Pakistani banks continue to flourish with strong quarterly profits

Rafay Malik | September 11, 2024 at 12:56 PM GMT+05:00

September 11, 2024 (MLN): Extending their streak of financial success, Pakistan’s commercial banks have closed another quarter scoring higher earnings driven by increased interest income, non-markup income and provision reversals.

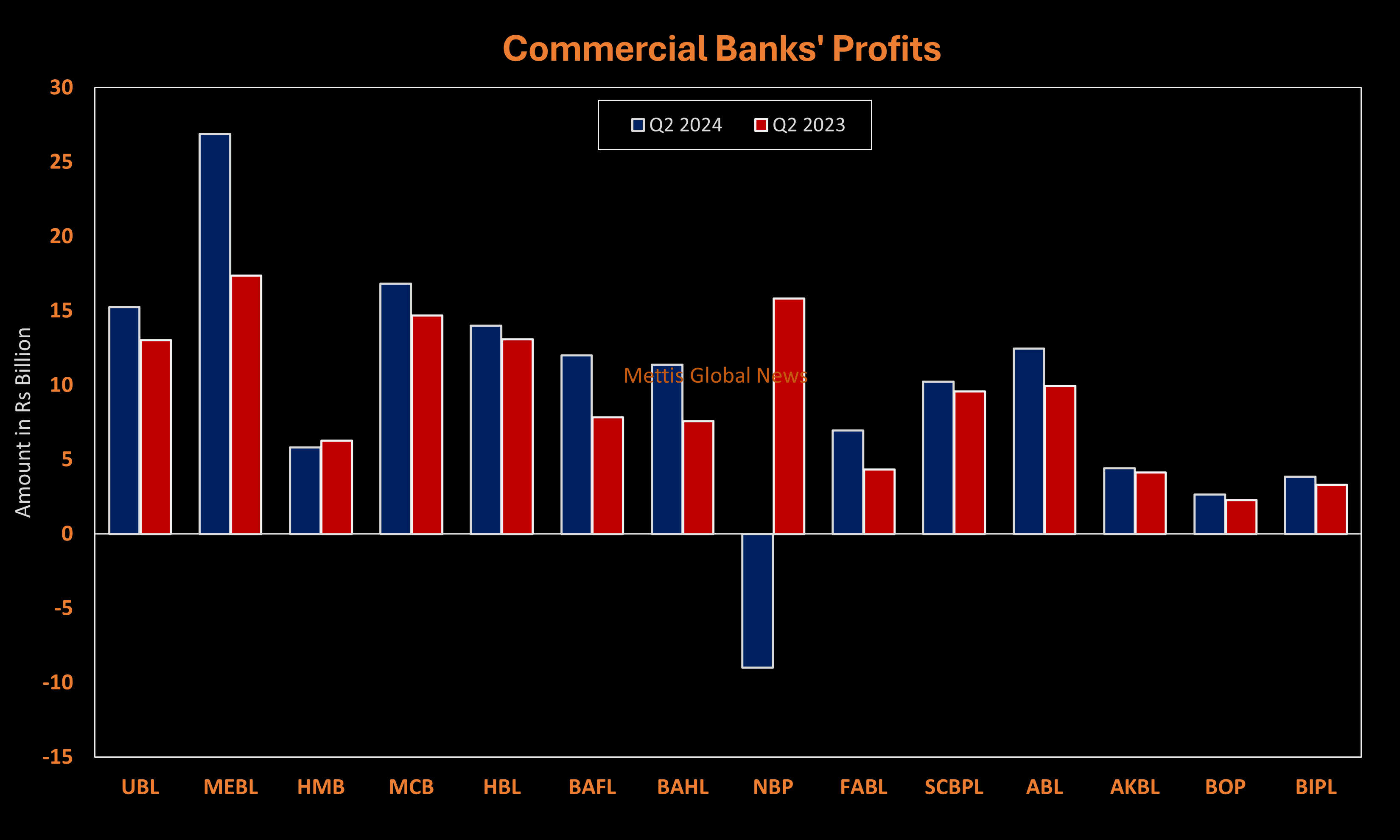

The KSE-100 listed Banking sector, which comprises of 14 members, recorded a consolidated profit of Rs133.81billion, which is 3.41% year-on-year (YoY) higher compared to the bottom line of Rs129.4bn posted in the same quarter last year.

Meezan Bank Limited (MEBL), emerged as the lead contributor to the sector’s earnings, arriving at a remarkable second-quarter profit of Rs26.89bn, up by around 55% YoY.

The sector's most profitable bank also maintained its position as the most valuable one in Pakistan as its market capitalization reached Rs429bn ($1.54bn) on June 30, 2024.

