Pakistan banks race for higher ADR to escape tax hammer

.jpg?width=950&height=450&format=Webp)

Rafay Malik | October 09, 2024 at 12:59 PM GMT+05:00

October 09, 2024 (MLN): A sudden rush has emerged among certain Pakistani banks to lend at lower-than-expected rates in order to bring their Advances to Deposit Ratio (ADR) to the desired 50% threshold.

The main agenda of these banks is to avoid an additional tax—initially imposed in 2022 and later extended for 2023—on lower ADR, which the government wants to raise to benefit the private sector.

According to media reports, certain banks have lowered their lending rates to single digits, specifically as low as 3-4%, to scale their advances up and enter the safe zone.

With the benchmark 6-month Karachi Interbank Offer Rates (KIBOR) standing at 14.7%, this reflects a lending rate over 1,000 basis points lower, indicating a strong eagerness to lend.

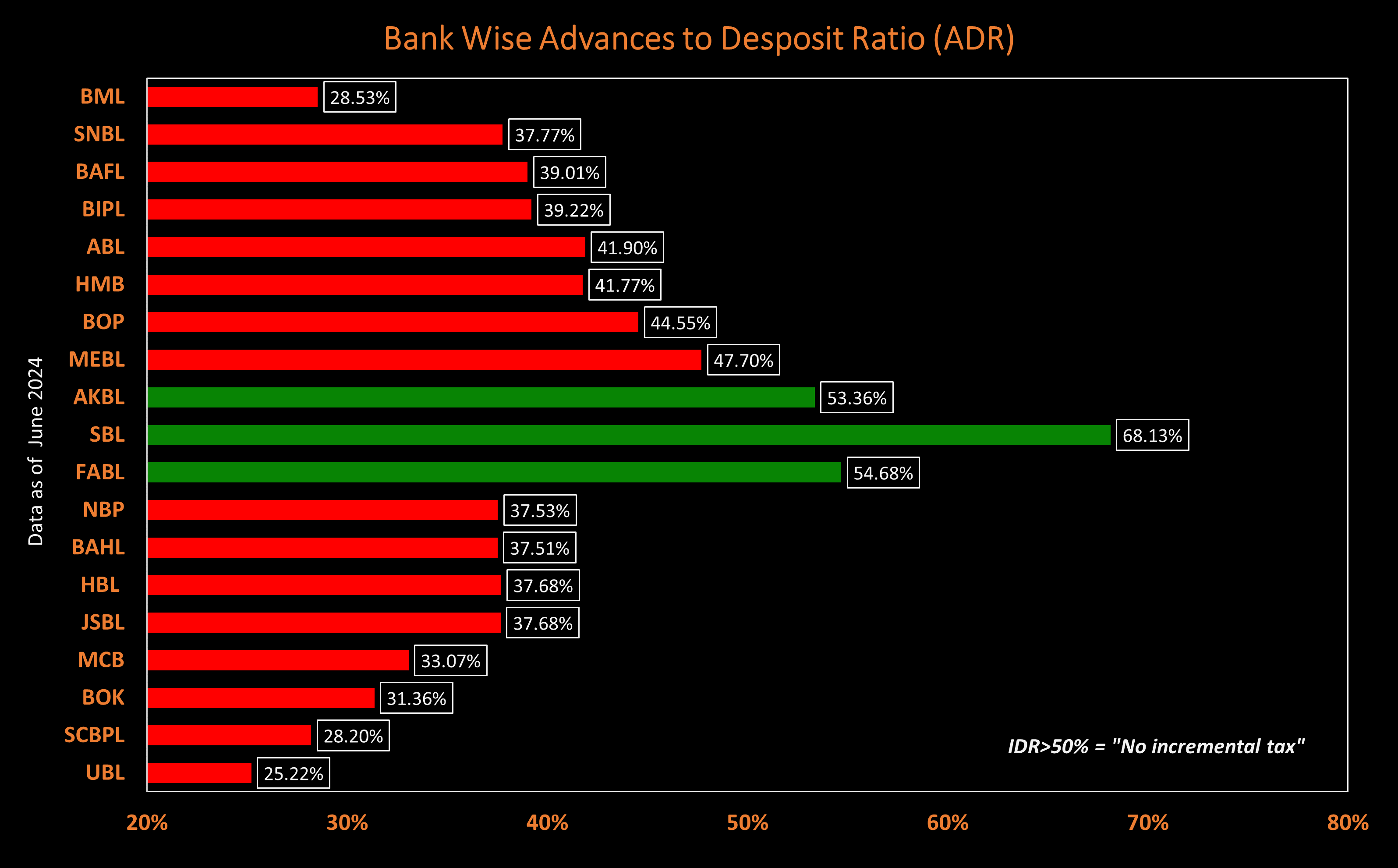

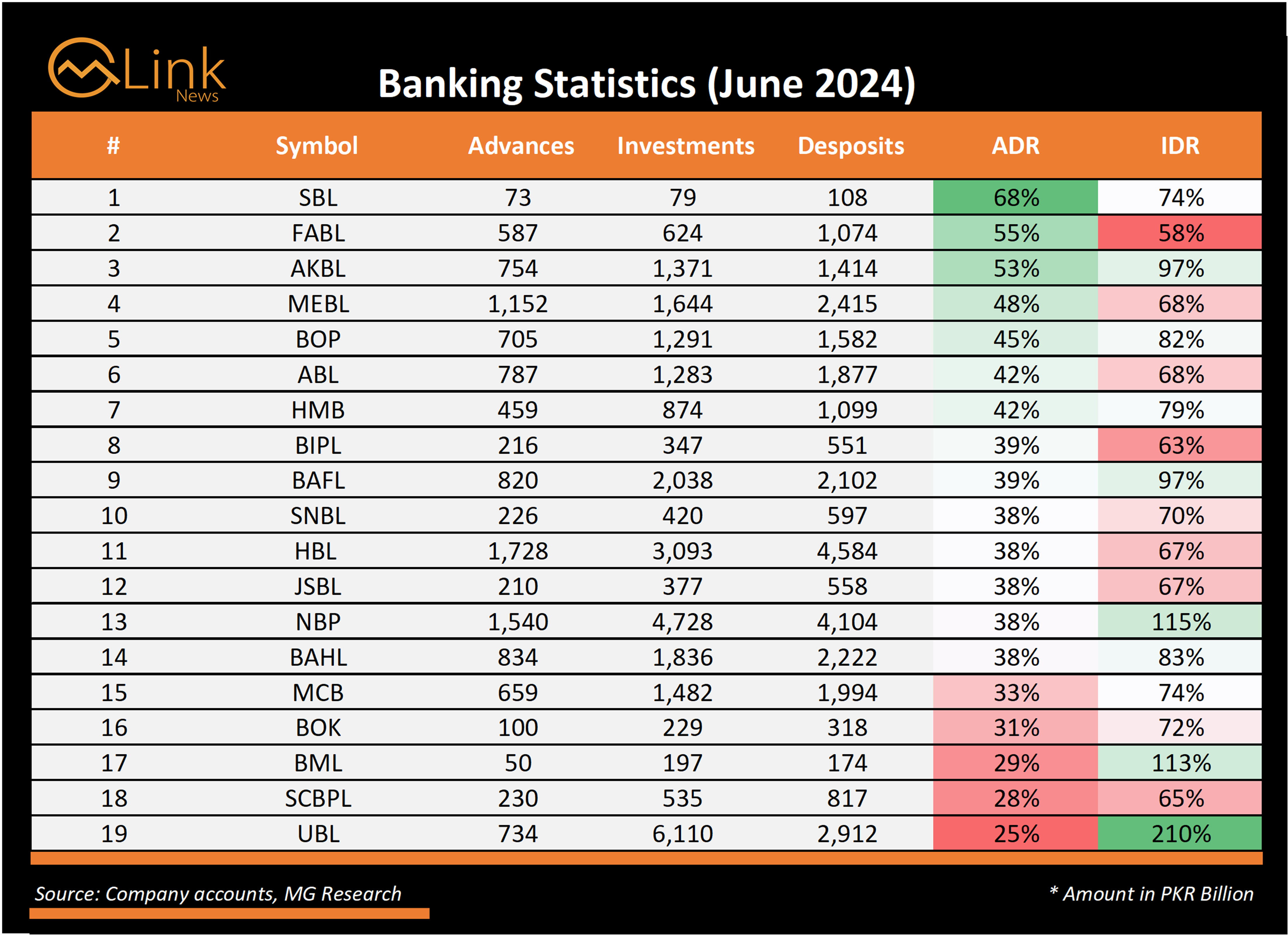

As of June 2024, the average ADR of the banking sector stood at 40.26%, with only three out of the nineteen members appearing to be safe from the additional tax.

Namely, these banks are FABL, SBL, and AKBL with strong ratios of 54.68%, 68.13%, and 53.36%, respectively.

Following closely with an ADR above 40% but below the 50% benchmark, are MEBL, BOP, HMB, and ABL, which may face an incremental tax of 10%.

