Zarea IPO: Should I Stay or Go?

MG News | February 07, 2025 at 08:55 PM GMT+05:00

February 07, 2025 (MLN): For a long time, Pakistan’s public markets haven’t moved in tandem with the structural shifts taking place in the broader economy. It’s quite evident from how the services sector, which accounts for the lion’s share of the country’s gross domestic product, has little representation on the bourse.

As a result, investors are unable to participate in the successes of the biggest growth drivers.

Whether it’s the telecom revolution of the mid 2000s or the tech boom after Covid-19, the public markets and its investors haven’t been able to benefit much. But Zarea plans to change this. After debuting, it will become the first platform-based company on the local bourse.

The company seeks to raise Rs1 billion for 23.81% of the post-IPO shareholding at a floor price of Rs 16 per share, of which 1500% is the premium. Just under half (45%) of these proceeds will be allocated to meeting working capital requirements while the remaining chunk is spread across technology, logistics, marketing, capex and team-building.

To help investors make a more informed decision, Mettis Global dug deep into the prospectus to better understand the offering.

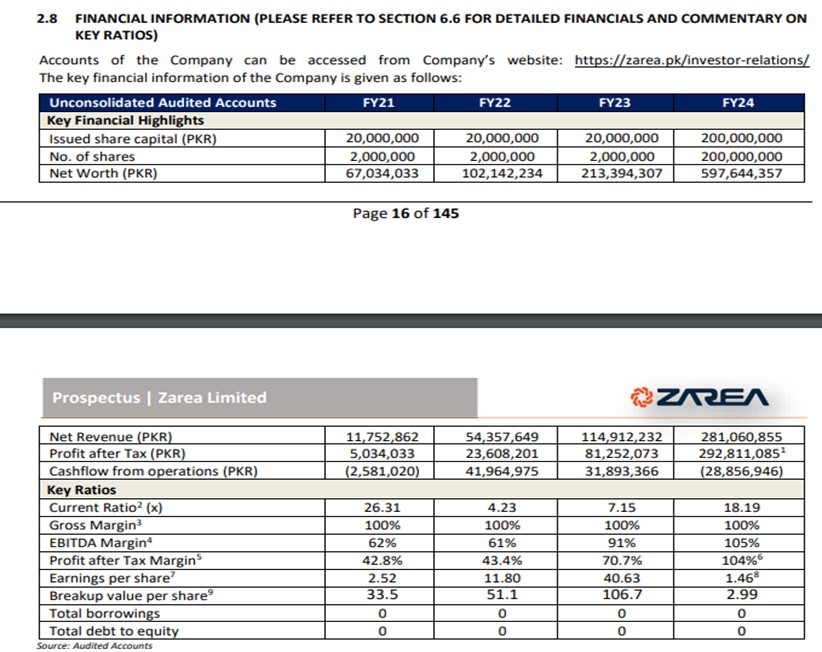

To start with, Zarea has scaled aggressively, with net revenues increasing from just Rs 11.75 million in FY21 to Rs 441.76 million by FY24, translating into a CAGR of 147%. On top of it, the net income was also in the black – a rarity of platform-based companies in the early stages – at Rs 292.8M in the outgoing fiscal year.

For investors seeking exposure to a high-growth play, there seems to be a lot in store. However, the story is not without its risks, not least because of a lack of clarity in the underlying reporting.

Gross margin 100%

Earlier in October, Zarea had filed its draft prospectus which showed a gross margin of 100%. In other words, it had no cost of sales – not even the technology team or infrastructure, in stark contrast to how platform-based companies report data. At the time, Mettis Global had pointed this discrepancy out to the listing officer and received the following explanation from the investment banker, Topline Securities: “The cost of sales applies when entities hold inventory directly; as per its core business model, it does not hold inventory, hence does not bear inventory-related costs.”

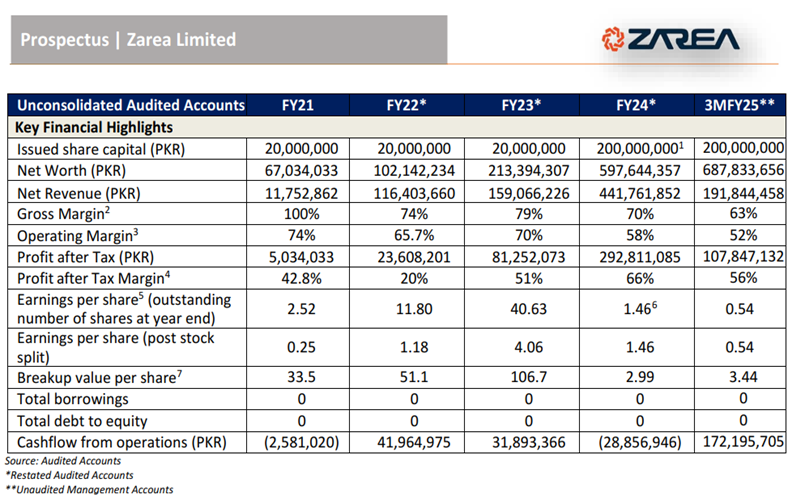

Instead, technology development costs were all capitalized in line with international accounting standards, according to the same response. Despite such matter-of-fact justification, there seems to be a change of heart as the final prospectus now shows gross margins at 63% in 3MFY25.

