Pakistan govt tackles debt head-on, retires trillions

By Rafay Malik | November 05, 2024 at 12:46 PM GMT+05:00

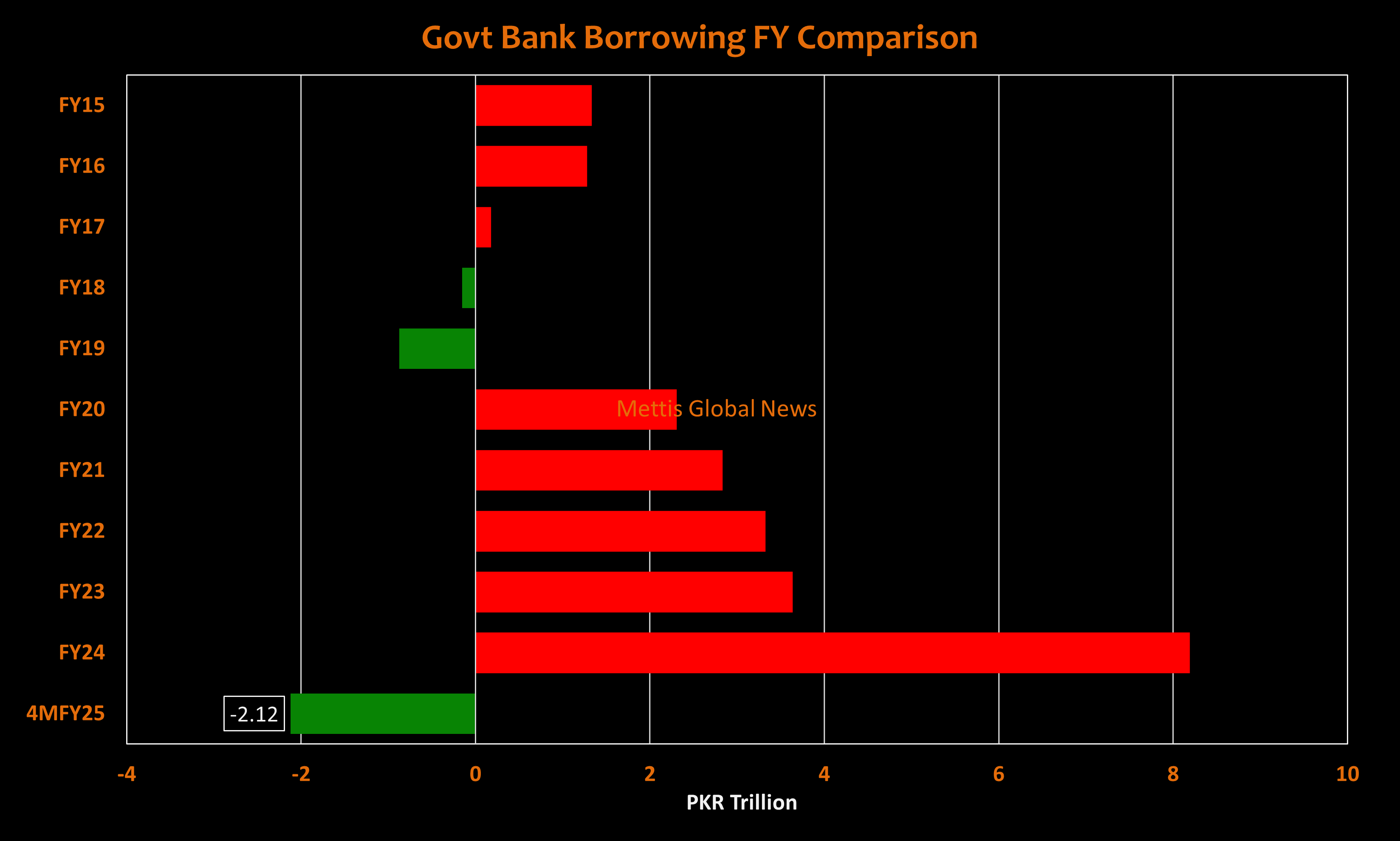

November 04, 2024 (MLN): Pakistan’s government has retired a substantial Rs2.08 trillion in debt in the ongoing fiscal year, marking a shift from the previous fiscal year’s record Rs7.54tr borrowed primarily for budgetary support.

