Banking sector kicks off Q1 2024 with a bang, records upbeat earnings

Rafay Malik | May 22, 2024 at 03:51 PM GMT+05:00

May 22, 2024 (MLN): Pakistan’s most profitable sector, commercial banks sustained its robust profit growth in the first quarter of 2024, primarily supported by consistently rising interest earnings and a significant uptick in non-markup income during this period.

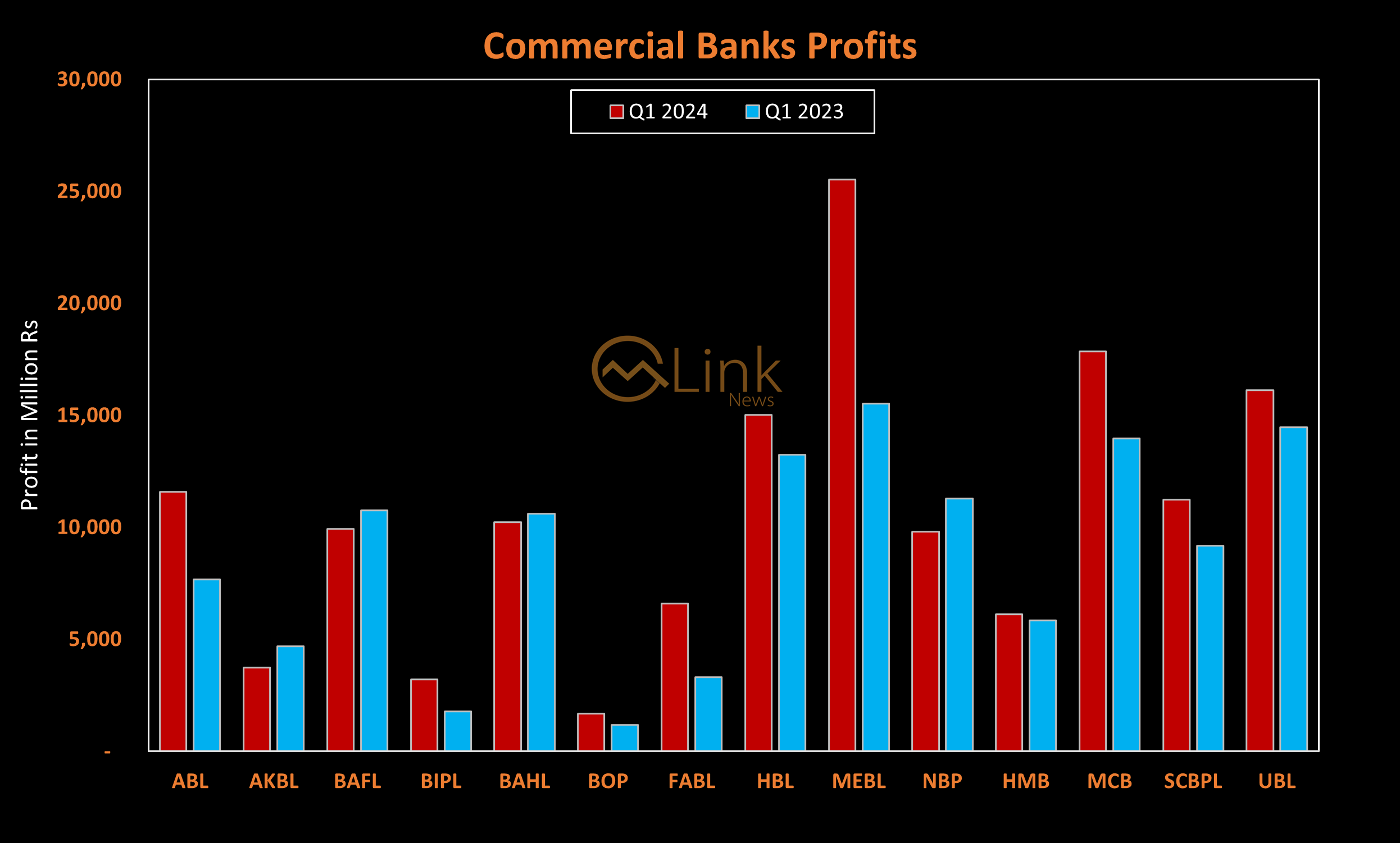

The KSE-100 listed Banking sector, comprising 14 members, generated a consolidated profit of Rs148.79 billion, which is 20.34% year-on-year (YoY) higher compared to the bottom line of Rs123.64bn in the same quarter last year.

Emerging as the most profitable entity among the correspondents, Meezan Bank Limited (MEBL) retained its dominance by achieving total quarterly earnings of Rs25.54bn.

MCB Bank and United Bank followed the lead and managed to secure second and third ranks in the profit race by earning Rs17.85bn and Rs16.14bn, respectively in Q1 2024.

