Weekly Market Roundup

Abdur Rahman | May 31, 2024 at 07:20 PM GMT+05:00

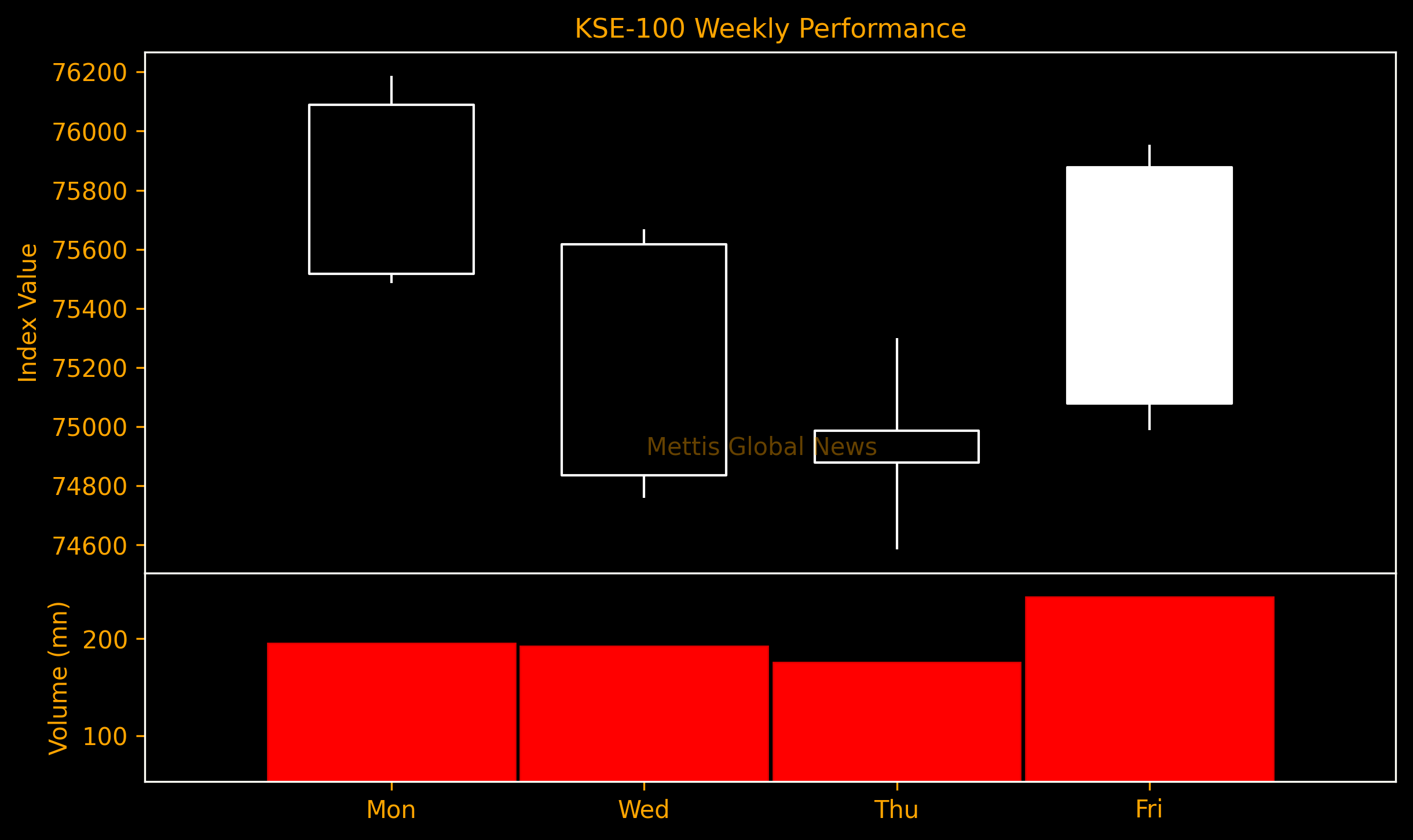

May 31, 2024 (MLN): The benchmark KSE-100 index closed this week at 75,878 showing a decrease of 105 points or 0.1%.

On the currency front, the Pakistani Rupee recorded a marginal decline of 0.04% WoW. In USD terms, the 100-index lost 0.2%.

Throughout the week, KSE-100 traded in a range of 1,602 points, between a high of 76,187 (+204) and a low of 74,585 (-1,398) points.

PSX average traded volume was recorded at 447 million shares worth Rs17.1 billion, marking a decrease of 19.9% WoW in the number of shares and 5.2% WoW in traded value.

