The Exit That Keeps Giving — But Not to You

MG News | April 06, 2026 at 11:50 PM GMT+05:00

April 06, 2026 (MLN): When Pak Suzuki Motor Company (PSMC) delisted from the Pakistan Stock Exchange in April 2024 at Rs609 per share, a price its own management proposed at Rs406 before a belated 50% bump, minority shareholders were told they were being offered a "fair exit."

Sixteen months

later, the company's audited results for the year ended December 31, 2025, have

turned that assurance into a notable disconnect.

The numbers tell a story that minority shareholders always suspected but could not prove in time.

They were cashed out at the bottom of the curve, handed a fraction of what the enterprise was worth, and left to watch from the outside as the parent company, Suzuki Motor Corporation of Japan, now holding 99.12% of PSMC, harvests the rewards of a business in full bloom.

Valuation

At the delisting price of Rs609 per share across 82.3 million shares, PSMC's implied market capitalisation was roughly Rs50 billion.

That figure now sits beneath the company's own book equity of Rs51.8 billion

as at December 31, 2025, meaning minority shareholders were bought out at a

price that did not even fully account for the net assets they were

surrendering, let alone the earnings engine behind them.

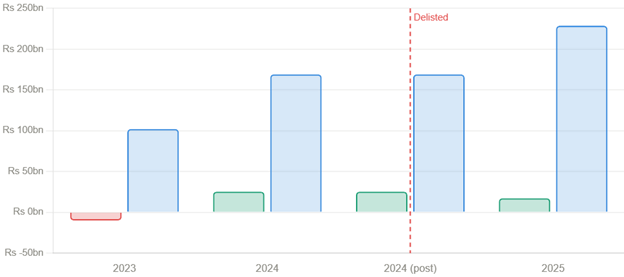

The 2025 income statement makes this more pointed. Sales surged 35% year-on-year to Rs 228.6 billion.

Automobile production rose to

87,404 units from 64,241, a 36% jump, still running at barely 58% of the

plant's 150,000-unit double-shift capacity.

Profit before tax stood at Rs24.5 billion. The Rs17.2

billion profit after tax reflects a materially higher tax charge of Rs7.3

billion, including a Rs3.5 billion prior-year adjustment following a Supreme

Court ruling, rather than any deterioration in the business.

Strip that one-off

out, and the operating performance is as strong as 2024, if not stronger.

In the two full years since delisting, the

parent company has collected profits of roughly Rs42 billion on an investment

for which it paid minority shareholders just Rs50 billion in total.

The implied payback period on the buyout is under three

years. That is not a fair exit; it is a bargain acquisition dressed in

regulatory language.

The royalty extraction continues, undisturbed

One of the most serious concerns raised by minority

shareholders in 2023 and 2024 was the royalty structure. Pak Suzuki pays its

Japanese parent a royalty and technical fee that was described then as

commercially aggressive.

The 2025 financials confirm the practice has not moderated; it has accelerated.

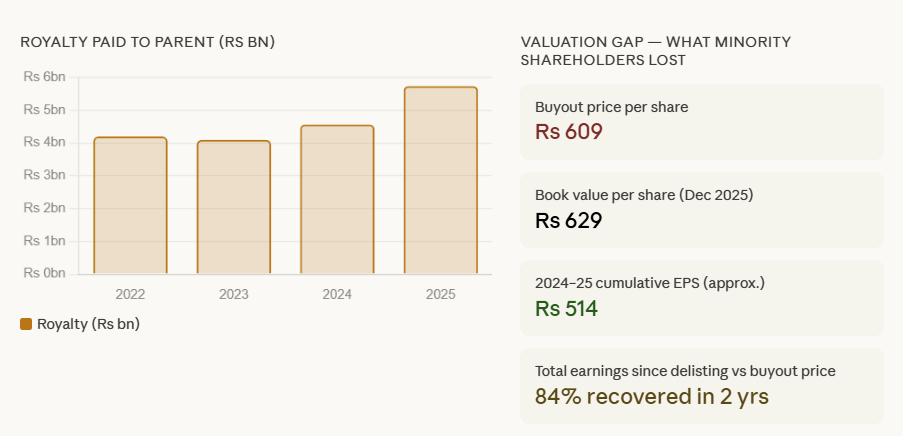

Royalty and technical fee paid to Suzuki Motor Corporation

reached Rs5.56 billion in 2025, up from Rs4.57 billion in 2024 and Rs4.2

billion in 2022. The supervision fee, a separate line item, added another Rs1.14 billion.

