Windfall Profit by Investing in Bonds

Abu Ahmed | June 02, 2023 at 03:44 PM GMT+05:00

June 02, 2023 (MLN): Investments in Bonds are made for steady income streams over the life of bonds, yet the desire for extraordinary profit continues to haunt investors. This article offers an investment strategy to satiate the very desire by investing in bonds.

When the idea of writing an article on the topic struck me the first time, I set it aside by considering it as a weird thought. Indisputably, investments in bonds are primarily for a steady income stream, not to be blessed by huge returns.

However, a deeper delve into the subject divulged a scenario contrary to the generally held perception of steady income from bonds. A deeper dug into the topic ended with evidence favoring the idea of making windfall profit by investing in bonds as a viable option.

The possibility resides within the bond structure, such as coupon rate, frequency of coupon payments, years to maturity, and presence of options.

Identifying the presence of a structural component or combination of those within bonds and understanding their role in inducing value with a change in interest rate is the key to transferring the desire for windfall profit into a reality.

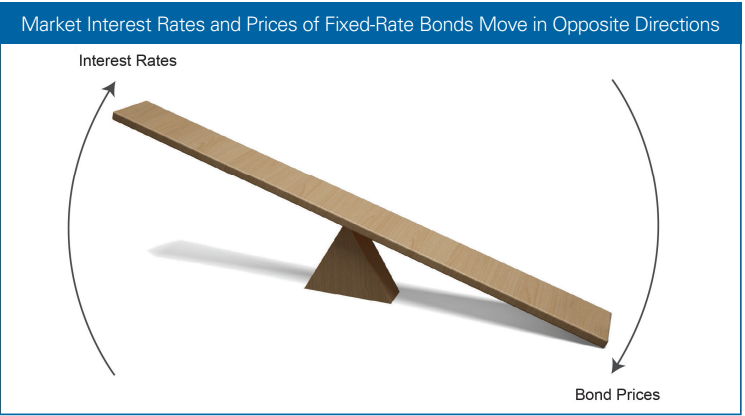

The modus operandi of windfall profit rests on the premise that the market value of bonds changes with a change in interest rate, ceteris paribus.

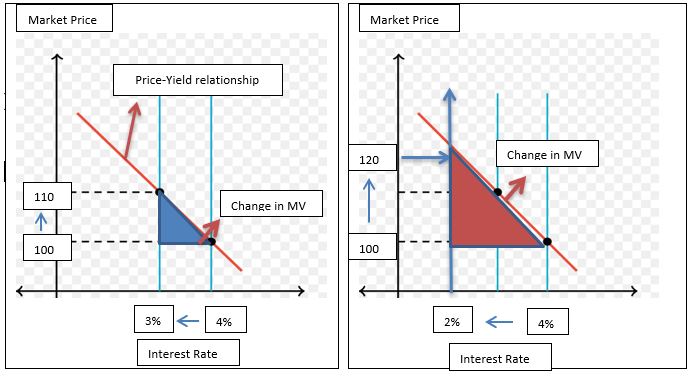

A quantum leap in the market value of bonds corresponds to a percentage decrease in interest rates. The more the interest rate decreases, the more the market value of bonds will increase. Below are the pictorial representation of incremental changes in the market value of a bond in response to a 1% and 2% decrease in interest rates.

It lays down the core principle for windfall profit from bond investing:

"If the interest rate is to fall, then invest in a bond and hold it till yield of the bond (interest rate) comes down to anticipated level."

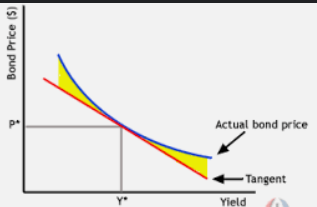

Unfortunately, the sooner the presumption of Ceteris paribus is gone, the quicker the linear relationship between price & yield turn to curve-linear. As a result, incremental change in the market value of bonds against a 1% change in interest rate no more remains constant along the interest rate continuum.

The curviness of the price-yield curve, commonly known as the convexity, determines the quantum increase in the market value of bonds against a 1% decrease in interest rate. The higher the convexity, the greater the increase in the market value.

It necessitates amendments in principle laid down initially for windfall profit by investing in bonds. Below is the comparison between the originally conceived and amended ones.

|

Basic Principle |

Modified Principle |

|---|---|

|

"If the interest rate is to fall, then invest in a bond and hold it till the yield of the bond comes down to the anticipated level." |

"If the interest rate is to fall, then:

(i)- Invest in bonds & (ii)- In the bond of higher convexity

and hold it till yield of the bond comes down to anticipated level." |

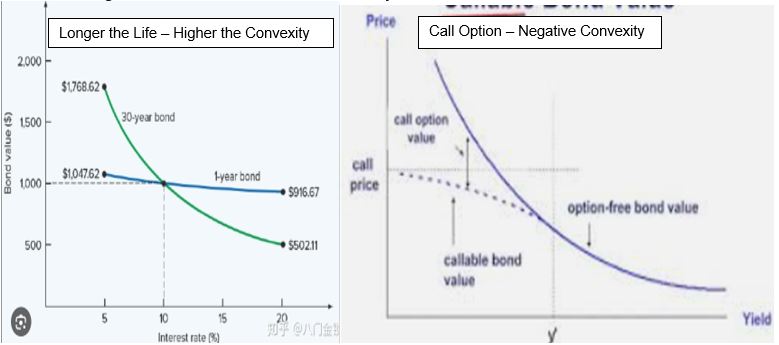

A host of factors influence the degree of convexity of a bond. The most contributing ones are coupon rate, year to maturity, and the presence of options. Each contributes differently in shaping convexity, but the overall convexity is the outcome of combined influences.