Meanwhile, the PSX market capitalization decreased by $296.57m or 0.8% to $36.54bn over the week. In PKR terms, market capitalization stood at Rs10.17 trillion.

Investors are eyeing the inflation data due on Monday, which is expected to show a softer than previously anticipated reading, bolstering bets for an interest rate cut in the upcoming monetary policy meeting.

The central bank is scheduled to meet on June 10, 2024, to announce its next decision. Investors are ramping up bets for at least 100 basis points (bps) cut.

Meanwhile, headline inflation is expected to decelerate significantly to about 13-14% YoY in May 2024, pushing real interest rates above 8%.

The government conducted two auctions during the week, picking up Rs501bn through T-bills at lower yields, and Rs421bn through PIB-PFL auction.

T-bill auction witnessed a fall in cutoff rates across all tenors, with the decline going as much as 60bps.

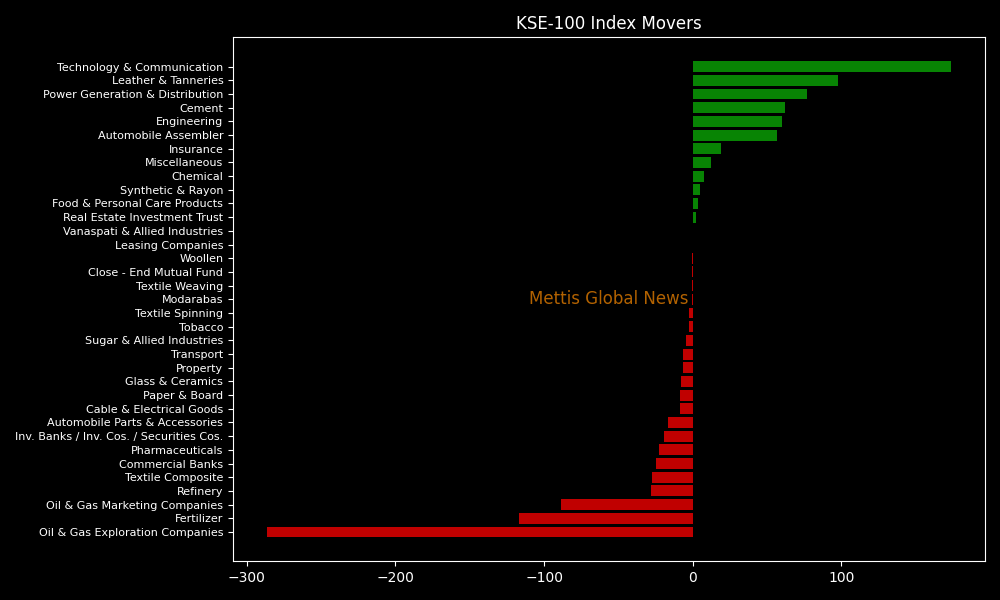

Top Index Movers

Sector-wise, top negative contributors were Oil & Gas Exploration Companies with (286pts), Fertilizer (117pts), Oil & Gas Marketing Companies (89pts), Refinery (28pts), and Textile Composite (27pts).

Contrary to that, the positive contributions came from Technology & Communication (174pts), Leather & Tanneries (97pts), Power Generation & Distribution (77pts), Cement (62pts), and Engineering (60pts).

The worst-performing stocks during the week were FFC (128pts), OGDC (117pts), BAHL (82pts), PPL (77pts), and BAFL (56pts).

Whereas, SYS, HUBC, SRVI, MEBL, and MTL added 179, 108, 97, 71, and 66 points to the index respectively.