What exactly happened that the entire accounting approach was revised – not only for the latest year, but all the way back to FY22?

Draft Prospectus

Final Prospectus

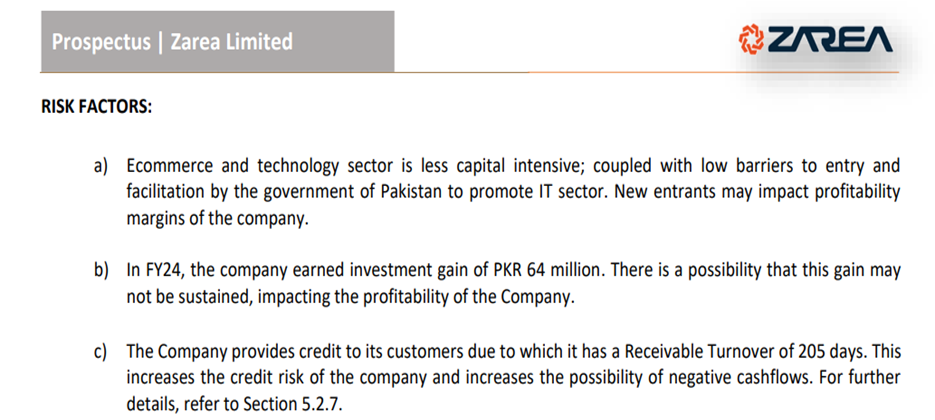

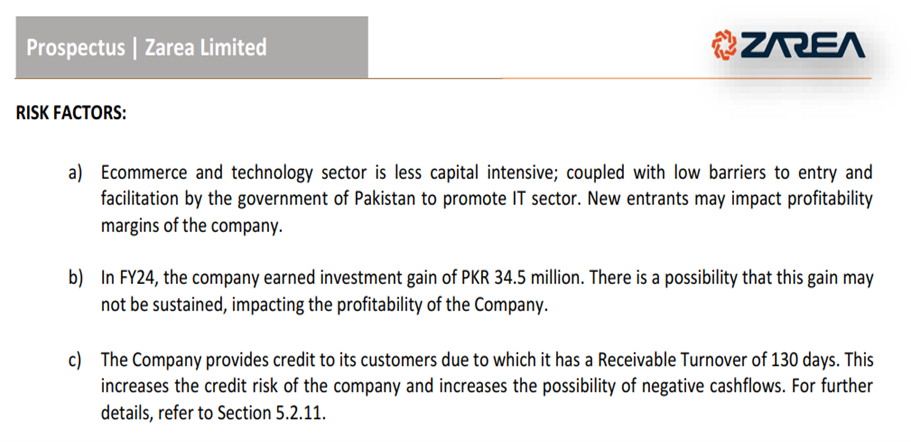

The final prospectus of Zarea Limited presents notable changes from its draft version, particularly in investment gains and receivable turnover. Initially, the company reported an investment gain of Rs64 million in FY24, which was later revised down to Rs34.5 million in the final document.

This significant adjustment raises questions about the basis of the earlier projection and the factors that led to a nearly 46% reduction in reported gains.

Similarly, the receivable turnover period was initially disclosed as 205 days, indicating a longer credit cycle for customers. However, in the final prospectus, this figure was revised to 130 days, suggesting a substantial improvement in the company’s receivables management.

Draft Prospectus

Final Prospectus

The extent of this restatement of audited accounts goes much further, with net revenues revised upwards by Rs160.7 million. All the difference can be attributed to the inclusion of the commodities sale segment, which wasn’t available in the October 2024 filing.

Again, there exists little clarity on what prompted the change or more importantly, why it wasn’t part of the financials in the first place. After all, 45% of the proceeds were meant to develop the credit sales arm, aimed at growing the very same line item.

Broadly, there are two revenue streams: marketplace and sale of commodities. In the former, Zarea acts as a platform connecting demand and supply while charging a certain commission for each transaction while the latter entails the company buying stock and then selling it forward on credit terms. [Note: it does not engage in financing as a business and therefore needs no license.]

The biggest chunk of the revenue comes from cement, bringing Rs 133M in FY24, with agri biomass a distant second contributing Rs81M.

Median Commission

In the prospectus, Zarea didn’t specify what their median commission is from the marketplace. According to the underwriter, the platform usage fee (PUF) varies on the commodity type and market dynamics. It does not apply a uniform rate, as the nature and demand of each commodity requires a tailored approach.