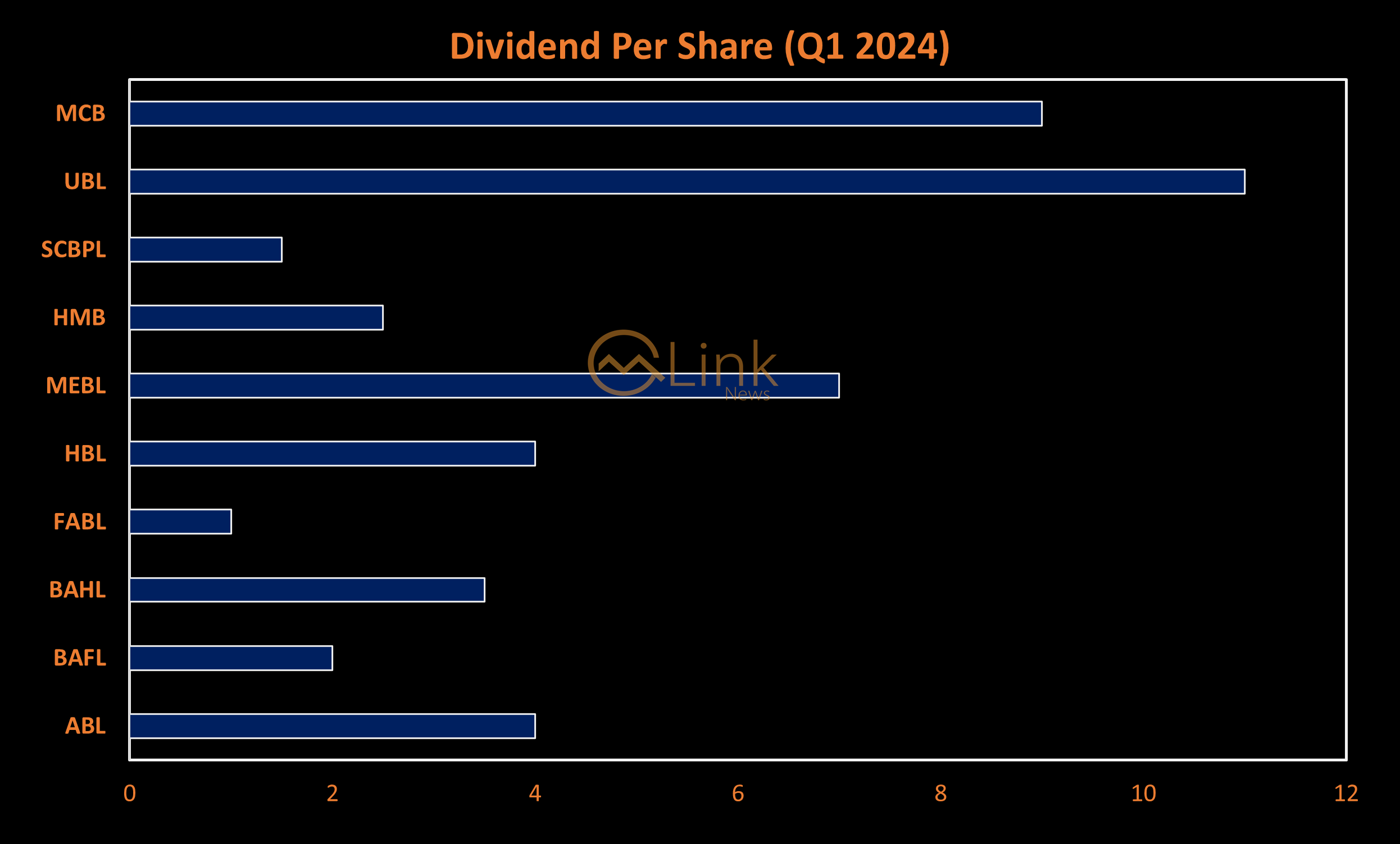

With respect to returns in the form of dividends to shareholders, UBL took the lead by declaring the highest dividend of Rs11 per share.

MCB and MEBL were the next in line, announcing dividends of Rs9 and Rs7 per share, respectively, in the first quarter of 2024.

Meanwhile, Askari Bank, Bank Islami, NBP, and Bank of Punjab did not pay dividends this quarter.

The huge profit rally observed during the review period spreads from the past year (2023), in which the majority of the banks recorded their highest-ever profits and dividend payouts.

Read: Pakistani banks cash in on soaring interest rates, achieve record profits in 2023

However, certain well-known banks including Askari Bank, Bank Alfalah, Bank AL Habib and NBP witnessed shrinking profits due to expanded operational expenses and heavy tax burden, which outweighed the shine in both interest and non-markup income this quarter.