MCB Bank (MCB) and United Bank (UBL) followed the lead and secured second and third place in the profit race, earning Rs16.84bn and Rs15.27bn, respectively in Q2 2024.

In the previous quarter, , the top three positions were held by the same banks, reflecting their consistent and sound performance as market leaders.

In terms of growth, Faysal Bank (FABL), MEBL, and Bank Alfalah (BAFL) secured the top three slots. Conversely, Habib Metro (HMB) and National Bank (NBP) reported a decline in their consolidated earnings.

Specifically, NBP, the sole government-owned bank incurred a loss of nearly Rs9bn on account of settlement of pension liability, which resulted in a one-time outflow of Rs49.01bn in Q2 2024.

To recall, NBP was the only bank that surpassed the Rs1 trillion mark in markup income in a single year, leading it to book a profit of Rs51.84bn in 2023.

For a more accurate examination, if the bank’s single-time loss is excluded from this review, the sector’s bottom line spiked 25.79% YoY in Q2 2024.

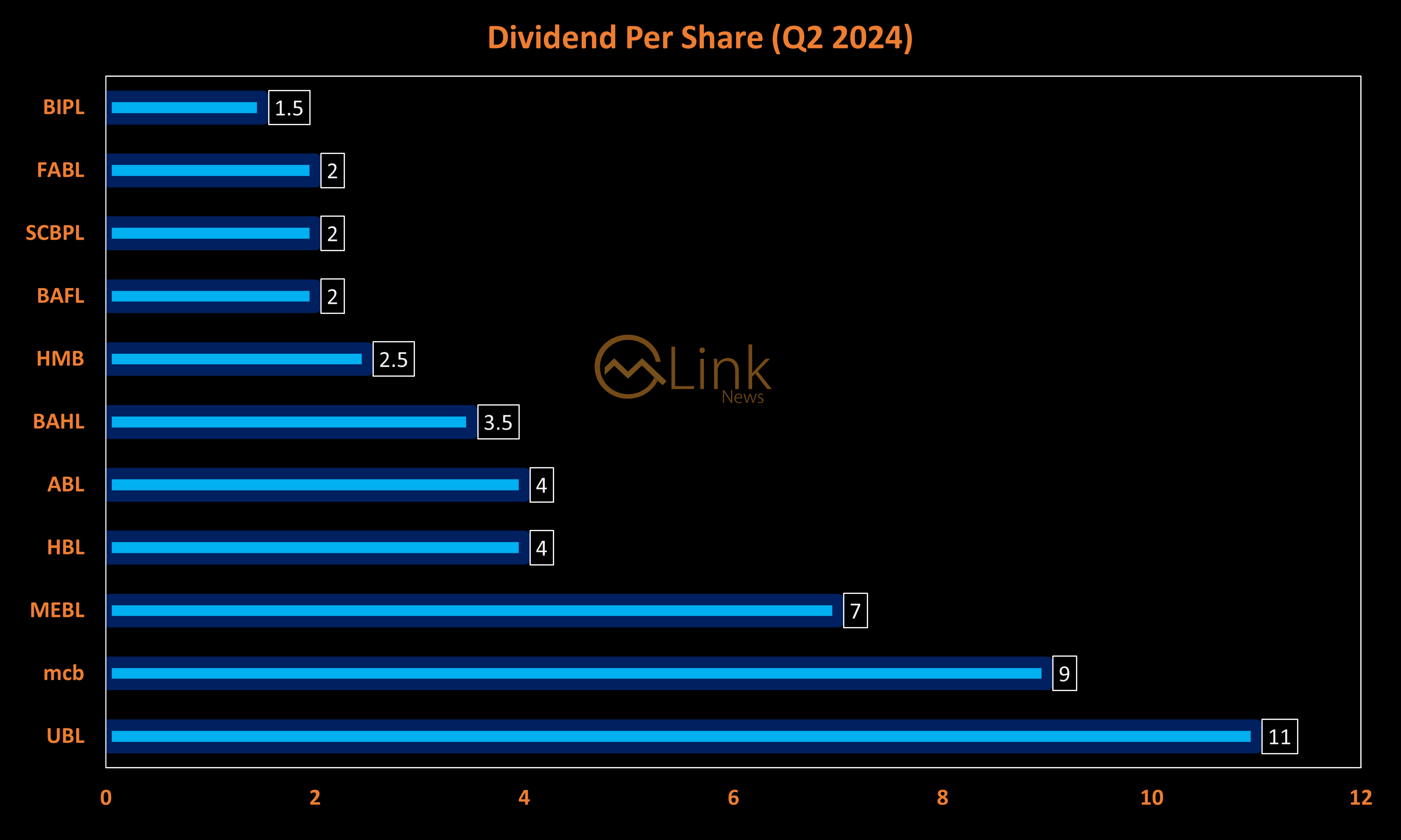

With respect to returns in the form of dividends to shareholders, UBL once again took the lead by declaring the highest dividend of Rs11 per share.

