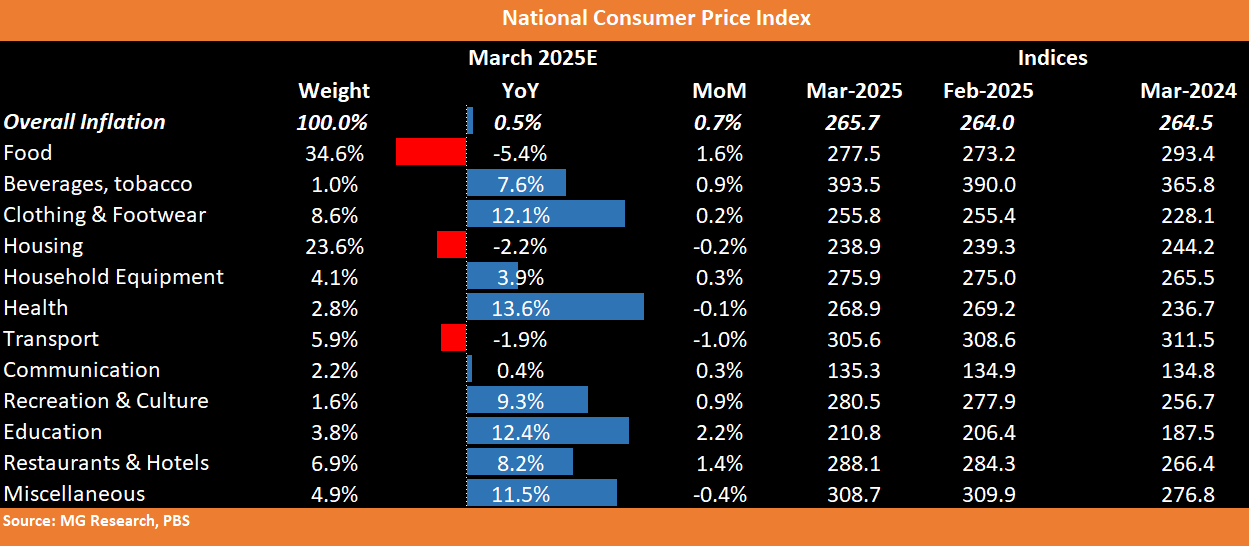

CPI for March likely to clock in at 0.5%

By MG News | April 01, 2025 at 11:25 PM GMT+05:00

April 01, 2025 (MLN): The Consumer Price Index (CPI) for March 2025 is estimated at 0.5% YoY, marking the lowest inflation reading since December 1965, when it stood at 0.57%.

On a MoM basis, inflation is expected to increase by 0.7% compared to the previous month's decline of 0.8%.

This will bring the average inflation for the nine months of FY25 to 5.35%, significantly lower than the 27.21% recorded in the same period of FY24. Last month, the YoY inflation clocked in at 1.5%.

The YoY drop is primarily attributed to the high base effect and a decrease in the food index.

Food Inflation is expected to decline by 5.4% YoY, and while on MoM basis, it would increase by 1.6%, mainly due to Ramadan and the Eid effect.

The monthly increase is likely primarily driven by higher prices of key staples, including chicken (+9.92% MoM), eggs (+6.35% MoM), and tomatoes (+26.32% MoM).

The Housing Index is expected to decline by 0.2% MoM, mainly due to lower electricity costs. This follows a negative fuel cost adjustment (FCA) of Rs2.12 per kWh for January 25, which will be accounted for in March bills.

Transport Segment is expected to see a meagre 1% MoM decrease in prices due to a 0.41% and 2.72% reduction in petrol and diesel prices, respectively. Similarly, on a yearly basis, it is also expected to see a drop of 1.9%.

According to the Economic Update and Outlook by the Finance Division, inflation is expected to stay within the 1%–1.5% range in March 2025 and rise to 2%–3% in April 2025.

