Weekly Market Roundup

_20260227200326243_a8f892.jpeg?width=950&height=450&format=Webp)

MG News | February 28, 2026 at 01:09 AM GMT+05:00

February 28, 2026 (MLN): Pakistan’s equity market

remained under sustained pressure during the outgoing week, as the benchmark KSE-100

Index closed at 168,062.17, down from 173,169.71 recorded on February 20,

2026.

The index shed 5,107.54 points over the week, translating

into a decline of 2.95% week-on-week (WoW), as persistent selling in

heavyweight sectors kept the market firmly in bearish territory.

Investor sentiment remained subdued as the IMF review

approaches, with market participants opting to trim positions amid uncertainty

over potential policy adjustments and fiscal targets.

The upcoming review is seen as a critical milestone for

economic stability, prompting cautious trading activity.

Market Capitalization

Market capitalization moved in tandem with the index. The total listed market cap declined to Rs4.96 trillion on February 27, 2026, compared to Rs5.11tr a week earlier, marked a contraction of approximately Rs152.2bn or 2.98% WoW.

The erosion in value shows broad-based declines across large-cap

sectors.

In dollar terms, total market capitalization fell to $17.73bn

from $18.27bn last week, representing a 2.95% weekly drop in USD valuation.

Dollar-adjusted returns stood at negative 2.92%, compared to

negative 3.56% in the prior week. While the pace of decline moderated slightly

in foreign currency terms, returns remained firmly negative, underscoring

continued pressure on equity prices rather than currency-driven weakness._20260227200307183_49bbb7.jpeg)

On the macroeconomic front, Pakistan’s

broad money supply stands at Rs46.19tr in January 2026, down 0.73% MoM but

up 15.08% YoY, as per data from the State Bank of Pakistan.

The State Bank of Pakistan purchased

$620m from the interbank market in November 2025, taking total FY26

(Jul–Nov) net FX buying to $3.12bn, though inflows moderated compared to last

year.

Pakistan’s weekly SPI inflation fell

0.54% WoW for the week ended Feb 26, 2026, while rising 4.23% YoY,

according to the Pakistan Bureau of Statistics.

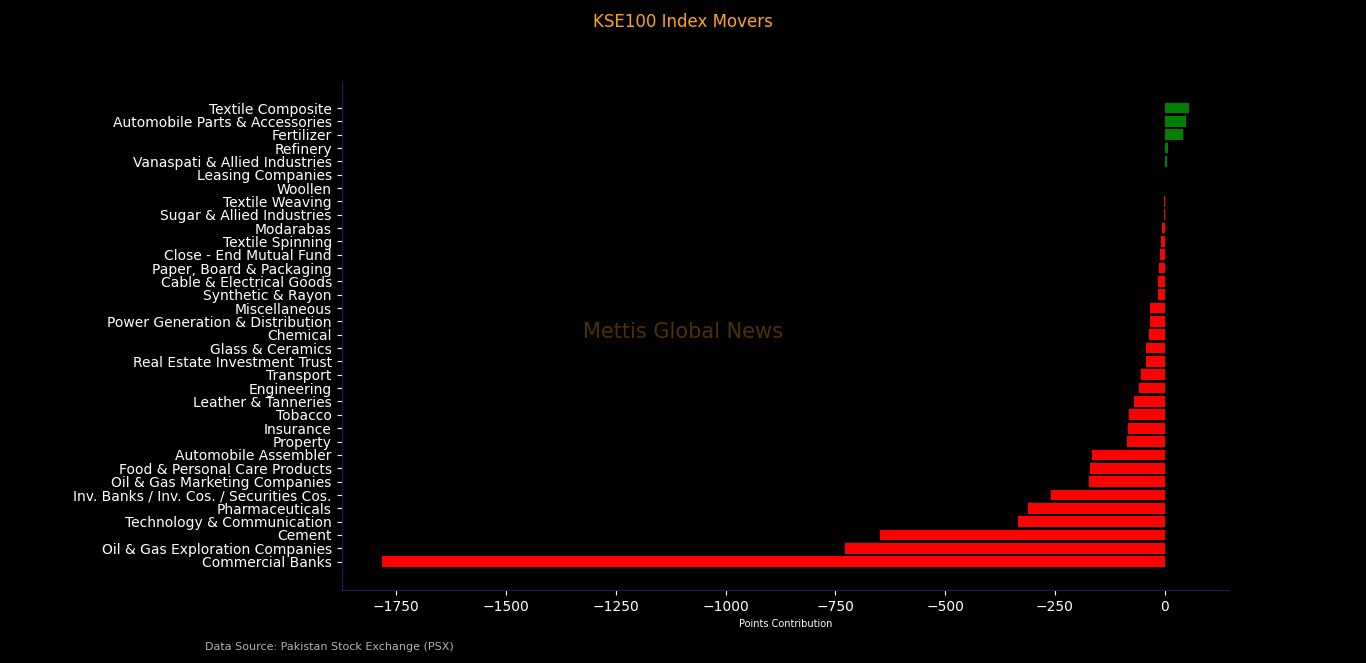

Index Movers

Sector-wise performance confirmed that selling pressure was

systemic. Commercial banks emerged as the largest drag, wiping out 1,782.63

index points amid heavy volumes.

