Mettis Global.

Speaking to Mettis Global, Zafar Paracha, Former Secretary-General of Exchange Companies Association of Pakistan said, In the backdrop of satisfactory performance of all the major economic indicators such as revenue collection as it increased by Rs186bn to Rs1.395tr in 1QFY22, remittances, and foreign direct investment, PKR will soon turn back to stand around 160--165 in the remaining months of FY22 if IMF does not impose any condition regarding the devaluation of the local currency.

With regards to Afghanistan’s issue, he pointed out that previously, NATO countries were spending $400-$500 million in Afghanistan which has been stopped after the Taliban’s take over. Moreover, the banking system of Afghanistan is surviving under huge pressure of freezing funds. Thus, the demand for the dollar is fulfilled by our interbank market.

He also underlined that the undocumented trade with Afghanistan put additional pressure on the sinking currency.

The local unit is also enduring the pressure of inflating import bill amid surging commodity prices in the international commodity market that has augmented the import bill by 100%. Besides, the import of the Covid-19 vaccine and boosters cost up to $2.5bn.

Though the road is slippery the State Bank of Pakistan is playing a commendable role, he mentioned.

The apt measures are taken by SBP such as revised prudential regulations for consumer financing to moderate import and demand growth in the auto sector.

In line with this, SBP has asked commercial banks to provide information about imports worth $500,000, In order to curb the free movement of the dollar.

SBP has also decided to impose 100% Cash Margin Requirements (CMR) on the import of 114 items, taking the total number of items subject to Cash Margin to 525.

The measure will help discourage imports of these items and thus support the balance of payments.

Sharing his views with Mettis Global, Asad Rizvi, the former Treasury Head at Chase Manhattan said, PKR will not ease off in days to come given the external pressure.

Regarding recent macro-economic developments, he said, it is good to know that FBR has collected Rs1.395tr. However, the foreign reserves of SBP fell by $780mn, which may further drop next week and put additional pressure on the balance of payment.

He also noted that the impact of 100% Cash margin imposed on 114 items along with consumer financing is the right step, but may not be enough to reduce dollar demand unless importers’ cash source is questioned if he/she is not a taxpayer.

The cash in circulation is already 37.2% of total commercial bank deposits (Rs19.2tr). Hence, consumers will have to pay the price and inflation will rise.

The rupee has been losing purchasing power rapidly in the domestic market, causing a rise in inflation that has badly hurt consumers, he added.

Expressing her concern over the ongoing currency crisis, Professor Dr. Shahida Wizarat, President Independent Economists and Policy Practitioners (IEPP) said that “since October 2000 I have been saying that luxury consumer goods import should be banned. None of the governments banned these luxury consumer goods.”

The government’s attempt to achieve a growth-oriented economy has inflated the import bill of all the industrial raw materials. Resultantly, the trade deficit has surged to $7.5bn in August’21.

She warned that if the same practice continues, the trade deficit will continue to broaden.

“This shows IMF strategy of growth is not compatible in the case of Pakistan,” She noted.

In addition, the excessive demand for foreign currencies in the interbank market has also plunged the value of PKR. She indicated that not only ordinary people/traders are buying but bankers are also involved in bulk buying.

Further, the crisis may catch the impact of the ongoing conflict of interest for GOP officials taking a decision on Air Lines of Communication (ALOC) to US, regarding the submission of the grant, she added.

She has also advised the government to take strict measures to curtail the import of luxury items.

Talking to Mettis Global, Ahsan Mehnti, Director Arif Habib Group said, “the ongoing devaluation of PKR is highly impacted by the market sentiments amid speculations over possible sanctions.”

While discussing rupee outlook, he said, “to halt rupee depreciation is not possible given the circumstances. However, measures taken by SBP can give some relief.”

The equity market has also felt a jolt since the depreciating currency shattered the investors’ confidence in the trading floor. However, the equity market has realized the entire impact of depreciation up till now and currently in a phase of consolidation, sharing his views with Mettis Global, Shayan Jan, Equity Trader at Intermarket Securities said.

Copyright Mettis Link News

Related News

.jpg)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 130,957.79 50.62M |

0.21% 271.13 |

| ALLSHR | 81,557.99 270.91M |

0.31% 252.74 |

| KSE30 | 40,036.53 25.47M |

0.23% 91.08 |

| KMI30 | 190,969.00 29.18M |

0.14% 270.95 |

| KMIALLSHR | 55,121.03 132.07M |

0.09% 46.87 |

| BKTi | 34,837.09 3.93M |

0.78% 268.69 |

| OGTi | 28,569.50 2.38M |

-0.59% -169.85 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,755.00 | 110,525.00 109,600.00 |

-660.00 -0.60% |

| BRENT CRUDE | 68.62 | 68.89 68.42 |

-0.18 -0.26% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

-0.75 -0.76% |

| ROTTERDAM COAL MONTHLY | 108.45 | 109.80 108.45 |

-0.55 -0.50% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.94 | 67.18 66.72 |

-0.06 -0.09% |

| SUGAR #11 WORLD | 16.37 | 16.40 15.44 |

0.79 5.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|