Together, payments to the Japanese parent on these two heads alone amounted to Rs6.7 billion in a single year, against a total equity base of Rs51.8 billion.

The same minority shareholders who once bore this royalty

drag without consent are now excluded from the recovery that follows.

Note 32.1.3 in the 2025 financial statements confirms the royalty arrangement remains unchanged in structure. What has changed is the scale, because the revenue base has grown. That is precisely the upside that minorities were denied.

Capital expenditure

Perhaps the most telling number in the 2025 financial

statements is capital expenditure: Rs14.5 billion during the year, building on

Rs8.6 billion in 2024.

Capital

work-in-progress has ballooned from Rs2.9 billion at end-2023 to Rs11.6

billion by December 2025. Contracted but unincurred capex stands at a further

Rs11.1 billion as at the reporting date.

This is not a company in maintenance mode. It is a company in aggressive expansion mode, new dies, new production lines, and new product development.

The biogas-powered plant that came to light after the delisting

was not an improvised pivot; it was part of a strategic investment programme

that was evidently under consideration during the very period when the

delisting was being structured and priced.

This raises an important question for the Voluntary Delisting Committee and the SECP. At the time when management was negotiating a buyout price based on a relatively weak balance sheet and recent losses, what visibility did they have regarding the upcoming capex pipeline, cost optimization plans, and the anticipated production ramp-up?

The financial

statements of 2024 and 2025 suggest the answer is considerably more than they

disclosed.

Book Value

At 82.3 million shares, the total equity of Rs51.8 billion as at December 31, 2025, translates to a book value of approximately Rs629 per share, already above the Rs609 buyout price, before ascribing any earnings multiple.

Add the cumulative profits earned in the two years since delisting, Rs25.2 billion in 2024 and Rs17.2 billion in 2025, totalling Rs42.4 billion, or

roughly Rs515 per share, and the picture becomes stark.

Minority shareholders received Rs609 per share for an asset

that, had they retained it, would have generated Rs515 in earnings

in under two years, while the underlying equity also appreciated.

No credible valuation framework, earnings-based,

asset-based, or comparable-company, would have produced Rs609 as a fair price

given what was about to unfold.

The regulatory architecture

Earlier coverage of this case called for the adoption of a

Reverse Book Building mechanism for voluntary delistings, a process that allows

shareholders to discover the price themselves rather than accept a floor set by

valuators working from dated balance sheets at the instruction of the very

party seeking to buy them out.

The 2025 results make that call more urgent. PSMC's

delisting has become a textbook case study in why the current framework is

structurally biased against minority shareholders: the acquirer controls the

timeline, selects the valuator, proposes the floor price, and presents an

information set of its choosing.

The Voluntary

Delisting Committee, as constituted, is left to negotiate upward from an

already-compromised starting point, as it did, pushing the price from Rs406 to

Rs609 without ever interrogating the forward-looking information that

management held.

The SECP must go further than process reform. Minority investors who were bought out at Rs609 and who have watched the company earn Rs515 per share in the two years since have a legitimate grievance that deserves formal examination.

A third-party investigation into what PSMC's

management knew, and when, about the 2024 and 2025 performance trajectory is

not optional if the regulator wishes to be taken seriously as a protector of

market integrity.

Car Sales Comparison

Total Suzuki car sales peaked at 144,070 units in FY2017-18, then crashed

through COVID, supply disruptions, and the economic crisis, hitting a 12-year

low of just 51,697 units in FY2023-24, the very year PSMC was delisted at Rs

609/share.

The parent company timed the exit with precision that, charitably,

can be called fortunate.