The central bank’s data on monetary aggregates unveiled that the federal government paid off scheduled banks Rs2.04tr as of October 25, 2024. In total, a sum of Rs2.12tr was settled in collaboration with provincial governments.

Interestingly, but perhaps more surprisingly, this reflects a change of strategy from past years when the government heavily relied on commercial banks to bridge its budget deficit.

In FY24, the country’s fiscal strain widened to alarming levels as the government took the highest debt ever taken from commercial banks in a year, which surpassed the combined figure of the last two fiscal years.

The adverse situation has persisted in the country for quite a prolonged period with FY19 marking the last fiscal year in which the government was a net debt payer.

Since then, heavy expenditures associated with surging markup payments have led to a consistent increase in dependency on banks.

Well, thanks to the bumper surplus Profit of the State Bank of Pakistan (SBP) worth Rs2.5tr for the first quarter of fiscal year 2024-25, the cash-starved government finally got the momentum to pay off the long-standing debt of commercial banks.

Due to the high interest rates, SBP saw a significant boost in interest income. Additionally, with improving forex conditions, exchange income surged, tripling SBP’s bottom line to Rs3.4 trillion.

Accordingly, the country managed to record its first budget surplus in over two decades during the first quarter of fiscal year 2024-25, eliminating the need to borrow at high markups—one of the country’s major expenditures.

Furthermore, in these four months of the ongoing fiscal year, the government has also paid off Rs206.45bn of its debt from commodity operations—advances related to the procurement of commodities such as cotton, rice, and wheat.

Apart from these measures, the government's reprofiling of debt by financing its fiscal deficit through the issuance of long-term government securities has drawn significant attention.

On September 18, 2024, the government surprised markets by unexpectedly rejecting all the bids for its Market Treasury Bills (MTBs).

This indicated that the government is now trying to retain its control by setting the rate at which it will borrow, rather than accepting the rate at which funds are offered.

With excess liquidity in the market and hopes of yields falling at a faster pace, participants have remained eager to park their bids to purchase government bonds, as seen in the last MTB auction, where participation was at its peak.

Additionally, the government has also started the buyback of T-bills—a debt management tool used globally in government securities markets to manage refinancing and liquidity risks.

As of now, the central has auctioned three buybacks, purchasing back bonds worth Rs1.026tr.

These buybacks enabled the Government to retire its outstanding debt before its maturity date, allowing it to potentially benefit from lower interest expenses in the long run.

Moreover, these debt overhaul measures mark a significant yet incomplete milestone for the country, as the central government's debt crossed the Rs70tr mark as of August.

Hence, more stringent and decisive actions are required to reach a permanent solution for escaping the debt trap.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 130,686.66 280.01M |

0.26% 342.63 |

| ALLSHR | 81,305.25 897.01M |

0.35% 281.26 |

| KSE30 | 39,945.45 114.02M |

0.09% 37.19 |

| KMI30 | 190,698.05 148.61M |

0.61% 1163.05 |

| KMIALLSHR | 55,074.15 495.43M |

0.53% 290.50 |

| BKTi | 34,568.40 28.73M |

-1.07% -372.33 |

| OGTi | 28,739.35 22.59M |

1.57% 443.29 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 110,145.00 | 110,525.00 110,055.00 |

-270.00 -0.24% |

| BRENT CRUDE | 68.64 | 68.89 68.63 |

-0.16 -0.23% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

-0.75 -0.76% |

| ROTTERDAM COAL MONTHLY | 108.45 | 109.80 108.45 |

-0.55 -0.50% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.92 | 67.18 66.92 |

-0.08 -0.12% |

| SUGAR #11 WORLD | 16.37 | 16.40 15.44 |

0.79 5.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|