Weekly Market Roundup

MG News | April 25, 2026 at 04:57 PM GMT+05:00

April 25, 2026 (MLN): Pakistan’s equity market

reversed course during the week ended April 24, 2026, snapping its two-week

recovery streak as the benchmark KSE-100 Index closed at 170,672.04, down from

173,939.01 recorded on April 17, 2026.

The index shed 3,266.97 points, translating into a 1.88%

week-on-week (WoW) decline.

A constructive resolution of the Middle East conflict

remained a key near-term catalyst for Pakistan’s equity market, shaping overall

investor sentiment during the week.

The Pakistan Stock Exchange (PSX) witnessed heightened

volatility in the final sessions, as investors closely tracked geopolitical

developments, particularly expectations surrounding a potential resumption of

talks between the United States and Iran._20260425115135535_c926cc.jpeg)

Market Capitalization

Total market capitalization declined in line with the index

performance. As of April 24, 2026, market cap stood at Rs4.923 trillion,

compared to Rs5.029tr on April 17, 2026, marked a decrease of Rs106.29bn or

2.11% WoW.

In USD terms, market capitalization fell to $17.65bn from

$18.03bn in the previous week, showing a contraction in overall market value

alongside slight currency pressure._20260425115112363_f28454.jpeg)

Dollar-adjusted returns turned negative, clocking in at

-1.85% WoW compared to +4.07% in the prior week, indicated a decline in both

local and foreign investor returns amid the market correction._20260425115102321_9511a1.jpeg)

On the macroeconomic front, foreign investors repatriated $1.83bn

in profits and dividends from Pakistan during 9MFY26, marking a 6.33% YoY

increase, according to State Bank of Pakistan data.

The Power and Financial sectors led outflows, while the

United Kingdom and China remained the top destinations for profit repatriation.

Banking

spreads widened in March 2026 as deposit returns fell while lending rates edged

up. Real deposit losses narrowed significantly, signaling improved purchasing

power for savers despite still negative returns.

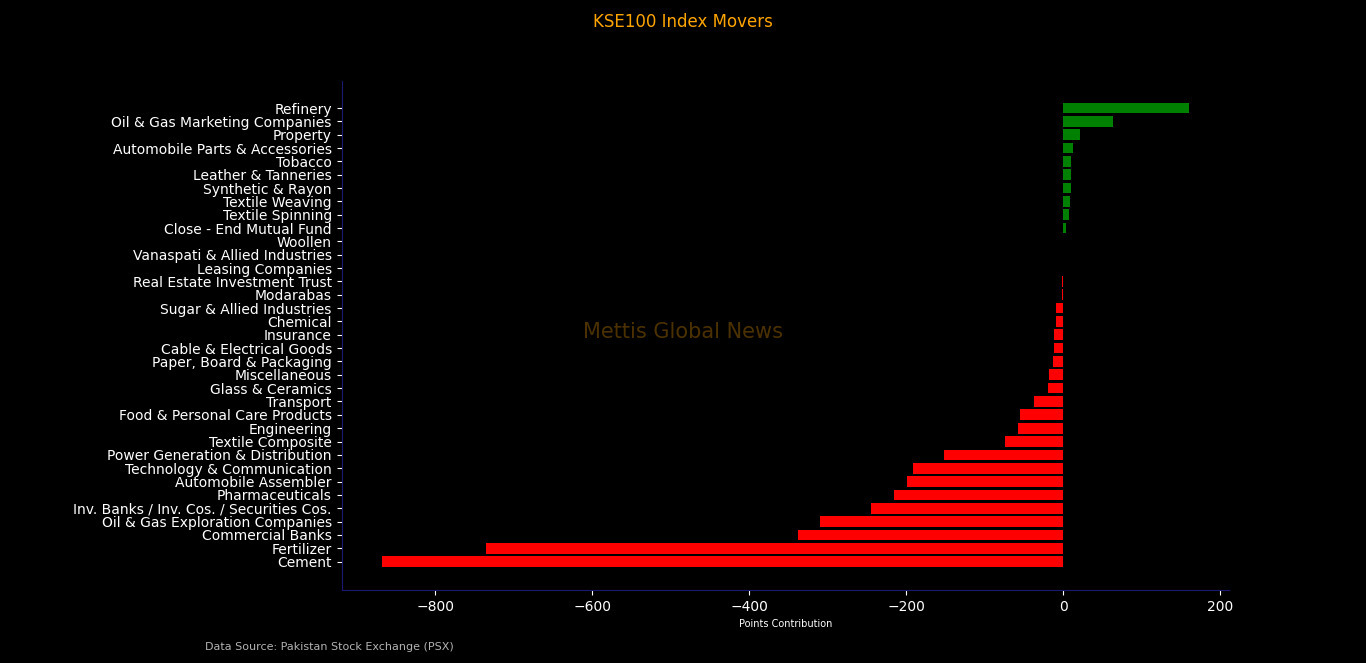

Index Movers

Sector-wise, the decline was broad-based, with major

heavyweights dragging the index lower.

Cement emerged as the largest laggard, shaving off 867.97

points, followed by fertilizer (-735.61 points), reflecting pressure on key

index drivers.

Commercial banks contributed a decline of 337.46 points amid

mild profit-taking, while oil & gas exploration companies (-310.19 points)

and investment banks/securities (-245.25 points) also weighed on the benchmark.