Oil and gas exploration companies followed with a loss of

728.63 points, while cement stocks erased 648.63 points.

Technology and communication shaved off 333.54 points,

pharmaceuticals reduced the index by 310.75 points, and investment banks and

securities companies trimmed 258.78 points.

Oil and gas marketing companies, food and personal care

products, automobile assemblers, power generation firms, engineering,

transport, and several other sectors also contributed negatively, reinforcing

the broad-based nature of the decline.

On the positive side, gains were limited and concentrated in

a few pockets.

Textile composite stocks added 55.36 points, automobile

parts and accessories contributed 48.69 points, fertilizer added 40.70 points,

and refineries and vanaspati producers provided marginal support.

However, these gains were insufficient to offset heavy

losses in banking, exploration, cement, and technology heavyweights.

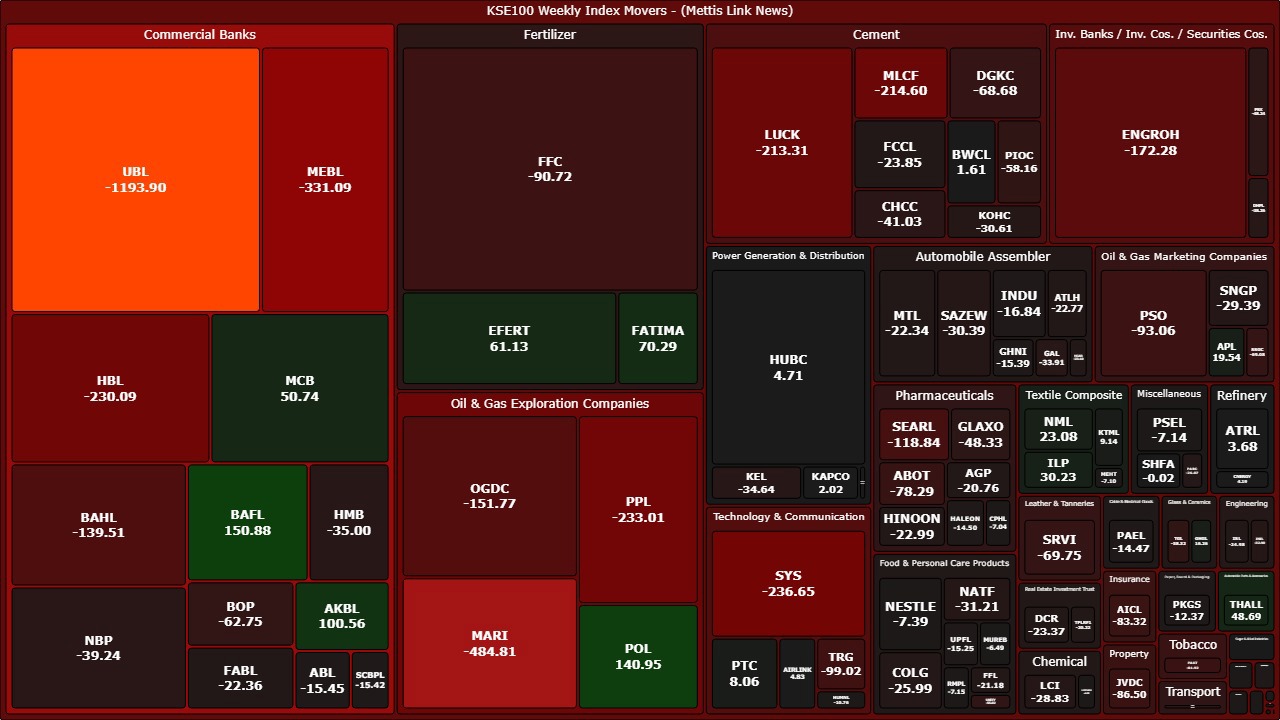

At the company level, a handful of stocks managed to post

positive contributions, including BAFL, POL, AKBL, FATIMA, EFERT, and THALL,

along with select textile composite names.

Nevertheless, losses among major index constituents

dominated overall performance. UBL alone erased 1,193.90 points, while MARI

shed 484.81 points and MEBL lost 331.09 points.

Technology leader SYS declined by 236.65 points, while PPL

and OGDC weighed heavily on the exploration segment.

HBL recorded a 230.09-point decline, and cement majors LUCK

and MLCF also posted substantial losses. The scale of declines in large-cap

stocks indicates institutional-level repositioning rather than retail-driven

volatility.

FIPI/LIPI

Foreign investment flows continued to exert pressure on the

market.

Under Foreign Portfolio Investment (FIPI), foreign investors

remained net sellers with a total outflow of $17.28m during the week.

The bulk of the selling came from foreign corporates, which

offloaded $18.29m worth of equities, while overseas Pakistanis and foreign

individuals provided only marginal buying support.

Local investors absorbed the entire foreign outflow,

resulting in a matching net inflow of $17.28m under Local Portfolio Investment

(LIPI).

Banks and DFIs emerged as the largest buyers with net

purchases of $33.88m, followed by companies and other organizations.

On the selling side, individuals, mutual funds, insurance

companies, and broker proprietary desks recorded net sales.

The flow dynamics suggest that domestic institutional

liquidity provided critical support, preventing a sharper market slide despite

continued foreign exits._20260227200258101_e7385e.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|