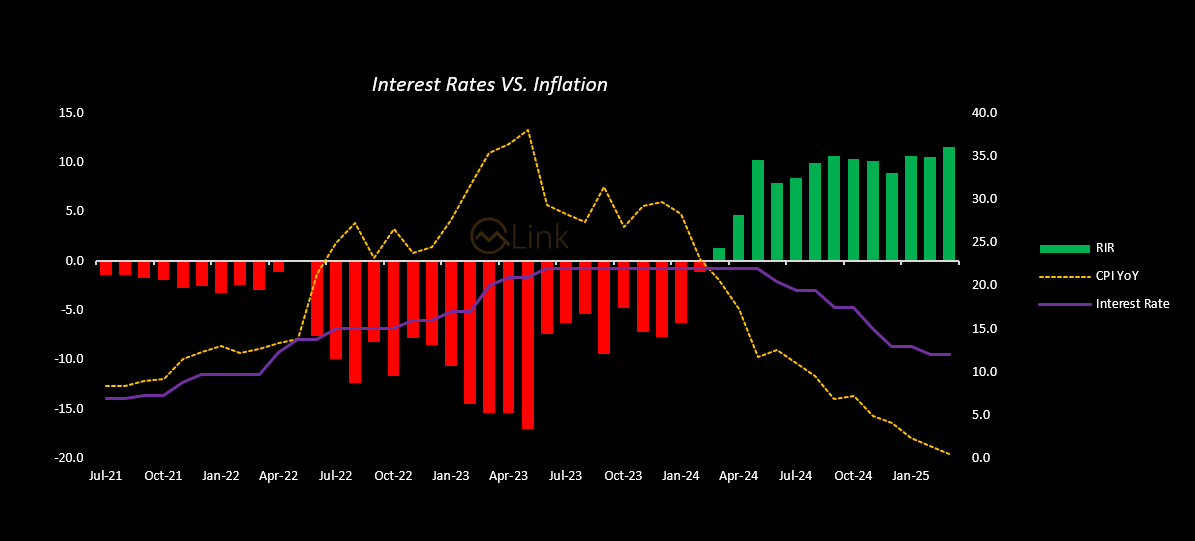

Real Interest Rate:

With inflation expectations at 0.5% for March 2025, real interest rates will be 11.5%.

On the interest rate front, the Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) kept the policy rate unchanged at 12%, effective March 11, 2025, in contrast with market expectations.

The Committee noted that inflation in February 2025 turned out to be lower than expected, mainly due to a drop in food and energy prices. Notwithstanding this decline, the Committee assessed the risks posed by the inherent volatility in these prices to the current declining trend in inflation.

Given these developments, the Committee assessed inflation to come down further before gradually inching up and stabilizing within the 5% - 7% target range.

This inflation outlook, however, is susceptible to risks emanating mainly from volatility in food prices, the timing and magnitude of energy price adjustments, additional revenue measures, protectionist policies in major economies, and the uncertain outlook for global commodity prices.

Copyright Mettis Link News

Related News

.jpeg)

.png)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 132,676.23 85.59M |

-0.54% -726.96 |

| ALLSHR | 82,993.04 474.30M |

-0.23% -195.02 |

| KSE30 | 40,369.48 31.06M |

-0.69% -281.98 |

| KMI30 | 190,862.78 35.26M |

-0.64% -1221.13 |

| KMIALLSHR | 55,707.55 243.10M |

-0.25% -140.15 |

| BKTi | 36,196.50 5.00M |

-0.62% -226.37 |

| OGTi | 28,264.02 6.69M |

-0.61% -173.59 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,050.00 | 109,545.00 108,625.00 |

-165.00 -0.15% |

| BRENT CRUDE | 69.96 | 70.09 69.85 |

-0.19 -0.27% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

2.05 2.15% |

| ROTTERDAM COAL MONTHLY | 106.65 | 106.65 106.25 |

0.50 0.47% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.13 | 68.27 67.78 |

-0.20 -0.29% |

| SUGAR #11 WORLD | 16.15 | 16.37 16.10 |

-0.13 -0.80% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|