This variable fee structure allows it to remain competitive and flexible, ensuring that Zarea meets the specific needs of each sector it serves.

“While a median commission rate might be estimated, it would not accurately reflect the diverse pricing strategies we employ across commodity categories. This tailored approach helps optimize its platform for a broad range of commodities, supporting sustainable growth and value for its clients.” However, upon asking again, they revealed that Zarea charges a commission between 1% and 10%. Taking the midpoint of the range for simplicity, this would translate into a gross merchandise value of Rs 5.6 billion during FY24. Alternatively, it earns a revenue of Rs 43,300 from each transaction.

The other business segment works rather differently. “Advances in commodities pertain to Zarea’s investment in agricultural biomass commodities during the on-season, which are sold in the off-season, capitalizing on predictable price appreciation driven by supply-demand dynamics. The commodities include bagasse, wheat straw, rice husk, and corn cob, which historically have experienced a price appreciation of 30-70% during the off-season every year. This investment approach has resulted in gains of PKR 29.7 million in 2024, PKR 10.5 million in 2023, and PKR 31.5 million in 2022 for ZL,” notes the prospectus.

Choosing Equity over Debt Financing

To expand this segment, the management needs working capital, for which 45% of the proceeds are earmarked. But the choice of funding is a little curious as debt is cheaper than equity and now the interest rates are also reverting to their long-term average. With strong profits and exceptional margins, can’t the company manage interest and principal costs comfortably while using the proceeds towards better growth avenues instead of tying them up for cyclical needs?

According to the response received by Mettis Global, “the working capital raised through the IPO is not intended for routine expenses; rather, it will help Zarea enhance market penetration and capture greater market share in the coming years. By boosting liquidity, it can better serve its growing customer base and support increased transaction volumes, all of which contribute to long-term growth.”

“Opting for equity over debt financing aligns with its goal of sustaining a strong, debt-free balance sheet, which supports operational flexibility as it scales. This approach also allows Zarea to reinvest profits from growth rather than channeling cash flows toward debt servicing, ultimately fueling further expansion. Choosing equity financing over debt for this purpose aligns with our commitment to maintaining a robust, debt-free balance sheet, providing the flexibility needed to scale sustainably,” it reads.

Additionally, this strategy positions Zarea to potentially declare dividend payouts in line with its company’s dividend policy, as disclosed in the prospectus. That brings us to another possible risk, one PSX investors are quite familiar with.

After all, the major shareholder, in practice, is a single individual who will own 76% of the shares (directly and indirectly), enabling them to secure approvals unilaterally. This raises corporate governance concerns, as minority shareholders risk being sidelined.

Regarding this, the Underwriter responded that all material decisions are presented to the Board for thorough review and approval. This governance framework ensures that no single individual has undue influence over decision-making. “Consequently, the question of domination by a single person or unilateral decision-making does not arise, as all significant decisions are made collectively by the Board in accordance with established policies and procedures,” it added.

Utilizing significant amount on Vehicles

For a platform-based company, which are supposed to be asset-light, Zarea also plans to use a significant portion of proceeds on capex. This includes Rs 240M to build in-house fleet and another Rs 60M for acquiring vehicles and renovating the office. Perhaps more worryingly, the entire technology component is apparently outsourced to a single vendor, raising the in-house tech capacity of Zarea.

“These allocations are strategic investments that support key aspects of Zarea’s operations, enhancing both sales outreach and logistics capabilities. The cars are designated for sales team, enabling them to engage effectively with clients, expand Zarea’s customer base, and strengthen relationships across various regions, which is crucial for its growth,” responded the underwriter. “The trucks, meanwhile, are a targeted investment to bolster Zarea’s logistics operations, adding unique competitive advantages to its e-commerce marketplace model,” it added.

“This approach allows it to meet customer demands more efficiently, ensuring timely deliveries and an overall improved service experience. These strategic investments will not only enhance Zarea’s financial performance but also position Zarea more competitively in the market, enabling it to deliver a high standard of service.”

Google Analytics data and third-party audit

As more platform-based companies hopefully come to the bourse, there’s also a major need to not only educate the investors better about their business models but also the regulators. Currently, there’s little in terms of standardization of indicators for tech entities, especially with regards to operations. Website or app analytics are a good case in point, where almost all information happens to be shared by the company itself. To encourage more transparency, we should ideally have audits from pre-approved external third parties.

Conclusion

Being the first platform-based company, Zarea’s IPO is a bold and much welcome step toward diversifying the PSX, but its long-term success will depend on maintaining transparency and strong corporate governance.

Final Word: While the decision to subscribe is ultimately in your hands, we believe that knowledge is power, and every investor deserves to know exactly where they're putting their money.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,775.00 | 64,610.00 63,260.00 | -345.00 -0.54% |

| BRENT CRUDE | 89.14 | 90.03 86.60 | 1.42 1.62% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.40 | 84.61 81.27 | 1.27 1.55% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|