Nonetheless, the majority of the banks successfully managed to capitalize on higher interest rates by booking a significantly higher income, enabling them to manage their rising markup and non-markup expenses.

Inflation in Pakistan was on the verge of menace, due to which the central bank remained cautious and maintained the policy rate at a record high of 22%, compared to the average interest rate of 18.5% in Q1 2023.

As a result, banks persistently booked higher interest earnings, with these 14 members earning interest income of Rs1.65 trillion during Q1 2024, which is around 58% YoY higher compared to last year.

The higher interest rate also exposed the sector to increased borrowing costs, resulting in the sector's interest expenses spiking by 75.97% YoY to 1.24bn in Q1 2024.

As the rise in the average volume of earning assets and timely repositioning within the asset book outweighed the impact of high percentage growth in interest charges, the overall interest income scenario for the sector improved, resulting in a 20.86% increase in net markup income to Rs415.7bn in Q1 2024.

Similarly, the non-markup income surged to Rs119.49bn (+67.23%) against Rs71.45bn in the corresponding period last year with major contributions coming in from fee commission income of Rs61.77bn (+32.83%), Foreign exchange income of Rs23.83bn (+5.22%) and net gain on securities of Rs19.93bn.

The transition of Pakistan’s economy to a recovery zone resulted in expanded banking operations with improved customer and interbank flows, increased debit card and branch banking services and home remittances.

The stable economic conditions further triggered growth in foreign exchange income as the Pakistani Rupee (PKR) remained relatively flat against the mighty Dollar, supported by healthy trade flows during the review quarter.

Further analysis of the sector’s profit and loss account reveals a surprising trend in the sector’s net flow through securities, shifting from a loss of around Rs5bn to a massive gain of Rs19.93bn in Q1 2024, as these banks booked massive capital gains on the sale of government and foreign securities.

The boosted non-interest income when merged with the interest income took the sector's total revenue to a massive Rs535.18bn, 28.84% YoY higher compared to the total income in the corresponding period.

Amidst a persistently high inflationary environment, costs related to staff, branch expansion, technological upgradation, and property all surged and the sector’s total non-markup expenses reached Rs227.21bn (+21.65% YoY).

Operating expenses were reported at Rs220.56bn, while worker’s welfare fund and other charges stood at Rs5.67bn and Rs976.02 million in Q1 2024.

The profit and loss account further draws attention towards provisional charges which narrowed significantly by 38.62% YoY to Rs9.05bn owing to reversals observed by certain banks in Q1 2024.

The reduced provisioning is attributed to the economic recovery and the high base effect during the review period as banks recorded relatively higher provisions in the same period last year due to economic struggles.

On the taxation front, commercial banks barred a cumulative tax burden of Rs150.14bn in Q1 2024, which is 66.4% YoY higher compared to the Rs90.24bn paid in the same quarter last year.

To sum up, rising operating expenses along with significant tax charges constrained the sector's profits.

However, the massive surge in the total income and reduction in the provision expense outweighed these restrictions, leading to a 20.34% YoY higher profit after tax.

| Consolidated Profit and Loss Account for the quarter ended on March 31 2024 (Rupees in '000) | |||

|---|---|---|---|

| Mar-24 | Mar-23 | % Change | |

| Mark-up/return/interest earned | 1,653,061,598 | 1,047,096,097 | 57.87% |

| Mark-up/return/interest expensed | 1,237,363,752 | 703,155,609 | 75.97% |

| Net mark-up/interest income | 415,697,846 | 343,940,488 | 20.86% |

| NON MARK-UP/INTEREST INCOME | |||

| Fee and commision income | 61,773,972 | 46,504,829 | 32.83% |

| Dividend income | 6,556,965 | 5,011,730 | 30.83% |

| Foreign exchange income | 23,831,324 | 22,649,526 | 5.22% |

| Income from derivatives | 3,093,295 | (4,972,714) | -162.21% |

| Gain on sale of securities - net | 19,931,223 | (4,998,856) | -498.72% |

| Share of profit of associates & Joint Ventures | 2,682,648 | 1,417,736 | 89.22% |

| Other income | 1,617,432 | 5,838,325 | -72.30% |

| Total non mark-up/interest income | 119,486,859 | 71,450,576 | 67.23% |

| Total Income | 535,184,705 | 415,391,064 | 28.84% |

| NON MARK-UP/INTEREST EXPENSES | |||

| Operating expenses | 220,563,425 | 182,456,661 | 20.89% |

| Workers welfare fund | 5,667,824 | 3,982,801 | 42.31% |

| Other charges | 976,023 | 335,124 | 191.24% |

| Total non mark-up/interest expenses | 227,207,272 | 186,774,586 | 21.65% |

| Profit before provisions | 307,977,433 | 228,616,478 | 34.71% |

| Credit loss allowance and write offs - net | 9,053,932 | 14,751,284 | -38.62% |

| Extra ordinary / Unusual items | - | - | - |

| Profit before taxation | 298,923,501 | 213,865,194 | 39.77% |

| Taxation | 150,136,734 | 90,224,574 | 66.40% |

| Profit after taxation | 148,786,767 | 123,640,620 | 20.34% |

It is worth highlighting that the banking sector composes the largest (25.21%) weightage to the KSE-100 index.