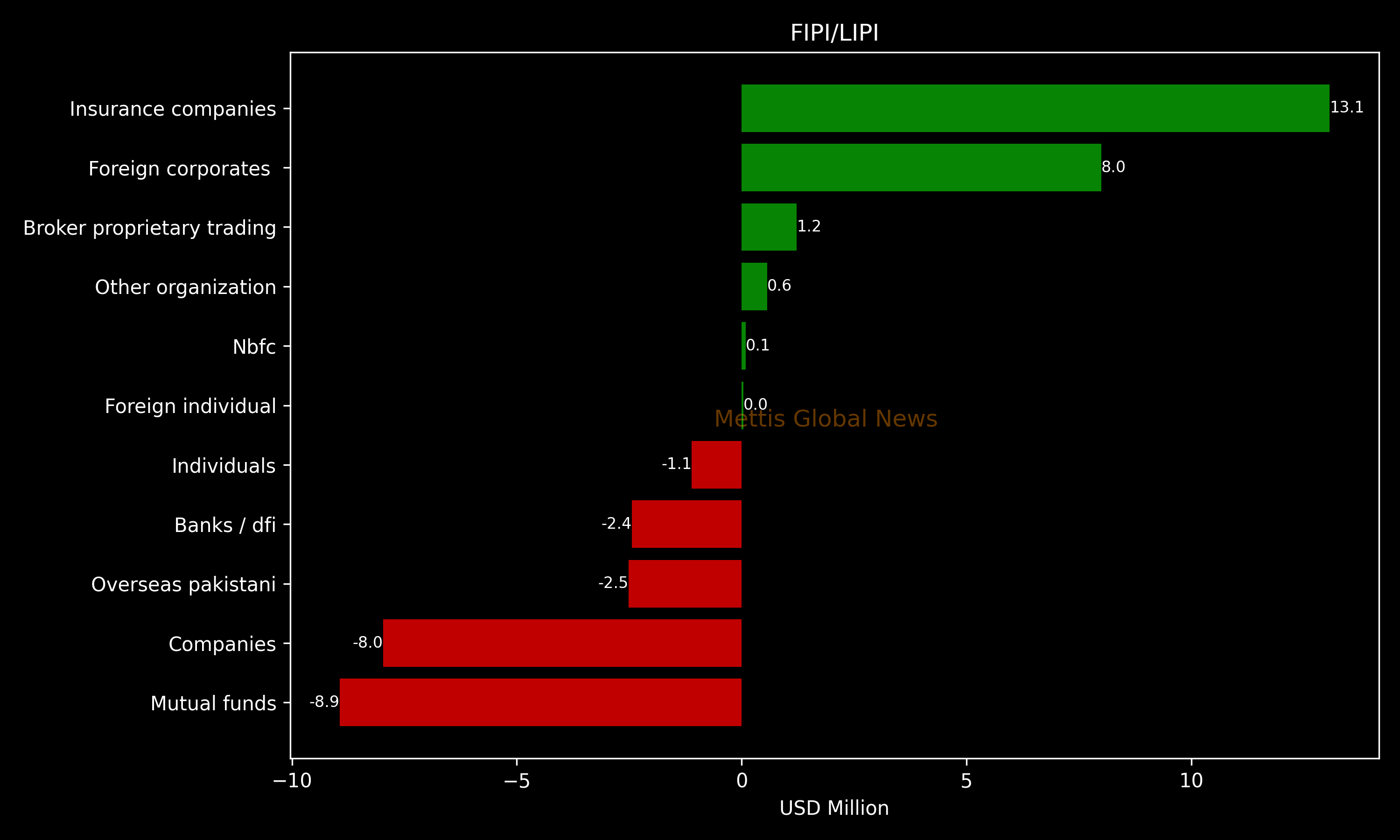

FIPI/LIPI

Foreign investors turned to net buyers during the week, acquiring $5.52m worth of equities.

Flow-wise, Insurance companies were the dominant buyers, with a net investment of $13.08m.

They allocated the majority of their capital, $4.73m, to Power Generation and Distribution, while divesting from the Technology and Communication sector, amounting to $0.1m in sales.

On the other hand, the leading sellers were Mutual Funds, with a net sale of $8.94m.

Their most substantial sales activity was in Oil and Gas Exploration Companies, amounting to $2.43m, while they acquired $0.16m of equities in the Food and Personal Care Products.

To note, the KSE-100 has gained 34,426 points or 83.05% during the fiscal year, whereas the ongoing calendar year has witnessed a cumulative increase of 13,427 points, equivalent to 21.5%.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 173,962.82 313.69M | 1.30% 2237.52 |

| ALLSHR | 104,178.62 550.40M | 0.93% 964.13 |

| KSE30 | 52,166.33 164.58M | 1.26% 649.19 |

| KMI30 | 250,496.48 141.11M | 1.59% 3930.77 |

| KMIALLSHR | 67,844.06 318.73M | 1.20% 801.29 |

| BKTi | 47,430.11 44.68M | 0.28% 130.40 |

| OGTi | 36,386.96 9.01M | 0.13% 45.59 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 74,260.00 | 74,260.00 73,715.00 | 545.00 0.74% |

| BRENT CRUDE | 91.89 | 92.95 89.93 | -0.81 -0.87% |

| RICHARDS BAY COAL MONTHLY | 117.00 | 0.00 0.00 | -0.75 -0.64% |

| ROTTERDAM COAL MONTHLY | 130.25 | 131.75 130.00 | -0.20 -0.15% |

| USD RBD PALM OLEIN | 1,157.50 | 1,157.50 1,157.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 87.76 | 89.02 86.35 | -1.14 -1.28% |

| SUGAR #11 WORLD | 14.07 | 14.35 13.90 | 0.14 1.01% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|