SBP's aggressive rate cut, IMF deal: A Dual Success

By Rafay Malik | September 13, 2024 at 02:20 PM GMT+05:00

September 13, 2024 (MLN): Yesterday’s Monetary Policy Committee (MPC) Meeting gave Pakistan more than just an unexpected rate cut as it assured the implementation of the delayed and deprived $7 billion Extended Fund Facility (EFF) from the International Monetary Fund (IMF).

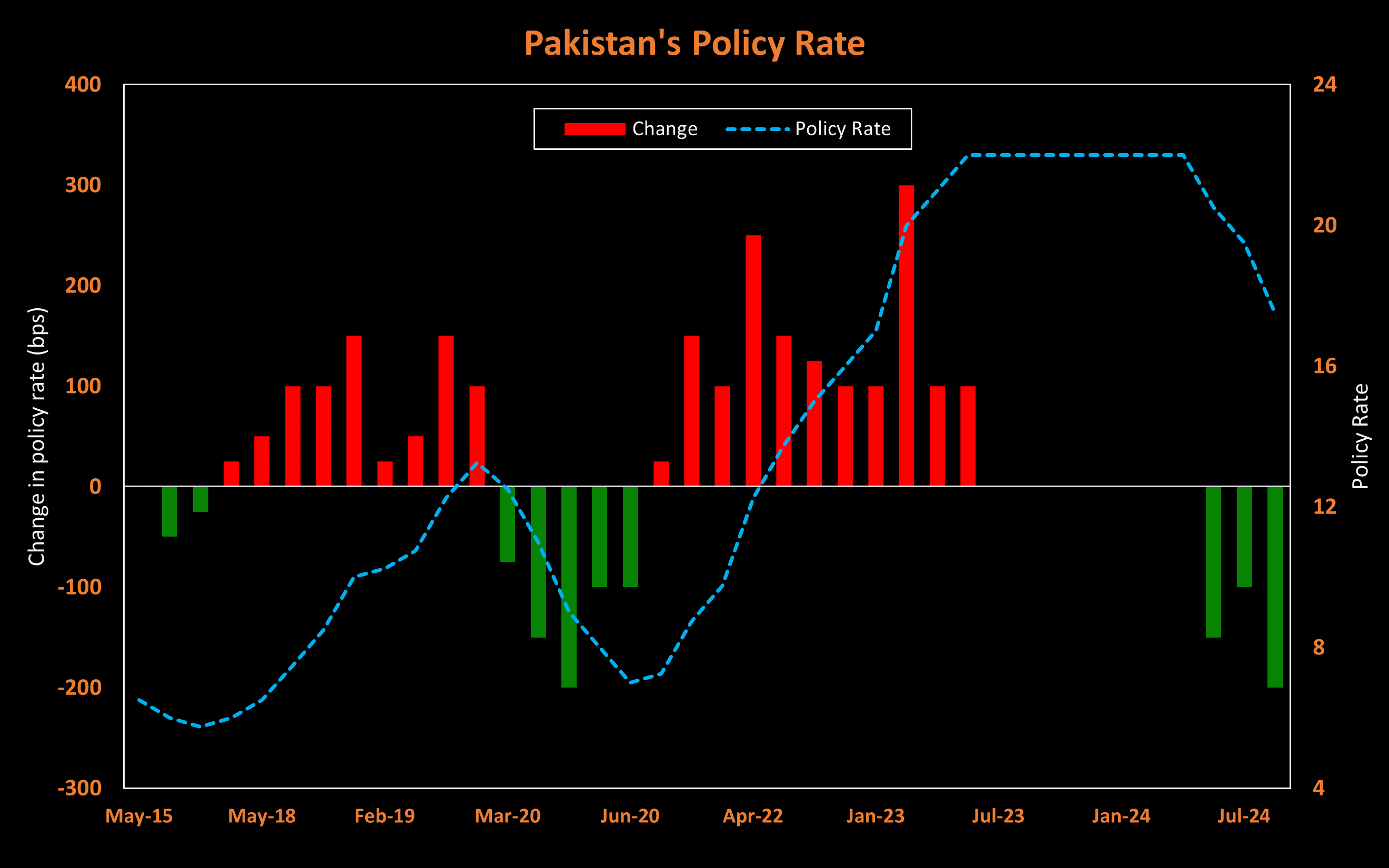

The State Bank of Pakistan (SBP), which was anticipated to slash the policy rate by 150 basis points, decided to cut it by a greater margin of 200bps, which stands out as the highest rate cut in 53 months.

