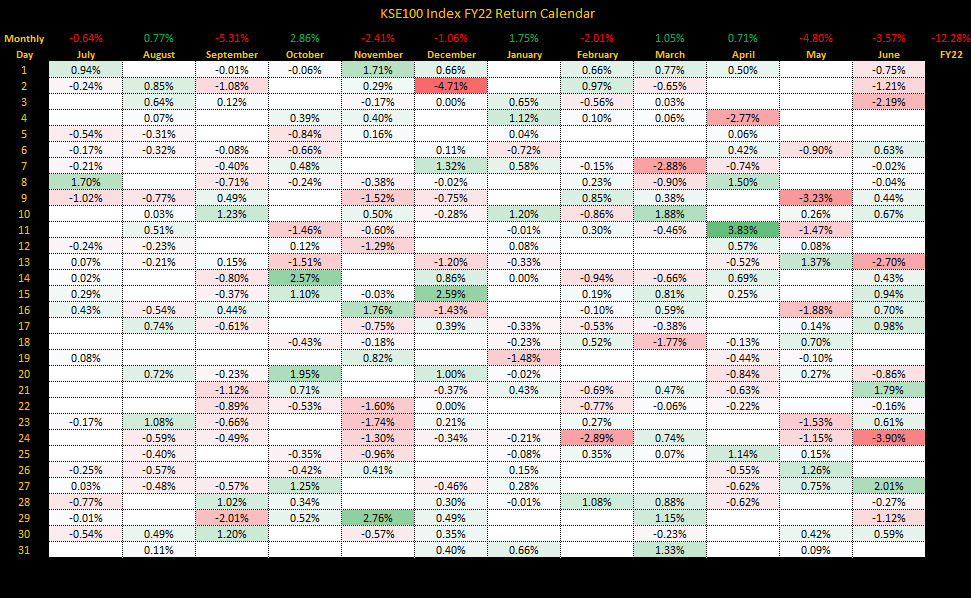

July 02, 2022 (MLN): FY22 proved to be a tumultuous year for Pakistan’s stock market as the benchmark KSE-100 index posted a negative return of 12.3%, which was the lowest after FY19 when the index delivered a return of -19%.

While on the back of hefty PKR depreciation of Rs47.30 or 23.09% YoY during FY22, the dollar-adjusted return clocked in at -32.54%, making the KSE-100 index one of the worst-performing indices in the region.

To recall, last year, the bourse had an upward move of 37.6% (46% in USD terms), the highest after FY14.

Reviewing the year-long pattern shows that tough political and economic conditions since the start of FY22 with the change of political set-up during the month of April’22 along with external financing issues due to freezing of the IMF program amid elevated commodity prices brought uncertainty to the market. In addition, the transition from the Emerging Market to a Frontier Market also put pressure on the bourse.

Adding to the woes, foreign exchange reserves started depleting, with the Pak Rupee losing significant ground against the USD and touching an all-time low of 211 per USD in Jun’22. Moreover, concerns over the inflation outlook pushed SBP to resume stern monetary tightening this year as the current policy rate of 13.75% is the highest since Jun’11. As a result, the bourse had a downward move over the year, it touched a peak of 47,356, with a low of 40,555, and closed at 41,541 points level, making the total change for the year at a loss of 5,815 points.

A closer look reveals that the last month of FY22 has been the most difficult month for the Pakistan stock market. Although Pakistan is edging closer to the IMF program, investors’ sentiments remained low due to persistent current account deficit, higher inflation figures and the government’s attempt to broaden the tax net in the FY23 budget in order to comply with IMF requirements. To note, the new corporate taxation measures affect nearly 13 sectors in the listed space, representing 80% market capitalization of the KSE100 Index. Subsequently, the KSE-100 index lost 3.6% or 1,537 points, with turnover thinning out even further.

.jpeg)

Sector-wise analysis reveals that the major downside to the benchmark KSE-100 index came from Cement with 2,359 points followed by Technology and Banks with 946 points and 506 points respectively. In particular, the scrips of LUCK (-1,113 pts), TRG (-1,014 pts), HBL (-423 pts), DGKC (-286 pts), and UNITY (-269 pts) turned out to be the most disappointing ones.

On the other hand, Fertilizer, Chemical, Miscellaneous, Automobile and Real Estate emerged as the best-performing sectors during FY22, as they added around 778, 501, 290, 180, and 52 points respectively to the benchmark index. To be specific, the scrips of EFERT (528 pts), EPCL (407 pts), MTL (368 pts), FFC (320 pts), and PSEL (318 pts) turned out to be the most pleasing ones.

Meanwhile, the All-Share Market Cap decreased by nearly Rs1.34 trillion, i.e., 16.16% lower than FY21.

Flow-wise, foreigners have continued on their selling spree, offloading $297.5mn worth of equities during the year compared to $387.34mn which was the highest since FY17.

On the other end of the spectrum, Individuals, companies, and Banks remained the aggressive buyers as they purchased $157.2mn, $115.2mn, and $111mn worth of equities, respectively. However, Mutual Funds and Brokers reduced their exposure by around $128.2mn, and $20mn, respectively. Insurance Companies too reduced their exposure by around $1.15mn during FY22.

Outlook:

The removal of cash subsidy, imposition of a levy on petroleum products and increase in budget revenue targets has increased the probability of

resumption of the IMF program which will rebuild investors’ confidence and provide much-needed certainty to the capital market in the coming months.

Moreover, the current account deficit is also expected to narrow down in FY23 due to economic slowdown and measures taken by the government to curb imports of non-essential items, providing respite to the market.

Another key area of respite could emerge from softening global commodity prices over inflation suppressing global demand.

Copyright Mettis Link News

33860