Other notable negative contributors included pharmaceuticals

(-215.63 points), automobile assemblers (-198.41 points), technology &

communication (-191.88 points), and power generation (-152.01 points),

indicating widespread selling across sectors.

On the positive side, select pockets provided limited

support, with refinery (+160.33 points) and oil & gas marketing companies

(+64.08 points) offering some cushioning to the index.

At the individual stock level, UBL led the upside with a

contribution of 528.21 points, followed by ATRL (+144.19 points) and PSO

(+116.33 points).

Other notable gainers included OGDC, PPL, MARI, HUBC,

ENGROH, MCB, HBL, and FFC, highlighting selective strength in energy, banking,

and fertilizer stocks.

Additional support came from EFERT, LUCK, DGKC, MLCF, FCCL,

SYS, TRG, BAFL, and SNGP, indicating participation from both cyclical and

growth segments.

On the downside, major drags included cement-heavy names

such as LUCK, DGKC, FCCL (despite some positive contributions, broader sector

weakness dominated), along with fertilizer stocks like FATIMA and AHCL, and

pressure in pharmaceuticals such as HALEON and ABOT.

Losses were also seen in technology (AIRLINK, PTC) and

insurance (AICL), reinforcing the broad-based nature of the correction._20260425115046758_daa178.jpeg)

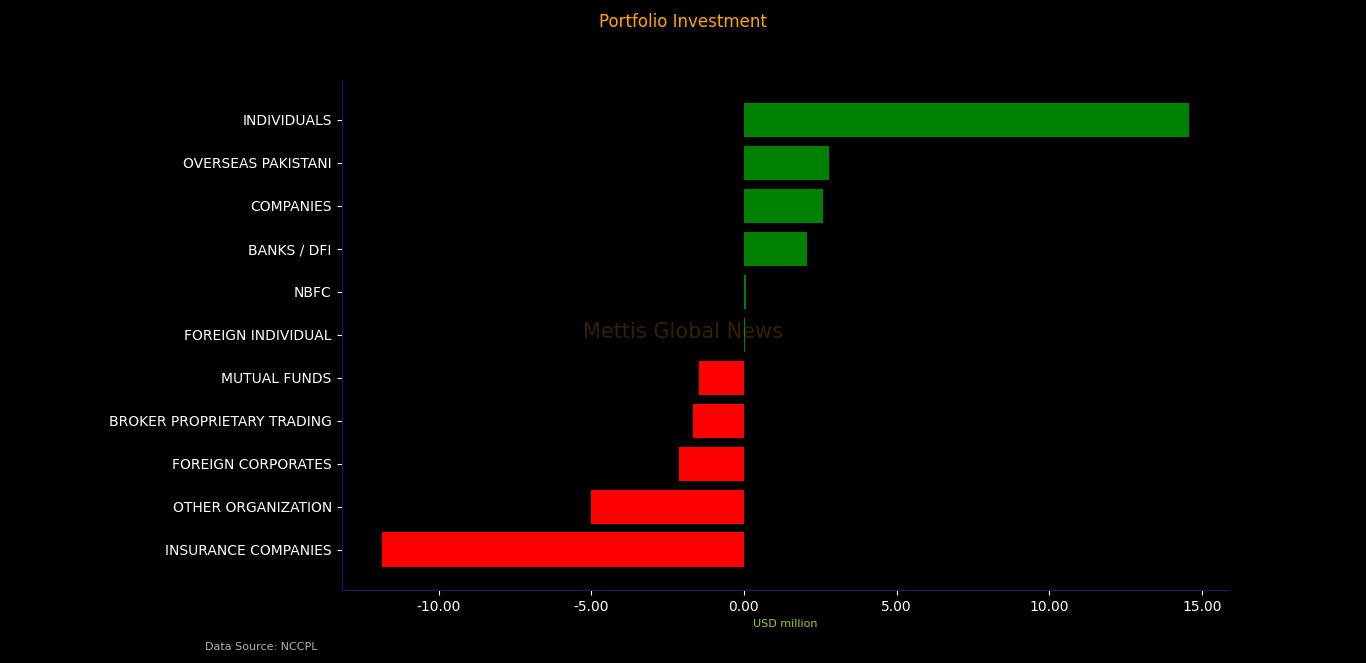

FIPI / LIPI

Foreign investment flows remained mixed during the week.

Under Foreign Institutional Portfolio Investment (FIPI),

overseas Pakistanis provided strong support with a net inflow of Rs781.59m

($2.80m).

However, foreign corporates remained net sellers, recording

an outflow of Rs594.88m ($2.13m), while foreign individuals were marginal

buyers with a net inflow of Rs13.05m.

On the domestic side, Local Portfolio Investment (LIPI)

posted a net outflow of Rs199.76m ($0.72m), indicating slight overall selling

pressure.

Among local participants, individuals emerged as the largest

buyers with net inflows of Rs4.07bn, followed by companies (+Rs721.67m) and

banks & DFIs (+Rs577.74m), supporting market liquidity.

On the flip side, insurance companies led the selling with a

net outflow of Rs3.31bn, while mutual funds (-Rs414.61m) and broker proprietary

trading (-Rs466.79m) also contributed to the selling pressure.

Other organizations recorded an outflow of Rs1.40bn.

In the debt market, insurance companies showed significant

inflows of Rs8.59bn, while banks & DFIs recorded major outflows of

Rs8.21bn, indicating active reallocation between asset classes.

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|