Meanwhile, the remaining 12 banks, below the 40% threshold are set to face 16% extra tax. Specifically, UBL, SCBPL, BML, BOK and MCB are on the red alert with the lowest ADR of 25.22%, 28.2%, 28.53%, 31.36% and 33.07%, respectively.

This raises a quite frequently asked question: Why do certain banks have extremely low ADR?

Interestingly, the answer to this can easily be found in the sector's robust investment-to-deposit (IDR) figures.

The average IDR as of June 2024 reached a staggering 85.47%, with few of the banks, even exceeding the 100% mark. This means that these banks are investing more than the total amount of their deposits.

Examining the investment portfolio of UBL and NBP, the banks with the highest IDR, it can be drawn out that the majority of these investments are in the government’s safe hands securities such as Market Treasury Bills (MTBs) and Pakistan Investment Bonds (PIBs).

Hence, with these government securities providing an assured and a greater return, these commercial banks prefer not to lend to the private sector, as doing so would result in a high opportunity cost.

Car financing, which is considered the key gauge of assessing private sector loans has already dropped for the 26th consecutive month to Rs227.3bn in August 2024, due to high borrowing costs coupled with the unwillingness of banks to lend.

This was the primary reason why the additional tax was introduced for the sector to force them to lend to the deprived private sector.

With lending at such minimal markup, individuals and corporates might stand up to take loans, which eventually would improve liquidity and thereby the stock market.

Nonetheless, the sector, despite bearing a low return on loans might not be able to meet the ADR requirement as the growth in deposits is also an equivalent hurdle.

The total deposits held by scheduled banks surged by 17.9% from a year ago to Rs30.78 trillion in August 2024 compared to Rs26.11tr in August 2023, with the likelihood of further growing.

The expected increase is driven by the public's growing willingness to save in banks, following the surge in real interest rates to a record 10.6%.

This follows the release of the September inflation data, which revealed the slowest inflation rate (6.9%) in nearly four years.

To meet the threshold, commercial banks would either have to reduce their deposits—an option that appears unlikely—or expand lending at an unusual pace with extremely low interest rates in a shorter period, creating one of the toughest challenges ever faced by the sector.

On the positive side, several banks, during their corporate briefing sessions, expressed confidence that they would achieve this target by December, thereby avoiding the incremental tax.

Additional challenges

Pakistan’s central bank has already initiated the monetary easing with the policy rate down by 450bps since June.

Inflation is down to 6.9%, the lowest reading since January 2021. Last year in May, price gains surged to a record 38%.

Considering this, and the elevated real interest rate, SBP is anticipated to slash rates further by a greater margin.

As the main source of income for banks is interest income, a reduction in interest rates will further result in reduced interest margins, which was already seen in Q2 CY24.

Furthermore, the significant investments of these banks in government securities may be affected as the government has initiated debt reprofiling.

On September 18, 2024, the government surprised markets by unexpectedly rejecting all the bids for its Market Treasury Bills (MTBs).

This indicated that the government is now trying to retain its control by setting the rate at which it will borrow, rather than accepting the rate at which funds are offered.

With excess liquidity in the market and hopes of yields falling at a faster pace, participants would remain eager to park their bids to purchase government bonds.

Additionally, the government has also started the buyback of T-bills, with the inaugural auction witnessing the repurchase of T-bills worth Rs351bn.

With another round of buy-back auction scheduled for today and participants showing eagerness to invest, government bonds are expected to yield lower returns, which could impact the sector's major source of income.

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 175,285.78 248.39M | 1.02% 1766.97 |

| ALLSHR | 106,536.82 578.97M | 1.02% 1073.42 |

| KSE30 | 52,320.98 90.24M | 1.18% 611.36 |

| KMI30 | 246,775.63 72.73M | 0.99% 2407.71 |

| KMIALLSHR | 68,372.65 345.21M | 0.84% 569.39 |

| BKTi | 49,718.24 37.75M | 1.43% 700.72 |

| OGTi | 35,126.27 7.30M | 0.44% 154.29 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,720.00 | 65,105.00 64,480.00 | -365.00 -0.56% |

| BRENT CRUDE | 85.28 | 85.55 85.14 | 0.33 0.39% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.25 -1.17% |

| ROTTERDAM COAL MONTHLY | 120.00 | 120.00 120.00 | 0.65 0.54% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 80.13 | 80.59 79.60 | 0.53 0.67% |

| SUGAR #11 WORLD | 14.86 | 14.99 14.71 | -0.02 -0.13% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|