For example, bonds with higher coupon rates, lesser coupon payments in a year, and longer life are more convex than others. Similarly, bonds with options, such as call or put, respond differently than an option-free bond to a 1% change in interest rate when in the money.

Therefore, a pre-requisite for windfall profit by investing in bonds is to comprehend the intricate convexity within the context of the bond’s structure and keep recalling the same whenever making a fresh investment in bonds for the purpose.

Does this mean that the investors, who are not well versed with how bonds behave to changes in interest rate, will continue to be unprivileged of windfall profit from bond investing?

Not necessarily, with this basic understanding of the price-yield relationship, they could as well as be beneficiaries of windfall profit by investing in bonds. The following example demonstrates how this could be.

Case Study:

For example, one has Rs.100,00 for investment for windfall profit by investing in a Treasury bill. He/She has choices of investing either in 3, 6, or 12 months Treasury bills. Outline an Investment Strategy to achieve the investment objective.

Frame-work for investing in Treasury bill for Windfall profit.

Investment Objective: Earn huge capital gains.

Operational Strategy Invest in Treasury Bills with Higher Convexity

(Price of which is more prone to change due to a 1% change in interest rate, bond’s yield).

Procedures:

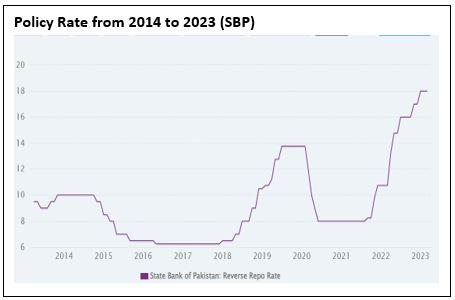

1. Take a view of the prevailing yield on Bonds (Interest rates) & Policy Rates.

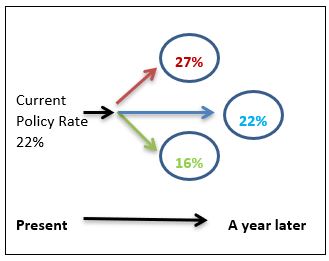

2. Take into stocks economic conditions and try to assess the direction of inflation, Policy Rate & expected change in cut-off yield of Treasury bills in upcoming auctions. (Read and listen to economists' views for the purpose. (Down the line one year)

3. Suppose, the majority of economists are of the view that interest rate (policy rate, inflation) is likely to come down significantly from the prevailing level within a year.

4. Then invest in 1-year Treasury Bills and continue to hold till the yield falls to the anticipated level.

5. Once the interest rate settled to the Predicted level, sell the bond and realize capital gains.

The rationale for choosing Treasury Bills:

Treasury Bills have been chosen to demonstrate the applicability of the concept for reasons that it offers a simplistic view of the price-yield relationship based on two factors i.e. coupon rate and time to maturity.

Risk of pursuing the Strategy:

Scenario-1:

When the Yield on 1-year Treasury Bills (bonds) remained unchanged.

In such a case, there would be no change in the market price of the Treasury bill, thereby, no capital gains. The only return would be interest income.

Scenario-2:

When the Yield on 1-year Treasury Bills increases from the current level.

In this case, the market price of the bond will decline. There will be a capital loss if the bond is divested at the prevailing price.

The Final Word:

Moreover, the all-time high return on Treasury Bills offers a conducive interest environment for testing the concepts without fear of losing much.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,571.27 436.67M | 1.06% 1878.35 |

| ALLSHR | 108,600.94 844.23M | 1.00% 1073.54 |

| KSE30 | 53,548.42 162.02M | 0.99% 525.53 |

| KMI30 | 256,725.70 154.74M | 0.76% 1936.43 |

| KMIALLSHR | 70,620.69 563.61M | 0.98% 683.55 |

| BKTi | 48,625.03 36.31M | 1.37% 658.39 |

| OGTi | 37,179.52 8.29M | 0.94% 345.85 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 60,625.00 | 61,150.00 60,590.00 | 790.00 1.32% |

| BRENT CRUDE | 72.63 | 73.51 72.27 | -1.11 -1.51% |

| RICHARDS BAY COAL MONTHLY | 115.00 | 0.00 0.00 | 0.50 0.44% |

| ROTTERDAM COAL MONTHLY | 126.50 | 126.50 125.90 | 0.50 0.40% |

| USD RBD PALM OLEIN | 1,157.50 | 1,157.50 1,157.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 69.44 | 70.21 69.05 | -0.90 -1.28% |

| SUGAR #11 WORLD | 14.01 | 14.09 13.81 | 0.06 0.43% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|