MCB and MEBL were the next in line, announcing dividends of Rs9 and Rs7 per share, respectively, in the second quarter of 2024.

Meanwhile, Askari Bank, Bank Islami, NBP, and Bank of Punjab did not pay dividends this quarter.

The huge profit rally observed during the review period spreads from the past year (2023), in which the majority of the banks recorded their highest-ever profits and dividend payouts.

The combined consolidated profit and loss account of the 14 - banks displays a net interest income of Rs431.58bn, rising by 6.55% compared to Rs405.06bn.

Even though the interest earnings moved up, growth remained capped and lower compared to the previous quarter, as the country embraced its first monetary easing in almost four years.

On June 10, 2024, the State Bank of Pakistan (SBP) surprised market participants by slashing the key policy rate by 150 basis points to 20.5%, a bigger margin than what was expected by market analysts.

Later on in July, the interest rate was slashed by another 100bps to 19.5%, in line with the market expectations.

As a result, nearly half of the KSE100 banking sector reported a year-on-year decline in net interest income. This includes UBL, HMB, MCB, BAFL, ABL, AKBL, and BOP.

Nonetheless, the remarkable growth achieved by other players, particularly MEBL and BAHL, propelled the sector’s net interest income to a higher level in Q2 2024.

Positive volumetric growth in average earning assets, supported by improving spreads and effective duration management of investments enabled higher markup income.

Further assessment of the profit and loss account indicates that the success achieved this quarter is largely attributed to non-markup income rather than markup income.

The sector’s total non-interest income boomed 44.64% to Rs122.62bn versus Rs84.78bn in Q2 CY23 as nearly all sub-components took the upward ride.

Fee-based revenues maintained the overall business momentum with an 18.35% increase over the same period last year resulting from growth across branches, improved customer and interbank flows and commission income from remittances and trade.

The "Gain on Securities" category provided the most favorable position for the sector, reaching Rs15.9bn in Q2 CY24 compared to just Rs957.53m in the same quarter last year. This increase was driven by higher gains on federal government securities and Euro bonds.

Additionally, foreign exchange income and returns from associates and joint ventures surged by 48.98% and 19.38% YoY, respectively, during the review period.

The total income of the sector clocked in at Rs554.2bn, up by 13.14% from Rs489.83m in Q2 CY23.

Now, if we focus on the banks' expenses, it becomes clearer how the growth in income narrowed as it moved toward the bottom line.

These assessed 14 banks registered non-markup expenses of Rs243.67bn, which is approximately 20% higher on a year-on-year basis, in line with high inflation levels.

As per certain banks, a high inflationary environment, continued investments in human resources, technological upgradation, fees and subscriptions, administrative expenses, and repair and maintenance were the causes of this substantial expense burden.

(Cost to income stood at a whopping 43.97% in Q2 CY24 vs 41.6% in Q2 CY23)

Another interesting element that attracts attention is the provision section of the income statement which reports a net provision reversal of Rs2.14bn versus a massive provision expense of Rs15.23bn in the corresponding period.

This means that improved economic conditions, combined with better credit quality and recoveries, led to a reduction in provisions for potential loan losses.

On the taxation front, commercial banks barred a cumulative tax burden of Rs129.84bn in Q2 2024, which is 8.19% YoY lower compared to the Rs141.43bn paid in the same quarter last year.

(Effective tax rate clocks in at 49.25, down from the 52.22% in Q2 CY23)

| Consolidated Profit and loss account for the quarter ended June 30, 2024 (Rupees in ‘000) | |||