Hence, the stellar earnings performance by commercial banks in this quarter and past year emerges as one of the major factors driving the upward rally in the local bourse.

Key Banking Stats as of Q1 2024

Over the period of rising interest rates in the country, the public began depositing money in banks due to which total deposits held by scheduled banks surged 20.11% YoY to Rs28.32 trillion in March 2024 compared to Rs23.58tr in March 2023.

This contraction restricted economic activity due to which advances only saw a meager 1.09% YoY rise to Rs11.96tr compared to Rs11.83tr from a year ago.

Advances to Deposit Ratio (ADR) stood at 42.24% showing a decrease of 795 bps on a yearly basis.

However, the commercial banks set out and made robust investments reaching Rs26.27tr as of March 2024, compared to Rs19.22tr from a year ago, showing a YoY increase of 36.71%.

Accordingly, the Investment to Deposit Ratio (IDR) moved up by 1126 bps to 92.76% in March 2024.

On the other hand, an inverse trend was noted in the banking sector spread, as it dropped by 51bps to 7.53% in March compared to 7.02% in the same month last year.

Future Outlook

MCB highlights two key external factors that could impact Pakistan's economic performance in 2024: firstly, global energy prices influenced by geopolitical tensions, and secondly, climate change.

Moreover, concerns regarding Pakistan's foreign debt obligations persist, especially given challenges in increasing export earnings and a negative trade balance.

Addressing these issues will require crucial support from the IMF's Extended Funding Facility (EFF) and external inflows from friendly nations, says MCB

However, achieving these objectives will entail rigorous fiscal and monetary adjustments to meet IMF requirements, including reducing gas and power circular debts, adopting a flexible exchange rate, and enhancing tax revenue collection.

This exposes a threat to the current disinflation trend being observed in the country and may further restrict the population's purchasing power.

The favorable base effect and reduction in food prices eased the consumer price index (CPI) for April 2024 to 17.3% YoY. On a monthly basis, the CPI recorded a decline of 0.4%, marking the first decrease since June 2023.

This improved the position of real interest rates, which transitioned to the positive zone in March 2024, after a hectic period of over 3 years.

Read: CPI inflation falls to 17.3% in April 2024

This downward trend in inflation has strengthened the market’s expectations for a transition by the State Bank of Pakistan (SBP) towards policy rate cuts by June 2024 to boost economic activity, which had been restricted earlier due to aggressive inflation in the country.

The potential impact of declining interest rates would be neutral, as although banks may book relatively lower interest income, the markup expenses would also decrease accordingly.

Therefore, the outcome depends on each bank's efficiency in generating higher income and managing expenses.

On the other hand, rate cuts would stimulate economic activity, leading to expanded consumption and investments. This, in turn, would result in increased banking transactions and a boost in the sector’s non-markup income.

Hence, this indicates a robust sector performance in response to rate cuts.

Allied Bank had a different view and said that despite a deceleration in domestic inflation the level of inflation remains high. Hence the central bank may keep interest rates higher for longer with the aim of reducing inflation to the target range of 5-7% by September 2025.

Regardless, the banking sector is poised to maintain its upward trajectory, whether through increased interest income or by expanding lending and banking operations with monetary easing.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 180,014.93 294.91M | 1.66% 2931.71 |

| ALLSHR | 108,372.13 738.00M | 1.30% 1386.88 |

| KSE30 | 53,821.81 143.92M | 1.87% 985.50 |

| KMI30 | 253,547.39 118.57M | 1.66% 4144.78 |

| KMIALLSHR | 69,491.95 365.01M | 1.26% 862.49 |

| BKTi | 51,843.62 70.63M | 2.49% 1258.04 |

| OGTi | 34,802.66 8.81M | 1.04% 358.83 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,790.00 | 65,030.00 64,760.00 | -290.00 -0.45% |

| BRENT CRUDE | 79.13 | 79.41 79.06 | -0.32 -0.40% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 1.75 1.65% |

| ROTTERDAM COAL MONTHLY | 116.50 | 116.50 116.50 | -1.40 -1.19% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 74.75 | 75.27 74.70 | -0.47 -0.62% |

| SUGAR #11 WORLD | 15.17 | 15.28 15.06 | 0.13 0.86% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|