Pakistan doubles down on energy reforms

_20260515073249470_9d6753.jpeg?width=950&height=450&format=Webp)

MG News | May 15, 2026 at 12:20 PM GMT+05:00

May 15, 2026 (MLN): Amid one of the most turbulent global commodity cycles in recent memory, Pakistan's energy authorities have doubled down on a commitment that would once have been considered politically untouchable: automatic, fortnightly alignment of domestic fuel prices with international markets.

The pledge, reiterated as oil price volatility rippled

through import-dependent economies, signals that policymakers regard cost

recovery not price suppression as the foundation of a viable energy sector,

according to IMF staff report.

The mechanics of that commitment run deep into the pricing

chain. Ex-refinery petroleum and diesel prices are benchmarked against global

markets, converted to rupees, and supplemented by import freight charges,

marketing margins, dealer commissions, and a federal petroleum development levy

before reaching the pump.

Every fortnight, that calculation resets a discipline the

authorities have committed to maintaining regardless of where international

prices move.

The same logic has been extended into electricity.

Pakistan's power regulator, NEPRA, conducts an annual rebasing exercise

recently shifted from July to January to smooth the tariff path during

low-demand months that determines a uniform weighted average tariff consistent

with full cost recovery.

That base tariff is then layered with quarterly adjustments

for capacity charges, monthly fuel charge adjustments for generation input

costs, a debt service surcharge to finance accumulated power sector

liabilities, and federal taxes.

The most vulnerable consumers those on lifeline connections

are shielded from the quarterly and monthly surcharges, preserving a degree of

protection without dismantling the cost-recovery architecture.

Gas pricing follows its own rhythm. OGRA adjusts tariffs

twice a year, in January and June, setting a progressive schedule that grants

lower rates to protected consumer categories.

Unlike the power sector, there are no intra-year surcharge

mechanisms; instead, any prior-year surpluses are directed back into tariffs to

chip away at the accumulated circular debt stock.

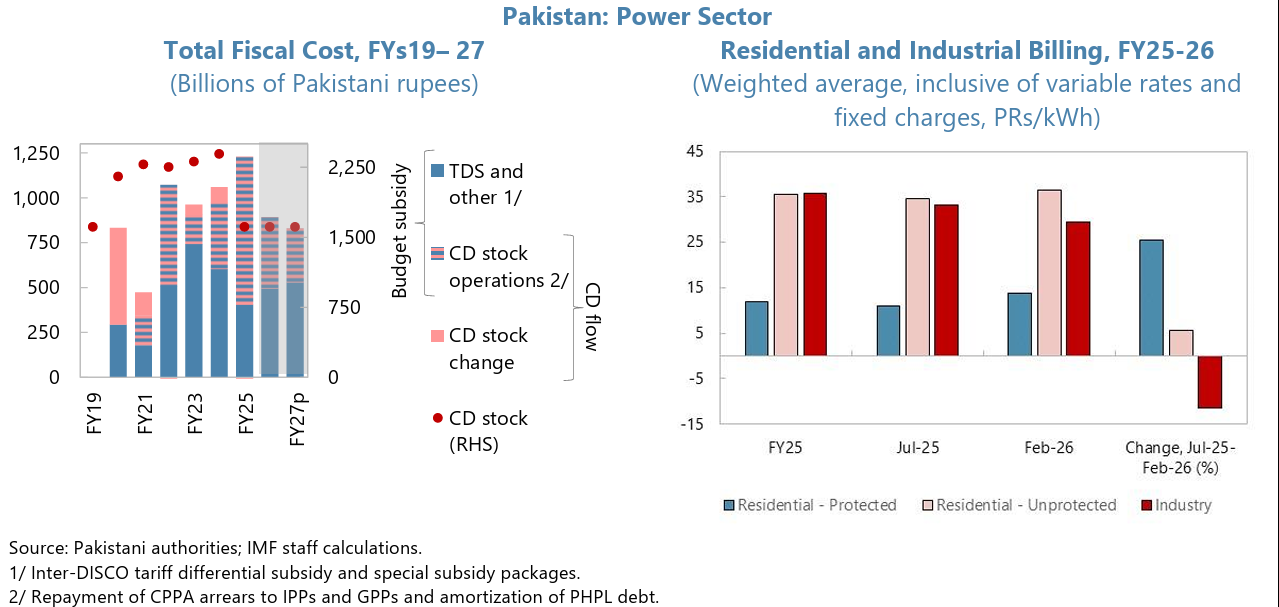

That circular debt remains the sector's most stubborn wound.

For FY27, authorities have set a flow target of Rs300bn Rs100bn lower than the

FY26 ceiling showing genuine operational improvements across the country's

power distribution companies.

The improvement is meaningful enough to allow the planned

power subsidy to ease from 0.7% of GDP to 0.6%. But non-operational pressures

persist.

The delayed settlement of penalty payment arrears with

remaining independent power producers, part of a CD stock reduction plan

spanning FY25 and FY26, continues to lag and demands faster resolution.

On the tariff side, a notable adjustment in February reduced

the cross-subsidy that industrial consumers had been paying toward residential

bills, unwinding a long-standing distortion.

The gap was offset by new or increased fixed charges on

residential consumers, including some in protected categories.

Authorities have been clear that any further restructuring

must preserve the progressive character of the tariff system that lower-income

households must not bear a disproportionate share of the cost-recovery burden.

Structural reform is moving, if unevenly. Private sector

participation in the distribution companies is advancing, though behind its

original schedule.

A second wave of DISCO privatisations has been launched in

parallel, with end-December 2026 designated as a key structural benchmark.

The transmission network has been restructured, and the

first wholesale electricity auctions are expected to begin in mid-2026.

NEPRA has also introduced a shift for solar consumers from a

net metering to a net billing model, better aligned with international

practice.

The transition is sensible in design, but its impact is

blunted by a significant carve-out: existing solar consumers are exempt from

the new framework, locking in what analysts describe as a likely regressive

cross-subsidy from grid ratepayers many of them lower-income to rooftop solar

owners, who tend to be wealthier.

The gas sector faces its own compounding pressures.

Disrupted LNG shipments from the Gulf have forced the authorities into

near-term supply triage, even as a longer-standing structural problem quietly

deepens: long-term import contracts have generated an RLNG surplus against a

backdrop of falling domestic demand.

The recently established National Integrated Energy Plan

secretariat, co-led by the Petroleum and Power Ministries, is intended to bring

coherence to supply and demand planning across fuels a coordination gap that

has long been cited as a source of inefficiency.

In parallel, efforts to reduce unaccounted-for gas continue,

and the publication of an audited, reliable gas circular debt dataset now to be

disseminated quarterly is seen as a prerequisite for any credible plan to

address what has become a large and growing stock of sector liabilities.

Taken together, Pakistan's energy reform story is one of

hard-won progress under persistent pressure.

The architecture of automatic price adjustment, progressive

tariff structures, and regulator-led cost recovery is more robust than it was

several years ago.

But the vulnerabilities circular debt arrears, a regressive

solar exemption, a gas surplus without a resolution plan are reminders that the

reform agenda remains unfinished, and that global price shocks leave little

room for slippage.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,850.00 | 66,020.00 64,290.00 | 230.00 0.36% |

| BRENT CRUDE | 83.50 | 84.44 81.50 | 1.01 1.22% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 105.50 105.50 | -0.25 -0.24% |

| ROTTERDAM COAL MONTHLY | 116.25 | 117.00 116.25 | -0.10 -0.09% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.20 | 78.77 76.53 | 0.91 1.18% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|