|---|---|---|---|

| June-24 | June-23 | % Change | |

| Mark-up/return/interest earned | 1,747,440,599 | 1,292,957,213 | 35.15% |

| Mark-up/return/interest expensed | 1,315,860,972 | 887,902,056 | 48.20% |

| Net mark-up/interest income | 431,579,627 | 405,055,157 | 6.55% |

| Fee and commission income | 62,322,347 | 52,661,322 | 18.35% |

| Dividend income | 5,567,036 | 5,506,337 | 1.10% |

| Foreign exchange income | 26,820,235 | 18,002,993 | 48.98% |

| Income /Loss from derivatives | 1,158,001 | 2,449,623 | -52.73% |

| Gain on sale of securities - net | 15,900,913 | 957,530 | 1560.62% |

| Share of profit of associates | 3,391,679 | 2,841,151 | 19.38% |

| Other income | 7,464,057 | 2,360,355 | 216.23% |

| Total non mark-up /interest income | 122,624,268 | 84,779,311 | 44.64% |

| Total income | 554,203,895 | 489,834,468 | 13.14% |

| Non mark-up/interest expenses | |||

| Operating expenses | 237,590,041 | 198,057,555 | 19.96% |

| Workers Welfare fund | 5,780,626 | 4,987,992 | 15.89% |

| Other charges | 301,351 | 731,524 | -58.81% |

| Total non mark-up/interest expenses | 243,672,018 | 203,777,071 | 19.58% |

| Profit before provisions | 310,531,877 | 286,057,397 | 8.56% |

| Provisions/(reversals) and write offs-net | 2,141,239 | (15,226,142) | - |

| Extraordinary / unusual items | (49,014,365) | - | - |

| Profit before taxation | 263,658,751 | 270,831,255 | -2.65% |

| Taxation | 129,844,339 | 141,432,016 | -8.19% |

| Profit after taxation | 133,814,412 | 129,399,239 | 3.41% |

Key Banking Stats as of Q2 2024

The general public remained eager to deposit their money in banks which led the total deposits held by scheduled banks to surge 22.01% to Rs31.12 trillion as of June 2024 compared to Rs25.51tr in June 2023.

On the other hand, due to the harsh effects of monetary tightening yet to materialize, the growth in advances remained stalled at 1.91% YoY in Q2 CY24. Another factor restricting advances is the banks' preference for investing in government securities rather than engaging in riskier lending to the population.

Advances to Deposit Ratio (ADR) stood at 40% as of June 2024, showing a decrease of 788bps on a yearly basis.

However, the commercial banks set out and made robust investments reaching Rs30.17tr as of June 2024, compared to Rs20.9tr from a year ago, showing a YoY increase of 44.39%.

Accordingly, the Investment to Deposit Ratio (IDR) moved up by 1,503bps to 96.95% in June 2024.

the banking sector spread has decreased by 37bps as compared to a spread of 7.62% in June 2023.

On the other hand, an inverse trend was noted in the banking sector spread, as it dropped by 37bps to 7.26% in June compared to 7.62% in the same month last year.

Future Outlook

The central bank has already initiated monetary easing, having cut the interest rate by 250 basis points over the past two MPC meetings.

With Pakistan's inflation dropping to a single-digit figure in August for the first time since October 2021, markets anticipate more substantial rate cuts.

As the main revenue stream of the scheduled banks is linked to the policy rate, a wider drop in this rate could further lead to constrained growth in markup income, as was experienced this quarter.

On the other side, the population, that was eager to earn higher returns on their deposits, may be inclined to shift towards borrowing and investing as interest rates come down. Hence, volume-based growth might be achieved in markup earnings.

Additionally, the anticipated reductions in the policy rate will stimulate economic activity, which in turn would boost banking operations.

Consequently, the banks could potentially record significantly higher fee and commission incomes, while customer and interbank flows are also expected to expand.

Since interest rate cuts hint at a mixed impact on the sector, the main outcome will depend on each bank's efficiency in driving higher income and managing expenses.

Despite the economic improvements seen in the second quarter of 2024, significant challenges remain - higher interest payments, sustainable external financing, and implementation of IMF's program conditions, according to MCB.

HBL also emphasized that the country's structural weaknesses including a narrow tax base, limited private investment, and distortions in the energy chain are yet to be resolved.

BAFL highlighted key areas for focus: supporting the consumer sector, facilitating SME growth, and leveraging technological advancements to meet evolving customer needs.

Enhancing trade volumes, increasing cash management penetration, and strengthening supply chain financing and home remittance capabilities are integral for the sector to adapt to industry and global developments.

Copyright Mettis Link News

Related News

.png?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,776.60 345.77M | 0.98% 1761.66 |

| ALLSHR | 109,308.50 789.13M | 0.86% 936.37 |

| KSE30 | 54,391.82 176.06M | 1.06% 570.01 |

| KMI30 | 256,134.77 127.57M | 1.02% 2587.38 |

| KMIALLSHR | 70,024.34 435.42M | 0.77% 532.38 |

| BKTi | 52,367.72 86.35M | 1.01% 524.10 |

| OGTi | 35,302.82 9.03M | 1.44% 500.16 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,430.00 | 64,590.00 64,415.00 | -190.00 -0.29% |

| BRENT CRUDE | 83.08 | 83.77 78.92 | 3.63 4.57% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 2.20 2.08% |

| ROTTERDAM COAL MONTHLY | 116.25 | 116.50 116.25 | 0.20 0.17% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.08 | 78.21 77.80 | 0.79 1.02% |

| SUGAR #11 WORLD | 15.58 | 15.60 14.98 | 0.43 2.84% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|