Well, this excludes the demand/ hopes of business councils who were eager to see a reduction of greater magnitude — around 300 to 400 basis points — considering the price gains figures sliding to single digits after almost 3 years.

Nonetheless, as the policy rate was down by a whooping 450bps from its peak of 22%, the recent rate cut is embraced to be more fruitful, especially by the highly leveraged sectors such as cement, steel and auto sectors.

To note, the pace of disinflation outpaced expectations due to the delay in the implementation of planned increases in administered energy prices and favorable movement in global oil and food prices.

Consequently, as expected, Pakistan’s stocks reacted positively, with the benchmark KSE-100 index surging by over 900 points during the early trading hours of Friday.

On the other side, what mainly generated optimism was the announcement by the governor of the State Bank of Pakistan, Jameel Ahmad that the nation has arranged more than $2bn in financing and assurances from lenders.

This was seen as the main hurdle for the IMF loan, or in other words, it clarifies why Pakistan was not on the IMF’s agenda as of now.

While positive announcements are not uncommon for the country, confidence actually emerged when IMF Director of Communications Julia Kozek, during a press briefing, declared that the Executive Board is set to meet on September 25 to review and potentially approve the EFF for Pakistan.

This helped dispel the negativity and doubts arising that the government was giving fake hopes about the IMF once again rescuing Pakistan, especially as the country's name was not on the IMF's agenda, until September 18.

Prime Minister Shehbaz Sharif stated lately that the friendly nations have assisted Pakistan in meeting the conditions required to secure a bailout from the IMF.

As the program is now affirmed to be secured this month from both sides, a mixed sentiment might arise in the country.

The sentiment can be divided into two segments, one of which expects Pakistan to improve its structural position by introducing reforms under the guidance and monitoring of the global lender, as it did with the program reached in June 2023.

Conversely, the other segment fears strict reforms, which, based on the practical example of the previous program, could involve higher taxes and duties on sectors to boost the government's revenue base.

Even so, as time passes and reviews of the EFF progress, the country would unlock substantial Dollars which would boost its foreign exchange reserves and turn out to be favorable for the domestic currency.

Considering these improvements, there is no doubt that the country is making efforts to steer towards stability.

However, success is not fully assured as Pakistan continues to grapple with certain economic issues and challenges such as rising debt burdens, markup payments, a massive tax target, and a GDP growth goal.

Copyright Mettis Link News

Related News

.jpeg)

.png)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 132,747.18 102.88M |

-0.49% -656.01 |

| ALLSHR | 83,057.26 574.19M |

-0.16% -130.79 |

| KSE30 | 40,398.35 36.15M |

-0.62% -253.11 |

| KMI30 | 191,037.16 40.96M |

-0.54% -1046.75 |

| KMIALLSHR | 55,750.43 293.52M |

-0.17% -97.27 |

| BKTi | 36,236.74 6.38M |

-0.51% -186.14 |

| OGTi | 28,271.91 7.34M |

-0.58% -165.70 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,155.00 | 109,545.00 108,625.00 |

-60.00 -0.05% |

| BRENT CRUDE | 70.15 | 70.18 69.85 |

0.00 0.00% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

2.05 2.15% |

| ROTTERDAM COAL MONTHLY | 106.65 | 106.65 106.25 |

0.50 0.47% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.32 | 68.34 67.78 |

-0.01 -0.01% |

| SUGAR #11 WORLD | 16.15 | 16.37 16.10 |

-0.13 -0.80% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|