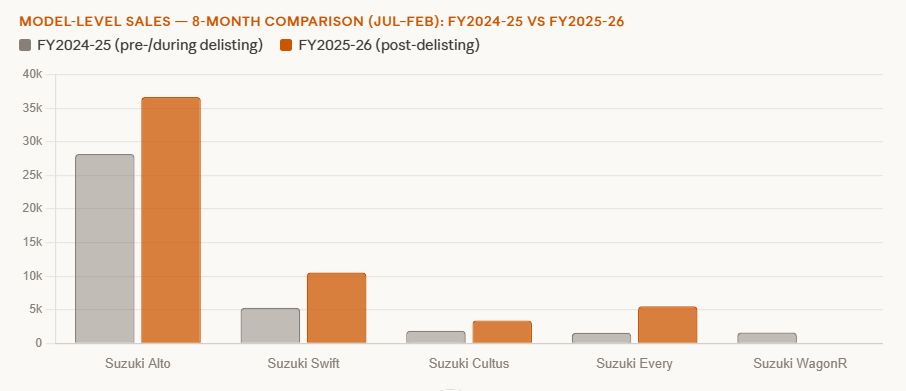

What happened next, model by model (8-month YoY from PAMA

Feb 2026 report):

- Suzuki

Alto — from 28,194 to 36,694 units (+30%), and this is with WagonR

discontinued, so Alto absorbed that volume entirely

- Suzuki

Swift — from 5,295 to 10,555 units (+99%, essentially doubled)

- Suzuki

Cultus — from 1,887 to 3,423 units (+81%)

- Suzuki

Every — from 1,577 to 5,520 units (+250%, a standout recovery)

- Suzuki WagonR — discontinued (only 53 clearance sales vs 1,608)

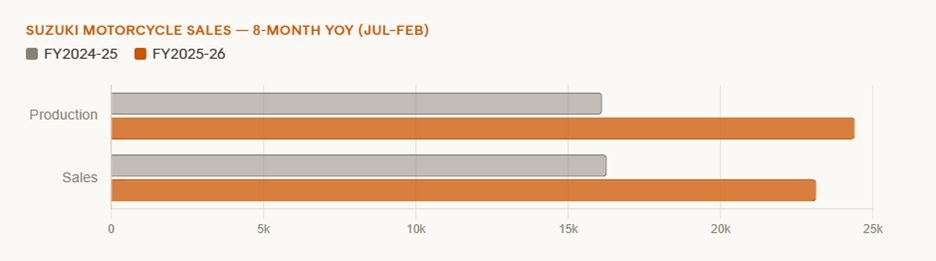

Motorcycles tell the same story: production up 51%

and sales up 42% year-on-year in the 8-month comparison, the segment minority

shareholders also held exposure to through PSMC's motorcycle division.

PSMC was delisted at the precise 12-year sales trough

(FY2023-24: 51,697 units). By FY2024-25 (first full post-delisting year) sales

rebounded +30% to 67,233. The 8-month FY2025-26 data points to an annualised

~84,000 units — 63% above the delisting-year base. Motorcycle sales have jumped

42% YoY. Minority shareholders exited exactly when they should have held on.

Bottomline:

Pak Suzuki Motor Company has delivered two consecutive years

of strong profitability, accelerating revenue, and a capital investment

programme that signals confidence in the decade ahead. Its 2025 results, Rs

228.6 billion in sales, Rs 24.5 billion profit before tax, and Rs 51.8 billion

in equity, are evidence to the underlying quality of the franchise.

They are also a monument to what minority shareholders were

denied.

The parent company now owns 99.12% of an enterprise it

acquired a significant piece of at Rs 609 per share, a price the market, armed

with the information now in the public domain, would never have accepted.

The regulatory architecture that permitted this outcome is overdue for reform. And the former minority shareholders of PSMC, who held their ground longer than most, deserve more than a footnote in the company's delisting announcement. They deserve answers, and they deserve compensation.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,070.00 | 64,215.00 64,070.00 | -145.00 -0.23% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|